Much news and analysis has been made regarding the level of public debt around the world, particularly in the so-called PIIGS (Portugal, Ireland, Italy, Greece, Spain) European nations, although the US and the UK are in similar shape quantitatively. More than enough news has been made regarding Australia’s public debt, which is paltry in comparison, although rising.

But private debt – that held mainly by households – is the elephant in the room. And in Australia’s case – its a large silver elephant, as we have the 2nd largest private debt to household ratio in the world (Netherlands is No.1, with Korea and UK slightly behind).

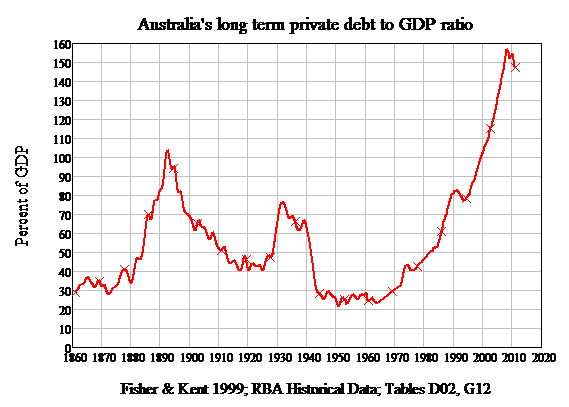

Measured differently as private debt to GDP (as public debt is measured), the growth in private debt is stark:

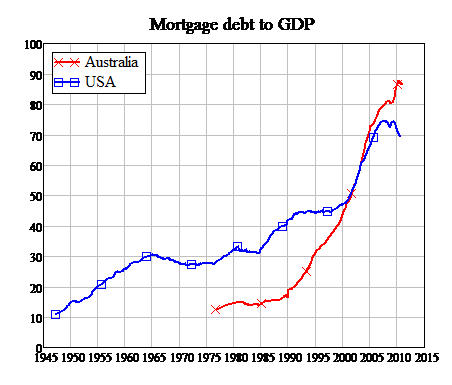

What makes up this debt? Obviously, the majority is housing, which has now surpassed the US’s gluttonous appetite for mortgage debt:

The remainder is personal debt, i.e credit cards, hire purchase loans, car/personal loans etc. Recently, the RBA announced that Australian households owe nearly $50 billion on credit cards, having grown 42 per cent in the past 5 years, with $36 billion of that total accruing interest (at an average interest rate in the high teens).

Is this level of private debt as concerning as the public debt dramas facing the PIIGS? The levels are similar, and the impact on the economy is felt sharply if debt-consumption based spending decelerates or goes into reverse. MacroBusiness bloggers have made this case, particularly the link between housing and retail (here), the “Godzilla” effect of interest rates and inflation (here) and the comparison between the US and Australia (here). The issue of whether or not this level of private debt can continue has been analysed thoroughly by Steve Keen.

As an investor, my question is: how can we profit from this situation?

Defining Debt

The conventional classification of any type of debt – public or private – is that it is someone else’s asset. Therefore to learn how to profit from debt, you need to find out who owns/originates it and how much of a return they are making on that asset. The extension of this equation is who do the owners of the debt turn to, to get a return of their asset, when consumers get into trouble paying the loan?

The Banksters

Previously, I’ve covered the big four banks, the largest originators of debt, and hence owners of these assets in Australia. A quick overview to place them in context of other listed businesses I will cover for the remainder of this post. In terms of returns, the banks average 12-18% Normalised Return on Equity (NROE – includes return an investor gets from franking credits) and are at low Price/Earnings (PE) ratios, averaging 10-11 times. The banks are the “Godzilla”s of debt profiteers in Australia, with a very strong concentration on residential mortgages.

Other Mortgage-related Companies

The “four pillar” policy has created an oligopoly of large, concentrated banks, with little variation on the theme. But there still exists smaller banks and lending institutions, particularly within regional Australia. Suncorp Group (SUN), Bendigo and Adelaide Bank (BEN) each face higher funding pressures than the big four and as a result have lower margins and profitability, with NROE at barely 5% for SUN and just over 10% for BEN. Although Suncorp is Australia’s 5th largest bank, its also a major insurance group, diversifying its revenue, but this has been hit hard by the Queensland Floods and poor management. BEN’s merger is still being swallowed as ROE drops and cost to income remains high. Both regional banks are not worthy of investment grade.

QBE Insurance Group (QBE) is a company worth mentioning as it has extensive exposure to the banks’ residential mortgage lending books, through the origination of its LMI. Lender’s Mortgage Insurance is obligatory for non-prime (my definition) loans with deposits of less than 20%. Some consumers get confused that this insures their mortgage in case they default, whereas the reality is the mortgage is insured for the bank – remember its their asset. Given that QBE has poor Return on Equity (less than 11%) and substantial reinsurance and other risks, I’ll be going over this company in a separate article.

