Japanese investors are a powerful bunch in world markets. For a microcosm of this, just look at Australia; Japan plays a big role here in debt and in turn, in currency; and it’s a market that has been very attractive to foreigners of late, keeping the currency stubbornly high regardless of price changes in the country’s key exported commodities. BUT, as with everything yen at the moment, there is a serious shift going on.

In Neil’s FT story last week, Westpac FX strategist Robert Rennie pointed out that Japanese investors were selling AUD assets at an increasing rate. Although Japanese Ministry of Finance data showed net sales of only $1.5bn in Australian assets by Japanese investors for 2012, the rate accelerated sharply towards the end of the year:

Advertisement

If we isolate the November and December MoF numbers for 2012, the pace of selling was even more aggressive. Almost A$8bn of Australian assets was sold in those two months alone by Japanese investors. That is an all time record and gives a clear sense of how aggressive this selling was.

Which currency was most in demand in Q4? US$22bn was ploughed into Europe by Japanese investors while US$13bn was put back into ¥ assets. This very much confirms a point we have been making for some time now.

So it seems that even if Japanese investors have yet to be totally convinced by Abenomics, they may have been swayed by the impish smile of one Mario Draghi:

Advertisement

That chart, showing the fairly dramatic difference between Australian and European inflows from Japanese investors, came to us via Morgan Stanley’s Ian Stannard who argued that significantly the yen story is becoming more and more driven by domestic investors — having largely been driven by foreign investors up until now.

But even if domestic investors have yet to fully buy into Abenomics (and there is more on that down below) there is obviously a rotation within existing investments going on.

Advertisement

From JP Morgan’s FX team for example:

Three months into the sharpest yen sell-off in almost two decades, it is generally accepted that this move is almost entirely foreign-investor driven. If Abenomics – the currency-toxic combination of loose fiscal and monetary policy while the current account is deteriorating – were motivating domestic and foreign investors alike to sell yen, a wide range of flow and position indicators would be trending. In fact very few are […]

Since Abenomics began in November 2012, total foreign bond purchases have not accelerated (chart 2) but the regional rotation has accelerated. Monthly MoF data show strong buying of core Europe (¥817bn per month), tiny selling of peripheral Europe and New Zealand (-¥7bn and -¥9bn), negligible buying of the US (¥2bn per month), significant selling of Australia (-¥235bn), and a meaningful increase into EM Asia and Latin America (¥73bn and ¥159bn, respectively).

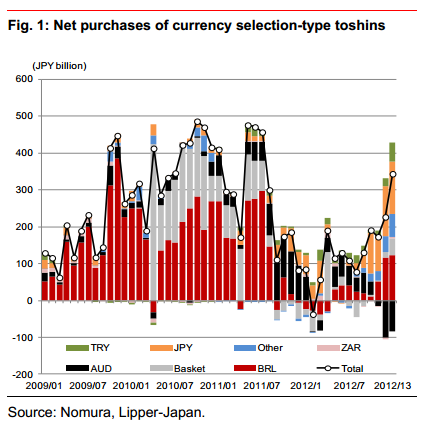

Interestingly, Nomura on Monday confirmed that Japanese investors continued to move away from AUD assets in January — at least, the retail ‘Toshin’ investment trusts which own about $300bn in foreign-denominated assets. However Nomura sees both net sales of foreign assets by the Toshins, a shift away from AUD, and a shift *towards* emerging markets:

January was the third month of net Toshin selling of foreign securities, to the tune of 700m yen or $800m, according to Ministry of Finance data.

Advertisement

There has been net selling for the third month in a row, while the pace of net selling slowed from the previous month (JPY430bn). Even though USDJPY and Japanese equities rallied in January, we could not see any clear evidence of recovery in toshin momentum. Some existing investors also regarded the JPY weakness as a good opportunity to book profits.

However, at the same time, net outstanding foreign holdings of the Toshins rose for the fourth month as the yen depreciated. Except in Australia:

While total foreign currency-denominated toshins outstanding rose, exposure in Australia remained almost unchanged. As a result, the share of Australian assets declined further to 18.3% from 19.3% the previous month. This is the lowest share since June 2011. By contrast, the outstanding in eurozone increased to JPY1.9trn (USD21bn) and its share recovered to 8.3% from 8.0% the previous month. The share of eurozone assets also recovered to 7.5%. Exposure to Mexico surged further to JPY239bn in January from JPY182bn in December. The shift from Australia into EM countries continued in January.

Advertisement

This of course could have implications for the Australian currency (and conversely the euro).

Japan holds somewhere in the region of 20 per cent of Australia’s national sovereign debt; about three-quarters of the total is foreign-owned. As for Japan’s position in the wider Australian debt market, Bloomberg in a report on the Japanese/AUD exodushas handily totted up that as of the latest available MoF data, Japanese investors held A$178.1bn equivalent of Australian-denominated debt at the end of 2011 — almost as much as the country’s entire outstanding sovereign debt (A$210.3bn) and a sizeable chunk of its total debt market (A$832.7bn).

Not surprisingly, the Bloomberg story observes that Australian asset managers take seriously the Japanese demand for Australian assets. But the story also reckons that this could be an indicator that “Mrs Watanabe” sees a top (or rather, a trough) for yen valuations and is taking profits. That’s consistent with what Westpac’s Reddie and the Nomura analysts say.

Advertisement

Jo McBride, who tracks Japanese pension funds, wrote an interesting post earlier this month explaining why she believes these investors will soon be sending a wall of money overseas:

Although returns on domestic assets have dwindled in recent years, pension funds’ have been discouraged from putting more of their portfolios abroad by the wall of cash coming the other way – from foreigners seeking the safe haven of the yen.

In June 2007, the Nikkei 225 stock index was briefly over 18,000, the coupon rate on newly issued 10-year Japan Government Bonds was 1.9% and the yen was at US$1= 122.68 (yen 1 = US$.0081507) .

The Nikkei has since struggled to keep its nose above 10,000 and the coupon on new 10-year JGBs has fallen to 0.7%. Yet for much of 2011 and 2012 the Japanese currency was below US$1= 80 yen (yen 1 = US$.0119518), an appreciation in five years of almost 50%.

Gains of this magnitude, at a time when markets elsewhere were in the doldrums, would have eaten up the earnings available on all but the riskiest of foreign currency assets, and such investments could anyway have involved lengthy lock-up periods.

Japanese pension funds, McBride says, have thinner cushions to fall back on than their American counterparts. Regulatory changes and the shifting demographics have created a more urgent need to match incomings with outgoings. Once they are confident a new era of the yen will be here for some time, their search for yield will drive them into more foreign assets. Mexico, Brazil, South Africa, peripheral Europe… it’s all possible. Or so it would seem.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.