Reader, Bamboozled, recently left a comment on my “Trouble with Funds Management” post, asking what direction to go with her super:

I’m a 30 something trying to consolidate a sizeable sum spread across 4 funds into something that resembles a reasonable super bet.

At the most basic level I have 2 lots of dosh in corporate funds (but from what I can gather one of those is actually a corporate plan within a retail fund?) one in a government fund and one in what I think is retail.

If reveiwing the ratings tables is only going to tell me how these institutions are performing against a flawed index, then what sort of questions SHOULD I be asking the respective funds to get an answer that will assist me to make an empowered (and hopefully profitable) choice?

As a rank industry outsider – how does one go about identifying an option that will make a real rate of return, without having to go down the SMSF path? I really don’t have the financial savvy (or to be frank the inclination) to go there.

At this stage I think this means I need to see a financial planner, but that leaves me feeling like I will be swimming with hungry pirhanas! What sort of questions should I be asking a Financial Planner to avoid the commission trap, and to be able to make a discerning choice about their abilities to best represent my interests?

Super = Frustration

Bamboozled’s frustration is widespread, and a result of the evolution of the superannuation industry through the myriad mutations imposed by successive governments, industry participants and media. For Generation X particularly (and I count myself among them, though I despise the classifications) the complexity of super is overwhelming and its no wonder that apathy sets in. This is exarcebated by the fact that most Gen X and Gen Y’s may have up to 5 or more jobs within the first 10 years of employment (and probably will change again that many times in subsequent decades).

Therefore, by fault and not design, most will have at least 3 if not more superannuation funds and will receive mind numbing multi-page long “statements” around August each year and will rightly put them in a pile and forget about them – hey its not like you can use the money anyway right?

Advertisement

Fix the Structure First So the first problem to solve here is structural: aggregating those super funds into one fund. There are a couple of issues:

First – find your super. You may have moved a few times and not sent a forwarding address. You probably have forgotten one or two funds you had whilst working part time at uni. The stories are not unique (I had 4 funds at one stage, The Princess had six) – the government helps here with SuperSeeker. Simply type in your name and date of birth and Tax File Number and it will track down any undeclared super hidden away.

Next – choose a single fund to put them all into. This is a hard one because it depends on your situation, particularly: where you are working and the overall equity balance of your super.

Advertisement

Where you work Contrary to popular opinion, most employees don’t have a choice where their super goes. Public servants are usually forced to use the government sponsored fund (e.g Queenslanders are stuck with QSuper, whilst defence personnel are stuck with the similarly poorly performing Military Super) whilst those in the private sector at major corporations are usually funnelled into large corporate funds with similar constraints, or perverse incentives as part of their remuneration (e.g additional employer contributions into super, but ONLY with their mandated fund).

If you fit one of these areas and are reluctant or unable to change your fund, change your current allocation option to cash (I’ll explain why in a later post) and aggregate your other funds into it.

Be careful too with private employer funds as they may have an insurance package that you will lose if you opt out (usually income protection). At this stage, most people do not require substantial insurance (it becomes more important when you have a dependent spouse or children, or large mortgage debts), but it’s something to look out for nonetheless.

Advertisement

Balance

If your total super – across however many funds – amounts to less than $50,000 or so, then the focus should be on finding the lowest cost fund with the highest performing cash option.

Why? Because to be frank, your super at this stage is basically a savings account. Allocating any funds to extremely risky options like shares, property and infrastructure exposes your small balance to high volatility. This is usually not a problem (volatility is good – it allows you to buy on the low side and sell on the high side – volatility is not risk), but with non-self managed super funds, your fund will actually record your balance down when the underlying asset goes down in value.

This is because they are effectively trading your super on the market and need to “mark to market” their results. So if the ASX200 goes down 9% (as it currently stands from the mid-April high), then your super balance (invested in equities) will be marked down 9% and you will realise this loss. This is the difference between risk and volatility – the risk with non-self managed super is that the volatility “losses” are realised. This has a huge negatively compounding effect on your equity over the lifespan of your super – measured in decades.

Advertisement

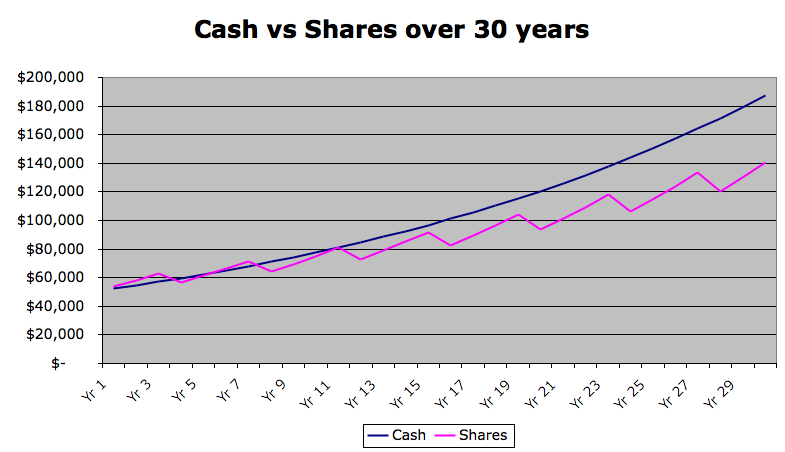

Here’s an example. Suppose you had $50,000 in super. Your cash option is a paltry 4.5% per annum, whilst your share option seems to “average” 8% growth – but with volatility of a 10% loss every four years. What would be the result (assuming no fees – remember the share option management fee would be about triple the cash fee)

