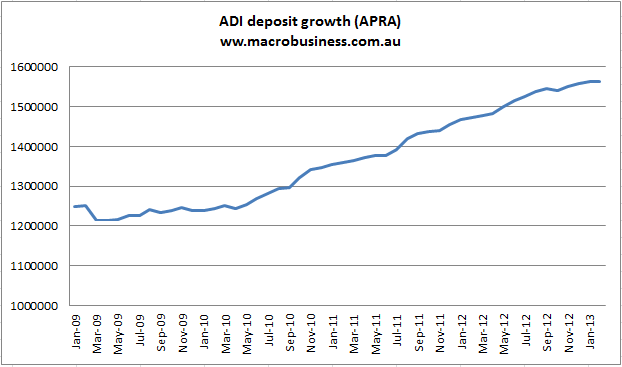

APRA has released its February banking statistics and deposit growth is going bye, bye on the month up just 0.1% and year on year growth is down to 6.6%. Here’s the aggregate chart with a plateau forming:

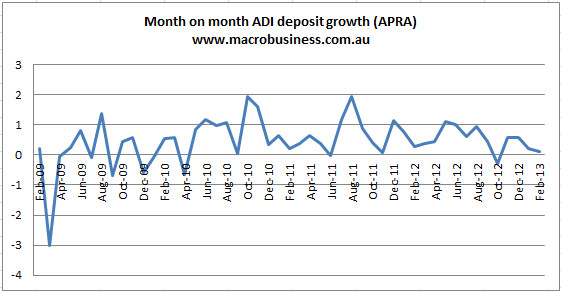

The month on month chart which is fading:

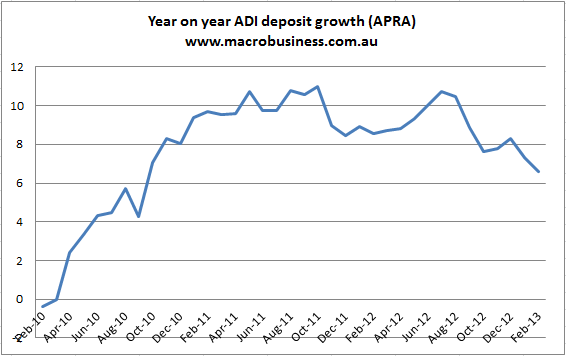

The year on year chart which is tumbling:

It doesn’t take Einstein to figure out more savings are going into assets now or just being spent. And there will be less savings too as national income keeps falling. I expect we’ll see the savings trend in the first quarter national accounts begin to fall too.

We are one uptick in credit demand away from the banks rushing into wholesale markets for more dough. Not that that’s a problem for the new and improved fast and loose RBA. What are you going to do APRA?