Following on from last week’s analysis of the Telstra/NBN Co agreement, we shine the equities spotlight on Australia’s big telco – Telstra.

Following on from last week’s analysis of the Telstra/NBN Co agreement, we shine the equities spotlight on Australia’s big telco – Telstra.The Business

Telstra is Australia’s largest telecommunications company and the owner of the majority of Australia’s fixed-line copper network. Its business can be split into the following segments:

- Consumer – mobile, broadband, telephony and PayTV services for retail customers

- Small and Medium Business – telecommunications services for SMEs

- Government and Large Business – telecommunications services for the big boys

- Sensis – directory and information services such as Yellow Pages as well as interests in several Chinese web and mobile service companies

- Wholesale – provision of network services to their competitors (e.g. Optus)

- Overseas interests – provision of mobile services in Hong Kong and full telecommunications services to

The Financials

Telstra has a reputation as a dividend stock, distributing much of its earnings to shareholders. However this has not resulted in a good share price performance, with Telstra dropping from $5.50 to $2.90 per share over the course of the last 10 years.

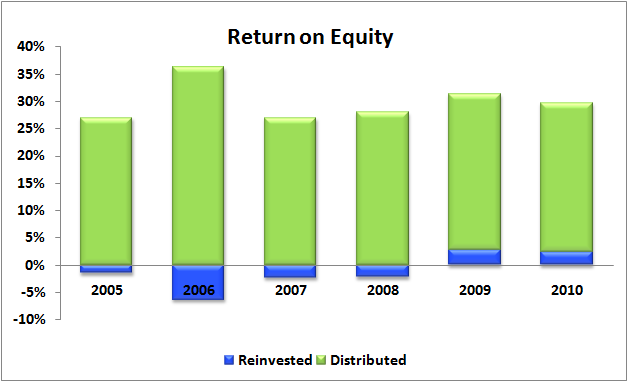

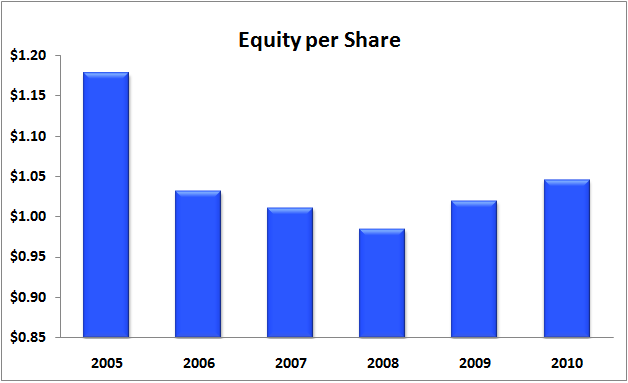

Over the last 5 years return on equity (ROE) has averaged 30%, which is an impressive result. However, given Telstra’s near-monopoly position in telecom infrastructure, this is not unexpected. Up until 2009 TLS had a habit of reinvesting and distributing more than it actually earned, which can be seen as the negative reinvested amounts in the ROE graph below. This had the effect of lowering equity per share and was also a sign of poor capital management. Reinvestment of unearned-profits ceased in 2009, which coincided with the departure of the Three Amigos and the sale of the last portion of government-owned shares. However the FY11 forecast is for another year of un-earned reinvestment, indicating TLS has returned to bad habits.

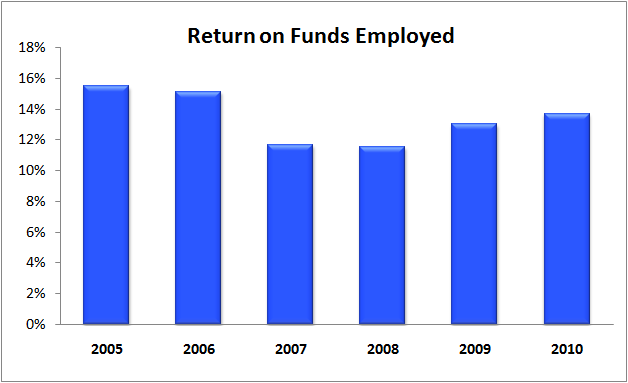

Telstra’s debt levels are actually quite high given their ROE performance, with interest bearing debt of $15b compared to FY10 NPAT of $3.9b. This reduces the return on funds employed to less than 15%, indicating they are not as good at turning capital into profits as their 30% ROE would imply.

