The Reserve Bank of Australia (RBA) has released its monthly chart pack today.

The Pack (downloadable as a PDF or in separate GIF images as below) has 16 categories covering the state of the Australian and world economies, via diverse metrics and observations.

I’ve reorganised the charts as follows:

Economic growth

The major measure of economic growth (successfully argued as flawed in comparison to measuring true prosperity, in my opinion) is Gross Domestic Product (GDP) growth.

Here is the “world” economy:

What seems to matter to Australia:

And our own “growth”, which continues to decline to sub 2% per annum:

Inflation

The core “prey” or concern of the bullhawk is “inflation” (although they have no problem with asset price inflation) – are their concerns warranted?

Maybe in the US, where consumer price inflation is picking up strongly:

In Asia, the CPI is double:

And higher in India and China:

But anemic in Australia – might be time for the bullhawks to head off and go “advise” the Asian central banks:

Households and Credit

Households drive the economy, so what are they up to? First, they are still saving over 10% of disposable income:

But they are still shelling out more (near 12%) in interest payments and even though wages are rising, debt levels remain the same – so where’s the real saving?

Retailers certainly know this saving and dis-saving is affecting them. Sales growth is stagnating:

Maybe interest rates are too high? This graph doesn’t include the RBA 25 points cut of yesterday, but the official cash rate is now (except for the GFC shock low), the lowest in 20 years:

But are actual housing lending rates that low? No – even with steady interest margins, bank lending rates – outstanding or new – are still very high. A dilemma…

Business

With retail sales sluggish, residential construction falling and households saving like never before, how are businesses faring? Great if you are a miner:

Even though mining is still the smallest employment group – with manufacturing employing 4 times as many – it has grown substantially:

Businesses continue to deleverage, with listed companies balance sheet net debt to equity at 30 year plus lows:

What about expansion through equity? The large slug of equity raised – to retire debt – during 2009, has wilted away and is exarcebating share buybacks (where investment money is returned to investors….)

But there’s a huge capital expenditure boom right? Only in mining (I wish this chart was adjusted for inflation and per capita basis) and the estimates (the pale blue dot following the parabolic curve on the left) are firing ahead:

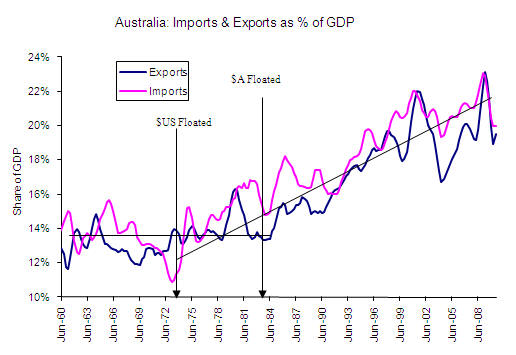

Exports

This leads me to the most stunning of all the charts contained within the Chart Pack. Macrobusiness has been covering the Terms of Trade “dilemma” for some time and this post WW2 chart says a lot:

The reason? Iron Ore and coking coal. Note the spot prices have fallen considerably below contract prices, which are likely to be revised soon (also note how contract prices have shortened in time at the behest of the big miners who wanted to capture the volatility of the spot price. This bites both ways…)

Here’s the clincher – the fragility of the Australian economy laid bare. Note how the resource boom coincides with the bubble on the Australian share market from 2003 onwards. More on that in a bit:

Where is this all going? The Middle Kingdom mainly:

This fragility – the opposite message to that prevailed by the mining-politico complex – is borne out by this stunning chart by Leigh Harkness, showing how exposed the economy is to any terms of trade shock from a collapse in exports:

Share Markets

Finally, let’s look at the share market. On the back of our resource export dilemma, this chart shows why the industrials just don’t matter anymore (since 2003 at least):

But dividends do matter as Aussie yields climb near 5% (more with our generous, if inefficent franking system). The rest of the world is catching up however. Remember an increase in dividend payout means businesses are returning MORE money to shareholders and not investing in growth in earnings: