The National Australia Bank (NAB) has released details of a record result today, overshadowed by the glitches on the ASX.

The basic summary of the result is thus:

- 19.2% increase in cash profit to $5.5 billion

- 5.7% increase in revenue

- 23.6% increase NPAT of $5.2 billion

- 2.34% to 2.17% decrease in Net Interest Margin (NIM) since March 2010 HY

The standouts were a large increase in mortgage growth and business lending, subsequent reductions in bad debt charges and arrears rates (which goes counter to the notion that current interest rate levels are too high) and an overall increase in market share.

A splendid result for shareholders, but a closer look is warranted.

Market Share and Funding

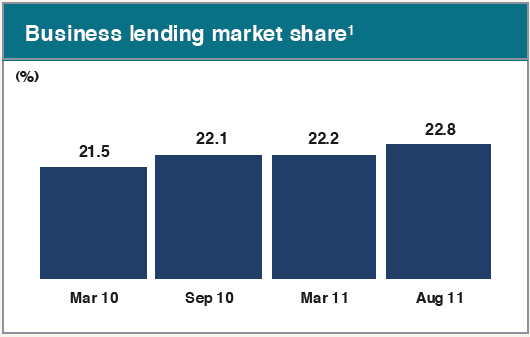

Business lending market share improved somewhat over the year:

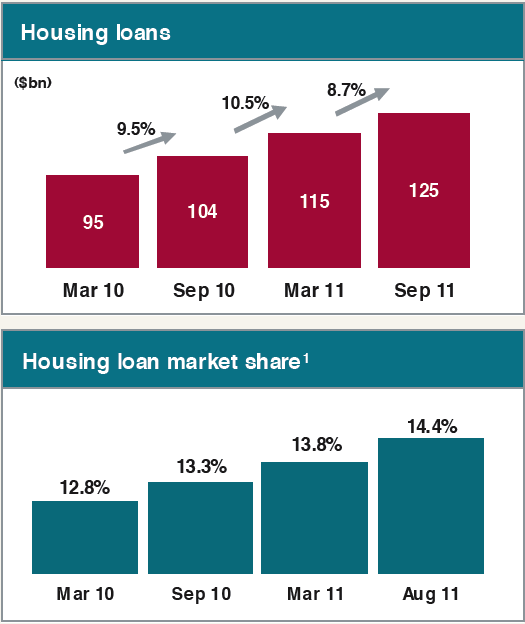

Whilst housing loan market share improved significantly from a low base, showing NAB’s determination to push ahead in this market.

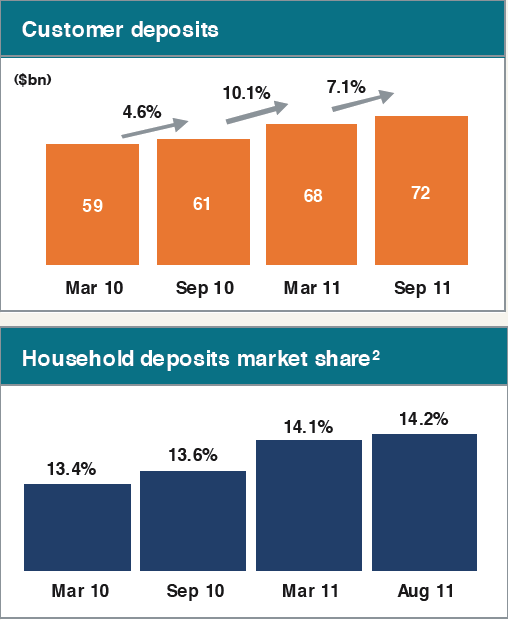

A rise in customer deposits has also seen NAB take some market share from the other Big Four and eased funding concerns:

Mortgages and Arrears

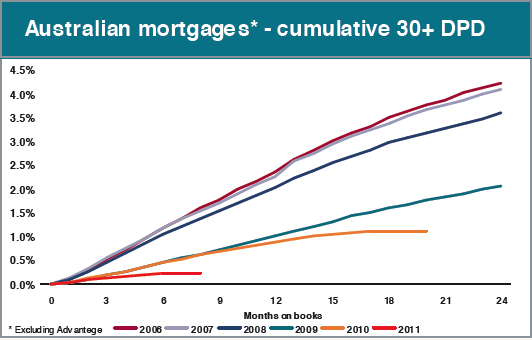

The residential loan book 30 days past due vintage from 2006 through to 2011 shows that recent loans have been performing well:

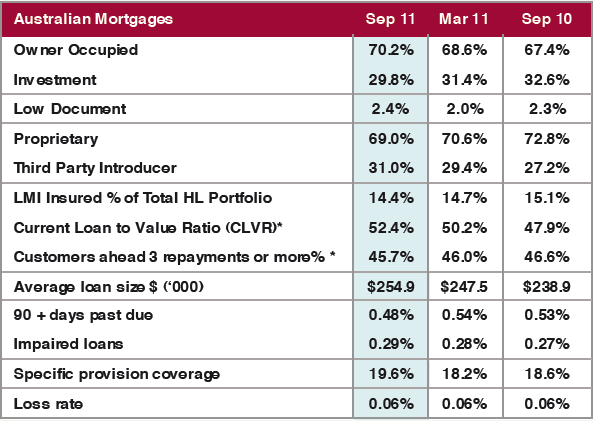

The following table of metrics shows that 90 days past due has decreased from 0.53% of the book to 0.48%, with impaired loans slightly rising, whilst Loan to Value Ratios (LVR) have increased substantially – from 47.9% to 52.4%.