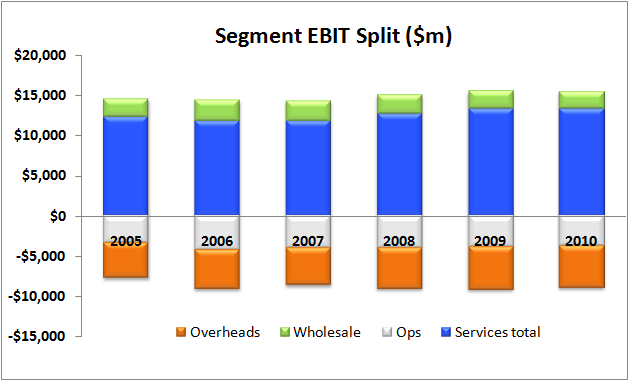

The EBIT split by segment is shown below. The Services segment comprises the retail, business, government and Sensis divisions whilst Operations represent the costs associated with building and maintaining TLS infrastructure. The Overheards costs represent marketing and corporate costs.

The 2010 revenue split by product and service type is shown below. It is clear the mobile services division is the most dominant in terms of revenue streams.

Management

Telstra’s recent management history has been colourful. The appointment of Sol Trujillo in 2005 marked the start of a very tense period between Telstra and the Howard government. This lasted throughout the period where the final tranche of TLS shares were sold and culminated in 2009 with the departure of the last or Trujillo’s right-hand men appointed during his tenure. During this period TLS share price dropped by over 30% and Trujillo walked away from the job with a large golden handshake, but not much in the way of accomplishments – at least according to most of the media commentariat.

The majority of the current board have been in their positions for 3 years or less, indicating a comprehensive change since the Trujillo era. Current CEO David Thodey has been with TLS since 2001, whilst the rest of the board has a broad range of experience from within corporate Australia. Short term remuneration typically makes up 25% or less of base salary, with the short term component decreasing markedly in 2010 as company performance dropped. Overall the remuneration scheme appears to be the run-of-the-mill set up.

Telstra and The NBN

Telstra recently released the first official details of the agreement between it and the NBN Co. The agreement stated that TLS would disconnect its copper network as the NBN fibre optics links rolled out. It also agreed to transfer its telephony and broadband services to the new NBN infrastructure and not to use the old copper network to compete against the NBN. During the rollout, TLS would allow access to its infrastructure so the NBN can be constructed.

TLS will be paid by the NBN Co for the disconnection of its copper network and the access to its infrastructure. The agreement only specified payments totalling $11 billion, which is a calculated Net Present Value of all the payments to be made during the expected 30 year life of the agreement. The actual amounts to paid and over what time frames were not provided. For this reason, it is extremely difficult to assess the impact on TLS furutre revenues as they will lose revenue from their infrastructure services whilst being compensated by the NBN with as-yet unknown amounts.

Regardless the NPV calculations, TLS has agreed not to compete with the NBN and has also agreed to transfer its network customers to the NBN as it is rolled out This means Telstra’s infrastructure assets will slowly be written off/disposed of and TLS will become a service-oriented telecommunication company. The large mobile services component of TLS’ revenue bodes well for the future, as this component of the business should not be affected by the NBN.

A more comprehensive analysis of the NBN agreement can be read here.

Opportunities

- Telstra is Australia’s largest telecommunications company and currently holds a monopoly on network infrastructure

- Return on equity is high and generally predictable

- The NBN agreement should provide a sizeable and consistent revenue stream over the next 30 years

Risks

- The NBN deal will force TLS to change from an infrastructure and services company to a services-only company

- The NBN deal carries a high level of regulatory and legislative risk given the current policies of the Federal Oppposition and the highly political nature of the NBN project itself

- The impact on revenues as TLS turns off its network and transfers to NBN-provided services is unknown at this stage

- Debt is relatively high and capital management has been less than optimal in the past

Summary

Despite its dominant market power, Telstra has shown to be a poor manager of shareholders capital. This is reflected in low returns on funds employed (i.e. high debt), decreasing equity per share in the past and extremely poor share price performance over more than 10 years. It has recently secured a large funding deal with the NBN Co to retire its network assets, however the compensation details are scant and the financial impact of losing its assets are unknown.

Due to the inherent risks associated with the NBN, as well as poor financial fundamentals for such a monopolistic business, Empire considers Telstra a Poor Company and not an investment-grade security.

Valuation

Using an equity per share value of $1.00, an average normalised (inc franking credits) ROE of 35% over 5 years and assuming 0% of earnings are reinvested, we value TLS at $2.68. However, because Empire considers TLS a Poor Company, we do not specify a maximum buy price.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no current interest in the businesses mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.