There is nothing more certain in life than death and taxes: today’s chart will focus on the latter.

I consider taxation reform as the “only hope” for future productivity/microeconomic enhancements (as we’ve botched the macro as highlighted by House and Holes (and others here) regarding the MRRT and SWF), and these two charts, taken from the 2008 Taxation Review highlight the problems.

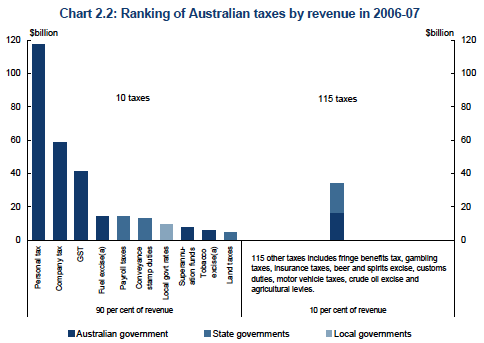

First, consider how 90% of all revenue is drawn from just 10 taxes – the “usual suspects”, whilst the remaining 10% comes from 115 taxes.

There are two major problems with this structure. On the one hand, the gross inefficiency and hazards involved in business and government having to deal with so many overlapping, complicated and such minor revenue raising red-tape. Fringe Benefits and Luxury Car Tax being a particular complete waste of time – the solution is a small increase in higher marginal income tax rates to “punish” the higher earners who want that Porsche. There are countless (actually 115) other variations of this ridiculousness.

On the other hand, the gross reliance on personal income tax (the largest bar of the 10) imbibes the system with fragility. This could be arrested by doubling the GST and increasing company and capital gain tax rates. (also in a future post I’ll show how wasteful the collection of most of this income tax is – in fact, for those earning up to $50,000 a year, it should be abolished)

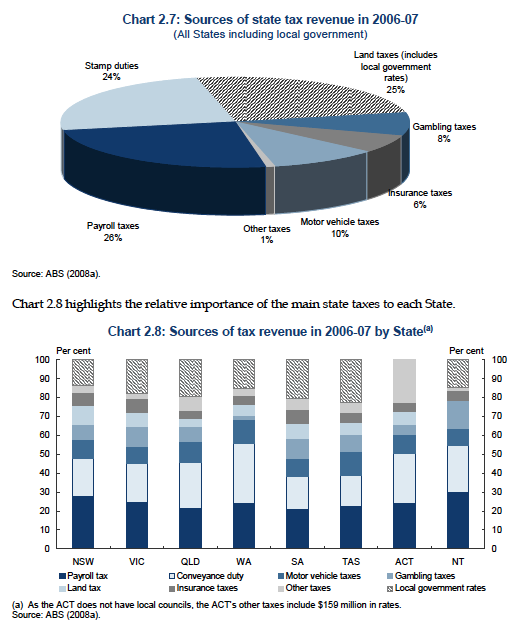

Secondly, this combined chart of sources of tax revenue for States highlights a problem raised by Delusional Economics and The Unconventional Economist. A reliance on housing transactions (stamp duty) puts great pressure on State budget finances (who cannot rely on internal money creation and must resort to public asset sales (e.g QLD) or selling bonds directly (e.g NSW)).

Again, another problem – whilst a quarter of revenue comes from transactions, thus reducing capital productivity (and increasing speculation) and labour mobility (increases the cost of moving), another quarter of revenue comes from labour-killing payroll taxes.

A tax for employing more people…how interesting. Again, simply increasing the corporate rate of tax (especially for non-SME, i.e big business) would be a much more effective solution and would “free up” the countless brigades of tax accountants into more productive endeavours.

There are a myriad of solutions to these problems, with increased Federalism (i.e more revenue raised via Federal governments) the most likely outcome. The Tax Summit this year will also likely come up with no real solution, as business, labour, the public and politics on both sides have shown these last few years an intransigence against meaningful progress.

The other side of the coin is the wasteful and inefficient welfare/tax transfer system (which comprises nearly half of personal income tax), but that’s for another chart or two to discuss.