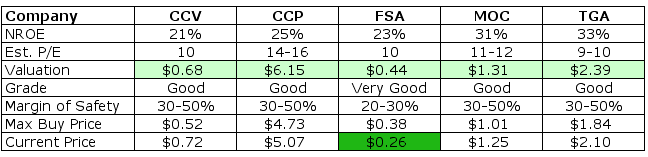

Mortgage Choice (MOC) is an independently owned mortgage broker that has toughed out the GFC and recent changes to mortgage origination regulation. It has very high ROE at 30%, although this has declined from pre-GFC 50% plus highs, a direct correlation with overall mortgage growth. The balance sheet is quite sound, with no debt, strong cashflow and very good capital management. The risks facing MOC are clear: they are directly exposed to any housing turndown. As I mentioned in my “Peak Profit” article, mortgage growth has decelerated (after reaching the “magical” $1 trillion mark) to around 4-6% annualised. Will this be enough for MOC to continue to grow in the future? Consequently, we value MOC at $1.31, but with a maximum buy price of $0.87 (50% Margin of Safety).

Debt Servicing Companies

Now to my favourites. Empire Investing prefers small-cap stocks, that is, companies with relatively small market capitalisations that are often ignored or treated with disdain by mainstream brokers and research houses. Thankfully, this is where the performance is, as I covered in my fund management post, as the Small Ords Index (which covers the “bottom” 200 stocks below the top ASX100) has outperformed the so-called “blue chips” for the last five years.

There are two groups comprising four stocks that I’d like to cover.

The first two, Cash Converters (CCV) and Thorn Group (TGA), are involved in the consumer appliance rental and unsecured personal loan markets, thus capturing a large amount of non-mortgage related consumer debt. TGA is the owner of Radio Rentals and other business related rental services. They recently announced a 7.5% increase in customers moving towards rental of appliances, instead of purchase (either outright or using debt). TGA have also expanded into personal loan services, with their loanbook doubling in the last six months. TGA’s balance sheet is quite good, and its ROE is double that of a bank at over 30%, whilst the P/E ratio is similar.

CCV is a well known brand, with a core business of retailing second hand goods which has proven profitable in both boom and bust periods. However, a major part of CCV’s business are unsecured personal loans, with loan book growth of 48% in the last six months. This is providing solid revenue growth to its bottom line. CCV is well positioned to grow the business and has been resilient to the business cycle due to its somewhat-controversial operations. Its balance sheet is strong, with no debt, hardly any intangibles and relatively high ROE of 21%.

Credit Corp Group (CCP) is a purchaser and manager of debt ledgers – i.e debt collectors. CCP acquires these books from various institutions and credit providers and creates collection and fee incomes as a result. Needless to say, business is a booming for CCP with net profit quadrupling in the last 4 years. In a recent market update, CCP announced a substantial increase in net profit (up 58%), a large increase in debt ledger acquisitions and expansion into New Zealand (which also “suffers” from high household private debt). CCP’s balance sheet is very good, with modest debt, strong cashflow and increasing ROE – currently 26% and forecast to rise to 29% next year.

FSA Group (FSA) is the largest provider of debt solutions to individuals and businesses in Australia. FSA organises debt agreements (DA) (and sometimes insolvency agreements and bankruptcy assistance) between creditors and debtors and collects a monthly fee. The average duration for the DA is 4.5 years, providing extremely strong and liquid cashflow to the business. Notably, FSA is almost a monopoly player in this niche market, with 51% of the market and due to recent regulatory guidelines requiring new entrants to provide extremely high levels of capital, an effective barrier to entry has been created. This area of FSA is forecast to grow at an 8% annualised rate and provides very high ROE for the business. With more and more Australians struggling to pay their debts, FSA is well positioned.

FSA also has a large financing division. This includes a broking section which assists clients with property to consolidate their debt using equity in their homes and a recently launched lending section provides both prime and non-conforming home loans whilst the factoring finance section provides credit solutions for businesses. The loan book is relatively modest at $200 million and surprisingly high quality, with an average LVR similar to CBA at 67% and relatively low size loans averaging $200K. This implies that the clients are at the bottom end of the housing market, not in the volatile mid-range. FSA says that loan origination is done organically, and does not rely on brokers as clients call them for assistance.

FSA has an excellent balance sheet, with modest debt, high free cashflow and excellent capital management. However, due to high funding requirements for its growing loan book and the reinvestment of capital into the debt agreement/servicing business, it does not pay a dividend. This has weighed on the share price, as the Australian investor is as addicted to dividends as it is to debt, even though FSA has a return on equity almost double that of a bank, at half the cost (P/E ratio of 5). It is the standout player in the debt profit market.

Valuations

Q Continuum will post an Equity Spotlight article on one of the above companies, providing a full detailed valuation, later in the week.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has an interest in some of the businesses mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.