Yesterday the retail stocks of David Jones, Harvey Norman, Myers and JB Hi-Fi all took a hammering. It was sparked by a David Jones earnings downgrade as well as an awful run of retail spending/consumer confidence data. To summarise the blood letting: David Jones (DJS) plummeted 18.2% to $3.20; Myer (MYR) dropped 6.4% to $2.48; Harvey Norman (HVN) dropped 4.6% to $2.30.

Yesterday the retail stocks of David Jones, Harvey Norman, Myers and JB Hi-Fi all took a hammering. It was sparked by a David Jones earnings downgrade as well as an awful run of retail spending/consumer confidence data. To summarise the blood letting: David Jones (DJS) plummeted 18.2% to $3.20; Myer (MYR) dropped 6.4% to $2.48; Harvey Norman (HVN) dropped 4.6% to $2.30.Meanwhile, Empire’s favourite retail stock JB Hi-Fi (JBH) dropped 5.3% to $15.65. Despite our recent Equities Spotlight article singing its praises, JBH fell with the rest of them – as did our portfolio value. Nonetheless, when one of your stocks drops as a value investor you have to ask yourself two questions:

- Is it still a great stock?

- Is it even better value now the price has dropped

Is JB Hi-Fi still a good stock?

Retail spending is down, the consumer is cautious and keeping their wallet shut Scotsman-style, our federal politicians are engaged in savage hand-to-hand combat over a carbon tax, Greece is in a slow-motion implosion and the US congress is playing debt chicken with the world’s largest economy. With such macro uncertainty it’s little wonder that investors are staying clear of those companies that sell discretionary goods. However, great companies survive such environments and eventually emerge stronger as the economy rebounds. We believe JB Hi Fi is one such stock.

Financials

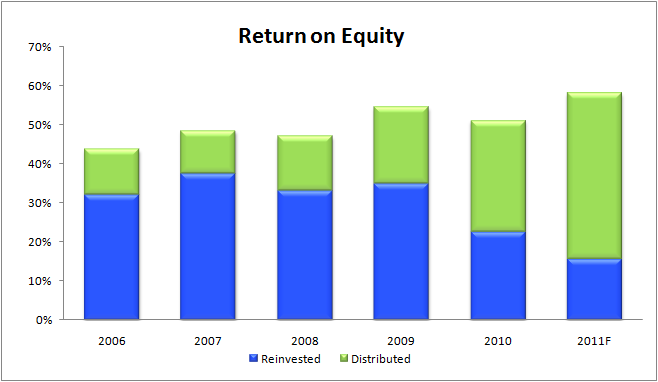

An in-depth rundown of JBH can be found at the MB equities spotlight article here. To summarise, JBH’s return on equity (ROE) has averaged 50% over the last 5 years, equity per share has increased 235% and borrowings are modest. Its financials are great and management has decided to increase dividend payouts as they saturate the Australian market – indicating a good grasp of capital management.

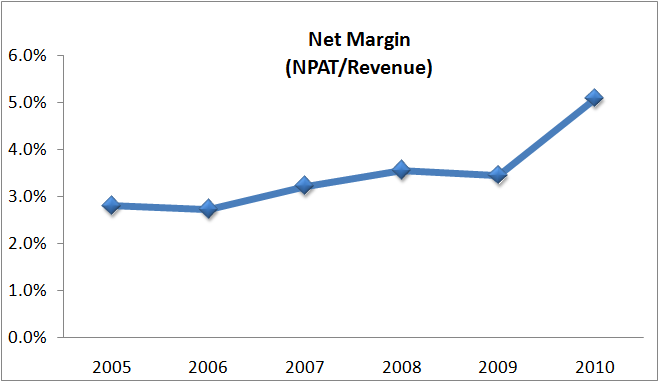

Another promising sign is an increase in JBH net margins, indicating that costs are being well-control despite rapid growth.

The recent price drop hasn’t changed any of the above. No doubt earnings will be impacted if consumers stay cautious and sales drop, however the underlying business will still retain a robust balance sheet with low debt.

Is it better than its peers?

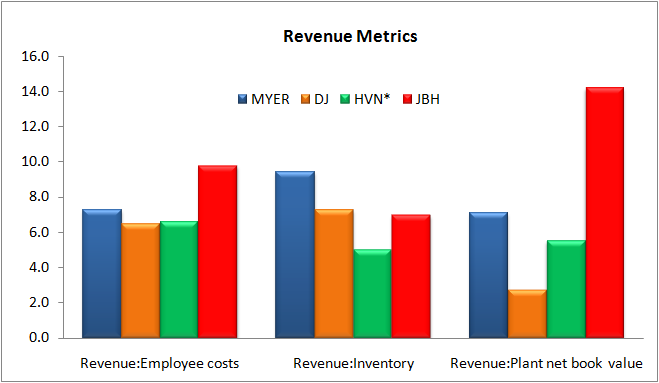

Based on my favourite metric of ROE, JBH is well ahead of HVN, DJS and MYR – whose ROE range between 20% and 30%. From a quantitative viewpoint, I much prefer JBH’s business model of small, spartan stores crammed with high-demand electronic goods. By contrast HVN, DJS and MYR typically have large floor spaces, more employees and are stocked with a greater variety of goods. This opinion appears to be backed up by the following revenue metrics I’ve derived from the FY10 annual reports of each company:

- Ratio of revenue to employee costs (i.e. labour)

- Ratio or revenue to inventory costs (inventory as of FY10 years end)

- Ratio of revenue to plant and equipment (net book value)

As we can see, JBH is streaks ahead on both labour and plant ratios, whilst it is on par when it comes to inventory. This would appear to confirm my previous hypothesis – DJS, MYR and HVN all spend far more on labour and plant to produce one dollar of revenue compared to JBH. This difference can’t be explained away by size, as JBH actually has higher revenues than both DJS and HVN. The inventory levels don’t tell us as much, except possibly that MYR is very good at stock level management.

So JBH has better ROE and can generate more revenue from a smaller physical asset base. This, combined with its increasing margins and higher ROE, tell me that it is indeed the superior retail company out of the group.

Is JBH good value now?

In my opinion, yes. It’s one of the best listed retailers on the ASX and has just experienced a big price drop brought about by another company’s troubles. In the previous JBH article The Prince valued its shares at $20.37, based on an 80% normalised ROE dropping to 70% over ten years.

Given the recent slew of retail data the 80% forecast ROE is probably too high (although the recent share buyback does complicate the forecast). However, to justify the current price of $15.60 I’d need to drop the average ROE for the next 5 years to 63%. That represents a drop in earnings of 20% from forecast, which would be a massive hit – although not unheard-of given DJS’ recent confession. If JBH comes through the next earnings season with minimal downgrades, I’d wager the market will look more kindly upon its share price. And given the strengths I outlined above, I think there’s a decent chance of that happening.

Which means right now, it’s bargain time on JBH shares.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has an interest in the business mentioned in this article (JB Hi Fi). The author also owns shares in JBH personally. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.