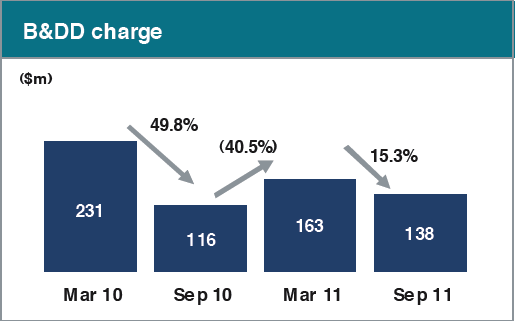

Pushing NAB’s statutory profit up is a significant reduction (some $440 million) in charges for bad debts,:

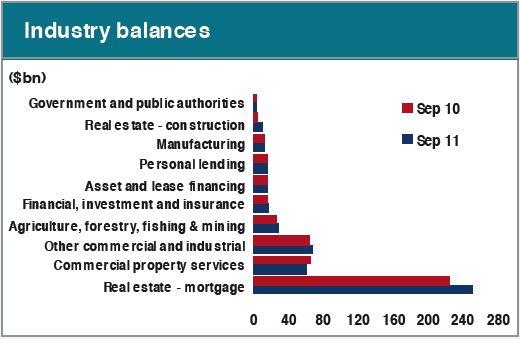

The effect on NAB’s drive to increase and concentrate its residential mortgage asset portfolio is shown with this graph:

Business Lending

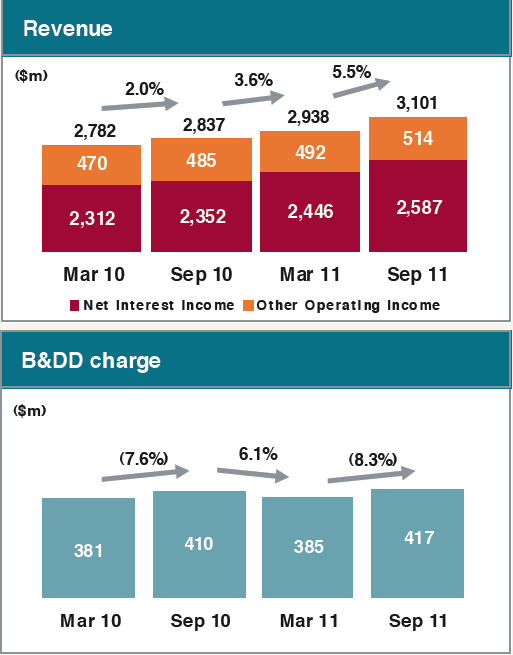

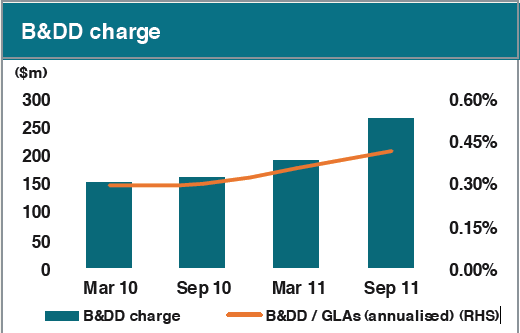

Whilst revenue from the business lending division is increasing (earnings up nearly 10% on last year’s effort), bad and doubtful debt charges (B&DD) across the system have been relatively well contained:

However, B&DD charges for SME businesses has been increasing at a fast clip:

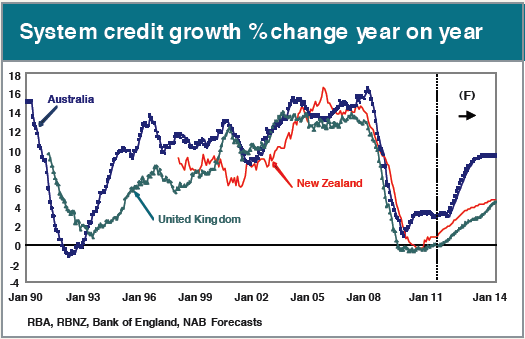

Finally, the economic team at NAB have compiled a series of forecasts regarding the change in growth of credit across the Australian, UK and New Zealand economies:

Overall a good result, with a subsequent increase in the dividend, which will please longer term investors. Surprisingly, arrears levels and bad charges have been reduced and contained, although there are some small signs that SME businesses are feeling the pinch. Risks abound due to funding pressures and as NAB moves alongside the Commonwealth Bank (CBA) and Westpac (WBC) as concentrated Australian real estate mortgage investors.