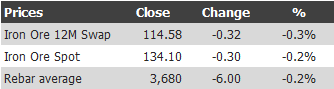

Find below the iron ore price table for March 20, 2013:

Rebar futures offset some of the weakness.

But the news flow today is all bearish. We might describe it as ‘the awakening’. FTAlphaville has a great summary of the very bearish debates suddenly seizing iron ore. The AFR has a decent article too on the same. Even the corporate rah rah boys of BS are sounding bearish. All of the material has been covered here previously but one quote from Merrill Lynch caught my eye:

The Indian government had placed a ban on iron ore mining in Goa during 2012, accounting for some ~40-45Mtpa of exports. The government has been reported as “considering asking the Supreme Court to allow ‘legitimate’ miners to resume operations”, which could bring an additional ~35Mtpa back onto an already depressed market

Oh dear.

There’s probably no immediate impact to prices from all of this bearishness, except to ensure that the speculators will stay clear and hoarding will remain a thing of the past. The other impact will be on aspiring producers. This is not a great context for poor old Roy Hill, which is the pick of them, and is aiming to raise funds. From the AFR:

Gina Rinehart’s Roy Hill Holdings has brushed off concerns about looming weakness in the iron ore price and expressed confidence that financing for the $9 billion Pilbara project will be in place by the end of the year.

Roy Hill chief executive Barry Fitzgerald said on Wednesday that the forecast volatility in the iron ore price was unlikely to affect the company’s plans as the project economics had been determined using a long-run iron ore price.

“The important point is that as the bumps have come and gone, the long-run price of iron ore, which is really symptomatic of when supply and demand come into balance, hasn’t really changed,” he told delegates at the Global Iron Ore and Steel Forecast conference in Perth.

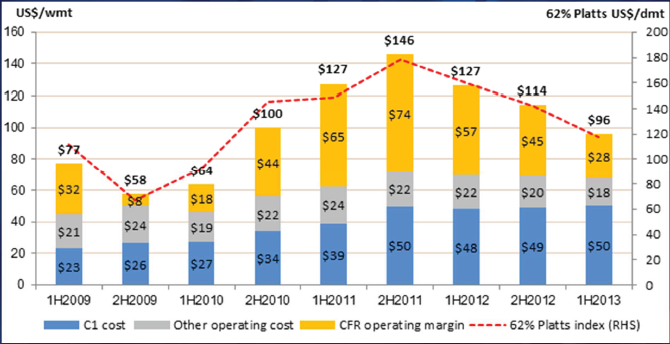

They want $7 billion to bring another 55 million tonnes of ore to market. Nobody knows the cash cost. But given FMG is the highest marginal cost expanding producer, with a cost of production stuck at $80 delivered (chart from their recent investor presentation below), it’ll need to be lower than that (or banks need their heads read):

Only one question I’d be asking. If Roy Hill is cheaper than FMG, why wasn’t it developed first?