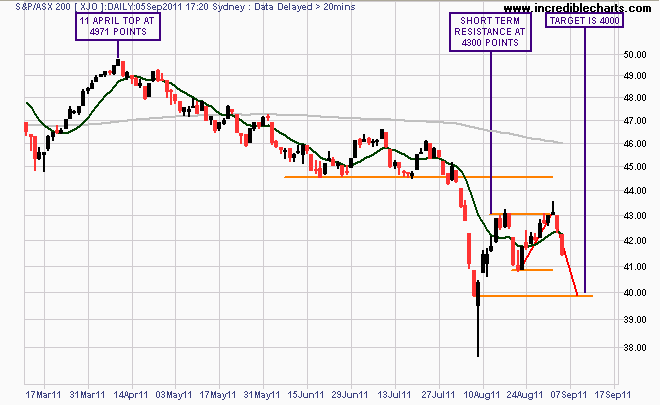

The S&P/ASX 200 slumped over 2% down today, after absorbing Friday’s US job data. The index is down 101 points or 2.4% to 4141 points. In after hours trading, the market is at 4130 points waiting for the European market whilst the US has a day off today.

Asian markets experienced similar losses, with the Nikkei 225 losing 1.8% to 8784 points whilst the Hang Seng closed down 3% to 19601 points.

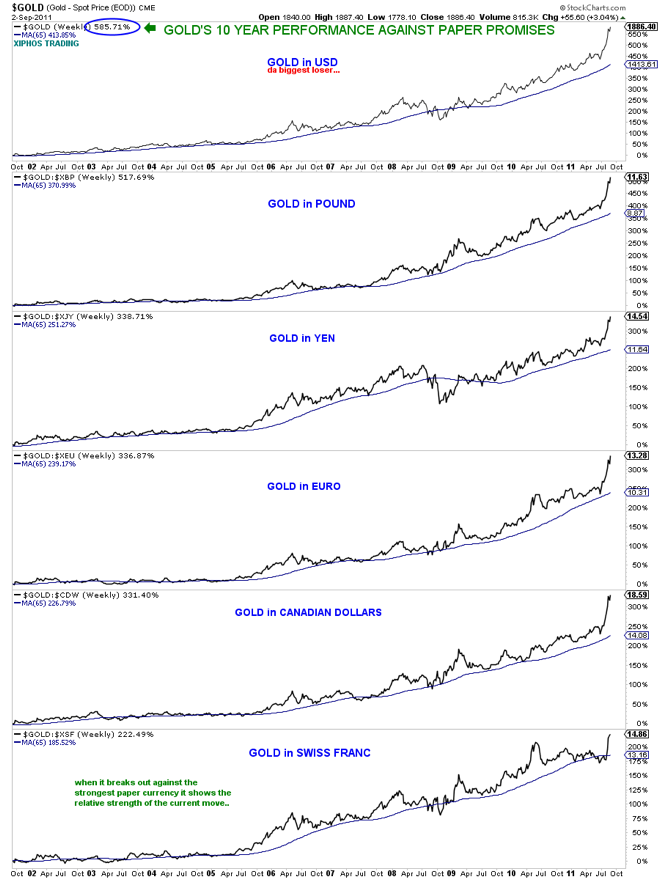

In other risk assets, the AUD lost nearly two thirds of a percent against the USD, now at 1.0578, whilst WTI crude dropped nearly 2% to just below $85 USD per barrel. Gold stood out – again – and rallied over half a percent to $1887 USD an ounce. As it has been against almost everything really:

From Xiphos Trading

Movers and Shakers

It’s blood red across the board on the ASX, with only 9 stocks out of 200 actually up for the day – Tishman Speyer Office Fund (TSO) the standout up 2.8%. For the rest its bad news with the energy and financial sectors hit the hardest.

Overall the banks lost between 2 and 3%, NAB the biggest loser down 3.15%. AMP finished down over 5% but this included its dividend whilst Macquarie (MQG) retraced sharply, falling over 4.4%

BHP Billiton (BHP) was a huge drag falling 3.4%, whilst RIO fell similarly – Bluescope Steel (BSL) continues to get pounded by the short sellers (sorry about that, guilty as charged) and is down nearly 8%

The Charts

Last Thursday’s bearish candle – called a shooting star, Friday’s sell off in anticipation of US jobs figures – and the absorption thereof and requisite sell down of US and Euro markets have led to today’s bath of blood.

Once again, we are now only a 100 or so points off the previous bottom close on the 8th of August. There is a definite battle between the knife catching bulls and the red-tempered bears around the 4200 point mark.

As I proposed in my June post “A Tale of two Corrections” price action is looking more and more like the 2001-03 bear market.