Three companies reported earnings today on the ASX: Rio Tinto (RIO), Transurban (TCL) and Energy Resources Australia (ERA). Macrobusiness will be reporting on earnings and valuing the key companies throughout the earnings season. Remember to bookmark the overall update here.

ERA reported a loss of $121.7 million in the six months ended June. This compares starkly with a profit of $22 million in the same corresponding period last year. The slump in earnings is largely attributed to the heavy rain experience in January at the Ranger mine in the Northern Territory.

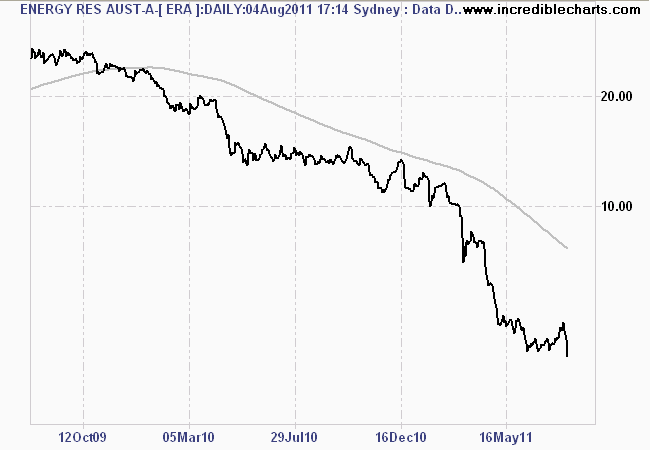

ERA, controlled by Rio Tinto(RIO) has experienced a significant slide in its share price this year, as seen by the chart below, and dropped nearly 10% on the result today. Book value for the uranium miner is now $4.34, some 10% above its last traded price.

ERA is seeking to cut costs, whilst extending the life of the Ranger mine. It has a good cash position with no debt but is largely beholden to the uranium spot price which has taken a beating since the Fukushima nuclear emergency.

Empire Investing does not consider ERA investment grade due to the risks involved and has not made a valuation.

![]() Rio Tinto (RIO)

Rio Tinto (RIO)

RIO reported record First Half (HY) earnings of $7.6 billion, some 30% above the same corresponding period last year. This accounting result was reinforced by strong growth in operational cashflow, also up 31%. RIO declared an interim dividend of 54 cents (USD) per share, with the ex-dividend date of 10th August. This equates to a dividend yield of approx. 2%

RIO also announced an increase in its share buyback program, extending to $7 billion, all to be completed by the first quarter of 2012. However, this has been eclipsed by the increase in capital expenditure, up to $5.1 billion in the first half (compared to $1.8 billion last year).

CEO Tom Albanese explained that though volumes were lower and RIO experienced ructions from serious weather in the first quarter, the result was due to higher prices received by the market. The chart from the RBA shows the differences in price:

Empire Investing will provide a valuation later, our major concern is the variability of returns (Return on Equity fell from 62% to 19% from 2006 to 2008 and climbed to 30% in 2010). At first glance, RIO’s half-year ROE has declined to 25% (based on a normalised period) due to the increased equity position.

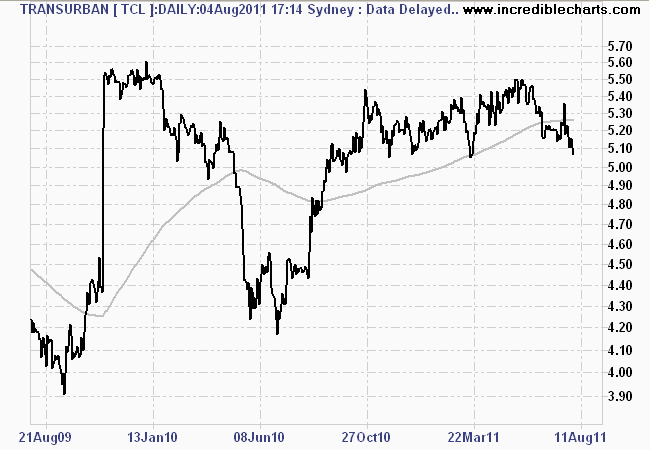

Transurban (TCL) is a major toll road developer and manager, with extensive interests and holdings in Australian and in the US. TCL announced a full year (FY) $118 million profit today, an almost doubling of profit over the previous year. This is a good turnaround for a business struggling to make consistent returns amongst crippling debt loads.

TCL declared a final distribution of 14 cents, to be paid on 11th August (the company is already trading XD), for a total dividend of 27 cents. That equates to a dividend yield of 5.3%, but there are no franking credits attached.

Although management consider TCL “well-placed” with potential growth prospects, the company is still broadly exposed to its large debt loads and interest rates, although refinancing is not a large problem at this stage.

Due to the very small Return on Equity (ROE) of approx. 9%, a very high net debt to equity ratio over 100% and the inconsistent earnings history, TCL is considered non-investment grade by Empire Investing.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no current interest in the businesses mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.