Following on from Q Continuum’s post on investing during sideways markets, today we shine the light on Australia’s best retail stock, JB Hi-Fi (JBH). Interestingly, this position is not shared with the current marketplace, as JBH remains the No.1 stock to sell short (i.e to profit on a fall in price), with over 14% of stock on short-seller’s books. Fairfax (FXJ) at 13%, Perpetual (PPT) at 6% and Wotif (WTF) at 4% are also experiencing heavy selling.

The Business

JB Hi-Fi (JBH) is a home entertainment retailer that dominates the sector. Products include portable music devices, games, music/movies, LCD/Plasma televisions and computers. JBH recently purchased the Clive Anthony’s retail group and announced a share buyback plan of up to 10% of shares on issue.

Financials

JBH has sustained a remarkable 63% average normalised Return on Equity (ROE) for the last five years. Previous to this year, it has done so using modest debt, evidenced by a high Return on Funds Employed and low debt-equity ratio.

There are some intangibles on the balance sheet, but they are minimised due to the business model of rolling out new stores based on free cashflow and reinvesting capital at high rates of return.

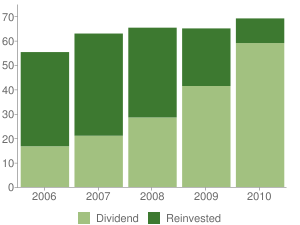

Notably, the proportion of profits reinvested in the business is reducing over time (see ROE chart) as the business model matures and market reach is almost completed. JBH recently announced a share buyback plan, more evidence of a slowdown as the business finds it harder to spinoff cashflow.

JBH Return on Equity

Future growth in the retail sector is reliant upon continued consumer spending and population growth, both of which are slowing. JBH is well placed, unlike its competitors, to weather these demographic and microeconomic factors due to its sound balance sheet and excellent use of working capital.

JBH recently purchased the Clive Anthony’s white-goods business, and has already started to incur losses from restructuring (mainly write down on intangibles).

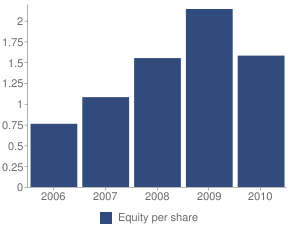

JBH Equity per share (note change in last year due to buyback)

Book value has increased steadily over the years, from $79 million to $293 million, but this will change substantially due to the share buyback.

Management

Capital management has been prudent and sensible, with excellent incremental returns on equity and very sound business practices (particularly working capital). Small amounts of capital have been raised but have not diluted earnings or return on equity. Management have been forthright and forthcoming with reports, results and warnings. A very well managed business through good times and bad

Key Risks and Opportunities

- Likely to expand and provide additional revenue using the same business model, albeit at slower rates

- Excellent brand name recognition and loyal customers

- High barrier to entry for competitors due to excellent working capital, economies of scale and low rent

- Expansion funded by cashflow

- Cautious consumer may weigh down on growth or stagnate revenue

- Online competitors can provide even higher margins and low costs, particularly with strong AUD

- Saturation of conventional retail market almost complete

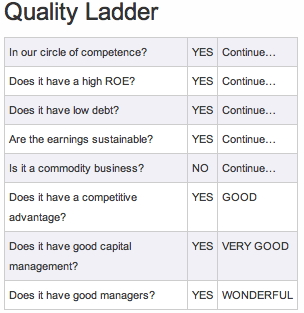

Conclusion and Valuation

JBH has a substantial competitive advantage as it continues to dominate its retail electronic competitors. Nothing comes close in terms of business acumen, customer reach, capital management and substantial returns to shareholders.

It’s excellent brand loyalty, effective use of working capital, and robust business model creates a very good barrier to entry for new competitors, although the online internet consumer space is an unknown. This robustness was reflected during the GFC when the business continued to flourished and during the post-GFC “cautious consumer” phase. Due to these elements, Empire considers JBH a “Wonderful” company.

Valuation

JBH has had an average NROE of 63% over the last five years, but the important metric underlying this is the reinvestment ratio, which is declining. Coupled with the share buyback, the forward valuation methodology gets a little tricky, with an expectation that growth in earnings will likely moderate, whilst dividend payout will increase over time.

Empire currently values JBH at $20.37 a share, based on a increased dividend payout ratio (and reduced reinvestment ratio of 25%).

Normally, a 10% Margin of Safety would apply, but due to consumer spending risks, and the increased competitiveness of online retailing, Empire would apply a minimum 15-20% Margin of Safety, with a maximum buy price of $17.71

Disclosure: The author is a Director of a private investment company (Empire Investing), which has a long position and may consider future additional long positions in the business mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.