Cash vs shares over 30 years

The effect of losing even 10% of your super in one year with 30 years of accumulation to go is more devastating than “missing out” on the 3.5% extra annual gain – if stock markets can do 8% per annum (which they don’t – but that’s for another article).

Advertisement

Choice – where to find comparisons? This can be very frustrating, but when you consider your super as basically a savings account, choosing the right one becomes a lot easier. There are some websites that help rate the performance of the myriad super funds, SuperRatings is the standout. They have an easy function to search the top 10 funds by asset allocation/investment choices.

As of today, it appears the best results for cash (over a five year period) are:

Top 10 funds with best cash options

Advertisement

Update on Cash Choices

Readers John and Ben enquired to the composition and low returns of cash funds in super, in comparison with non-super retail cash returns. I’ve had a closer look at the top 3 funds mentioned above and here’s what I found:

Tasplan – use the Colonial First State Wholesale Premium Cash Fund, which mainly invests in 30-60 day deposits. Charges 0.41% per annum

FuturePlus – uses the QIC Cash Enhanced Fund (same as QSuper) which invests in AA rated credit (short term deposits). Charges 0.3% per annum

HOSTPLUS – unsure (website is very unhelpful, which is usual, but a quick call and they were helpful) After delving through 52 pages, it appears the managers are JPMorgan Chase and ING. 0.05% cost ratio which is very cheap.

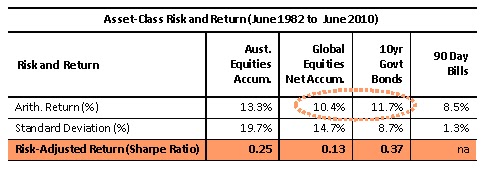

Effectively all of them are following the UBS 90 day Bank bill index. For an idea on how this asset class has performed over the long term, check out the table below, constructed from Morningstar data. (h/t Chris Joye)

For now, forget about choices like “diversified fixed interest” or “enhanced cash” or similar – even if they look more stable. I’ll explain in a later article why cash is your best option at this stage.

Aggregating

So you’ve found all your super funds, you’ve made the choice of which one to put it into (cheapest and best cash option) now how to get them all together. Be prepared to having to wait weeks or months for the administration side of your old super funds to get their act together, mainly due to recent Anti-Money Laundering Legislation, but also because of reluctance of handing back “your” money. This is where big and concentrated funds make no sense – just like the banks and energy companies, customer service is woeful.

Advertisement

You will need certified copies of your identity – find your nearest Justice of the Peace and nearest photocopier and run off copies of your driver’s license, passport and utility bills. Make sure the JP certifies them correctly – super funds are notorious for handing back “failed” declarations of identity, just for a misspelled word or an illegible handwriting (or scanned picture of your mug on your driver’s license).

Non-SMSF choice for Gen X Self Managed Super (or DIY or SMSF) is not for everyone, but should be for everyone. The system should be simple enough that anyone with a Grade 10 ability in maths and finance can run their own fund, but instead layer upon layer of lawyers, accountants, auditors and financial advisers are required to administrate what is effectively a savings account.

If your aggregated balance is nudging $100,000 more than $50,000 I would certainly consider this route, but only if you have the time and psychological wherewithal to step up to this superior option. Self Managed super can be costly, frustrating and poor performing if not managed properly. If you have difficulty with your other personal finances I would steer clear.

Advertisement

One of the greatest benefits of self managed super is the ability to get the gains of high risk assets like shares but hedging the volatility, and of course the flexibility that is unparalleled. These and other reasons are why DIY super is the biggest and best performing of all the super choices. More on that later.

Asking a financial planner Bamboozled finally asks, what about seeing a financial planner? To be frank, with small super balances and the power of the internet, you can sidestep this option for a few (or many) years. When circumstances change – particularly a larger balance in your super, a much higher income, marriage, having children or take on large amounts of debt, then coming up with an integrated financial plan that includes super makes sense.

This article is in a series regarding “The Trouble with Super”, with an introduction and explanation of what to be covered here. New articles will be posted weekly/fortnightly.

Advertisement

Disclosure: The author is a Director of a private investment company (Empire Investing) and a former financial planner. The article is not to be taken as investment or general advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.