Today’s chart comes from Naked Capitalism, discussing a paper regarding the remarkable recovery of Argentina post its default in December 2001.

Following the default, which included removing a currency peg against the USD and subsequent devaluation, there was a severe financial crisis, with huge contraction in GDP – 11% for the year.

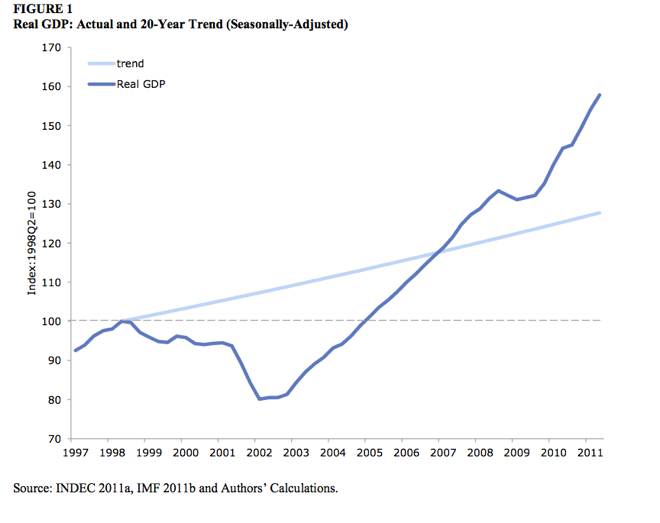

However real GDP – adjusted for the structurally high inflation (double digit) in the South American economy – returned to pre-crisis level after 3 years and returned to trend growth thereafter, as the chart above shows, with 8% real growth forecast for next year.

The drivers of the growth:

that the role of exports is not very large during the expansion of 2002-2008. It peaks at 1.8 percentage points of GDP in 2005 and 2010, and amounts to a cumulative 7.6 percentage points, or about 12 percent of the growth during the expansion. The story for net exports is even worse, with net exports (exports minus imports) showing a negative cumulative contribution over the period. The recovery is driven by consumption and investment (fixed capital formation), which account for 45.4 and 26.4 percentage points of growth, respectively.

Lot easier to grow your economy when you don’t have a millstone of debt around your neck isn’t it? Don’t cry just yet Greece (and Ireland, Italy etc)..