I’ve said before that investing is more about psychology than about fundamental valuations, numbers and metrics. In the case of residential property’s evil “twin” brother, gold, this is more true than ever. Regular readers know that I am watching out for signs of the current bull market in gold becoming an out of control bubble. In my previous article on gold, I discussed two new developments (central banks buying gold, gold mining executive saying “the fundamentals no longer apply”) and now today I bring two more plus a visual case that the trend may not be over.

Soros turns around 360 degrees

George Soros, the 80 year old billionaire who is on record as saying that “gold is the biggest bubble ever”, recently sold his $800 million SPDR Gold Trust ETF stake in the precious metal (derived from regulatory disclosure documents)

George Soros sold most of his holdings in the bullion-backed SPDR Gold Trust and iShares Gold Trust funds in the first quarter, while buying shares of mining companies Goldcorp Inc. and Freeport-McMoRan Copper & Gold Inc.

Soros’s fund held 49,400 shares of SPDR Gold Trust as of March 31, compared with 4.721 million at the end of the fourth quarter. The New York-based fund sold all 5 million shares it held in iShares Gold Trust. Soros bought 301,300 shares of Freeport-McMoRan and 7,600 of Goldcorp.

Speculation as to this move by the well known guru is very bullish, as explained here by GoldCore:

There is of course the precedent of other hedge fund managers , such as David Einhorn, who have also sold their gold ETF holdings but bought physical bullion in allocated accounts due to a concern about counter party and systemic risk.

It is quite possible that Soros’ fund has adopted a similar strategy.

This would allow Soros to discreetly accumulate bullion away from the public and media spotlight that result from SEC filings.

Soros has admitted he is in no longer in the “deflation” camp, regarding inflationary pressures as the greater probability. So far his take has been correct, with recent inflation figures from the EU, UK and US “surprising” economists and commentators alike, as very low interest rates and QE programs around the world continue to take their toll on monetary stability.

Interestingly, Bill Gross’s PIMCO – which recently dumped all of their US Treasury positions – is now a bullish proponent of the shiny metal. PIMCO’s new $1.2 billion equity fund has announced its largest position is actually in gold, for “protection against what can go wrong.”

HK Gold Trading

This development is very relevant for Australian institutional and retail investors alike:

The Hong Kong Mercantile Exchange (HKMEx) has received authorisation from the Securities and Futures Commission and will make its trading debut on May 18, 2011 with the 1-kilo gold futures contract offered in US dollars with physical delivery in Hong Kong.

The ATS authorisation grants HKMEx the right to offer market participants, through its member firms, the use of its state-of-the-art electronic platform to trade commodities. The Exchange will begin trading with at least 16 members including some of the world’s largest financial institutions as well as several well-established brokerages in Hong Kong.

The initial debut yesterday was very quiet, but is expected to pick up in trading volume. This provides gold with better competition in world markets, as the previous sole supplier of tradeable contracts – COMEX in the US – has been notorious for hiking margin requirements during surges in precious metal (particularly silver) prices, which has definitely not added to price stability. It is unclear whether HKMEX will act in a similar manner with it predominately Chinese clients.

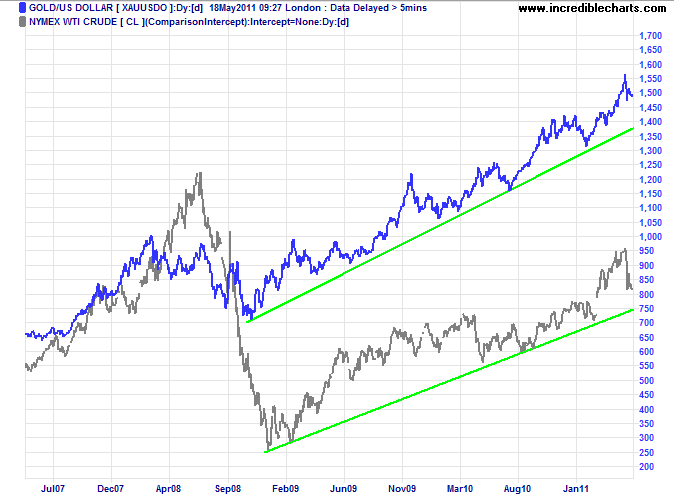

Gold and Oil megatrends

I’ll finish with this very interesting chart from Colin Twiggs (Disclosure: I use his charting software, but receive no payment in kind for showing it here)

Astute readers will notice the trendlines begin around the time of the Lehman Brother’s collapse and subsequent Wall Street bailout in 2008/9. It also covers two runs of Quantitative Easing and “lite” versions in between, and shows remarkable resilience. This chart highlights how the very concept of inflation is hard to define: is price rising because of increased fundamentals (less supply, more demand) or because of an increase in the supply of money itself without a commensurate rise or deterioration in the underlying fundamentals?

Whilst both commodities have undergone a correction in the last month, the bulls will wager that this healthy within a bull market phase. But is this market still reliant upon uncertainty and continued QE from the Federal Reserve to continue its “inexorable” rise?

Disclosure: The Prince is a full time equities trader, occasionally trades non-physical gold (both long and short) and holds physical gold as part of his family superannuation fund. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.