Asset markets are effectively all the same: housing, shares, commodities, FX, precious metals, pork bellies and interest rates. They are all markets for speculators to trade, investors to get a return of and on their money and sheep to think they can buy and hold (or negative gear) forever.

As I’ve said before, gold in its non-physical form, is no different to those above. Its price is moved in the short term by speculation, just like everything else, and made easier by the proliferation of ETF’s and ETC’s.

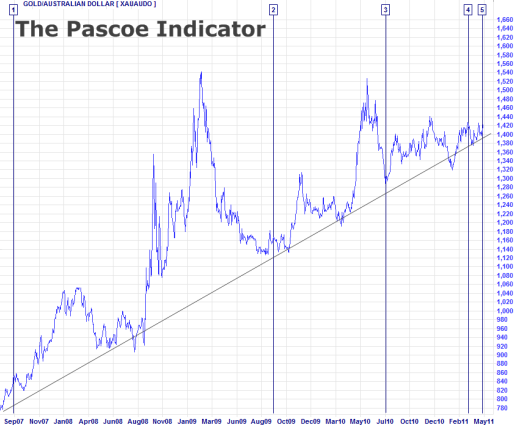

To be sure, I’m no Michael Pascoe or other MSM haters who wish to bash gold-bugs over the head, and provide them with a “gold” contrarian indicator to buy back in again. (h/t Bullion Baron)

Vertical lines represent dates of Pascoe's bearish gold articles. From the Bullion Baron

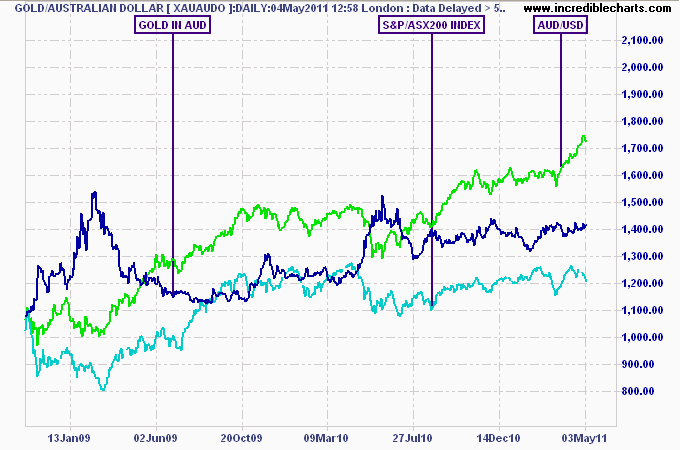

Pascoe has a point though – like the ASX200, gold in AUD has not moved appreciably in the last 12 months, as AUD/USD appreciation negates the robust returns in spot gold in USD. And anyone who bought gold in the dying days of the GFC in AUD is still waiting for their “return”.

At MacroBusiness, we are empirical observers of what is happening, not what should be happening according to models, pet or conspiracy theories. And it is clear that, at the very least, gold is in a exuberant investment phase that is accelerating and two new signs have just appeared that could reinforce this perception.

A Brown Top

Former Prime Minister Gordon Brown infamously sold the majority of the central banks gold reserve whilst Chancellor in 1999, at was then the almost exact bottom in gold’s price. Other central banks performed similar disposals, including one Peter Costello who sold the majority of the RBA’s gold, some 167 tons in 1997 at a paltry $US340 per ounce.

Now there is clear evidence that the central banks are back buying gold – is this a countercyclical Brown top?

From Bloomberg:

In 2010, central banks became net buyers for the first time in two decades, adding 87 metric tons in official-sector purchases by countries including Bolivia, Sri Lanka and Mauritius, according to World Gold Council data. China, with more than $3 trillion in foreign-currency reserves, plans to set up new funds to invest in precious metals, Century Weekly reported this week. Russia purchased 8 tons of gold in the first quarter.

Central banks in emerging markets may aim to hold 2 percent to 8 percent of their foreign-currency reserves in gold, Francisco Blanch, the head of commodities research at Bank of America Merrill Lynch in New York, said in an interview.

Gold is “close to” its cyclical high, said Blanch, who expects the metal to average $1,500 this year.

What may preclude these purchases from being bearish on gold (in USD terms) is most of the buying is by nations who wish to diversify out of the weak and continually debasing USD. This could also be the start of a new monetisation of gold amongst a new reserve currency basket, but this is just speculation.

The Fundamentals no longer apply?

What was the most oft-heard quote during the NASDAQ bubble, as P/E ratios hit triple digits, or were as non-existent as the underlying earnings? This time is different. What was the most heard phrase during the Southern European debt orgy? The EU is different, the fundamentals don’t apply. And as the great Australian housing bubble slowly hisses?

Any careful, rational observation of past hysterias, bubbles and “madness of crowds” shows a 100% failure rate after the words “this time is different” or “paradigm change” are uttered. In gold’s case, there maybe an element of truth, as the “old” fundamentals, i.e. gold’s non-utility as a currency or monetary standard (only 40 years “old” by the way) have a chance of reverting to the ancient fundamentals in a “paradigm” reserve currency move away from the USD.

From MiningWeekly (my emphasis added):

The traditional supply and demand fundamentals that have determined the gold price in previous decades no longer apply, Barrick Gold chairperson and founder Peter Munk asserted on Wednesday.

“Gold today is no longer related to a normal economic cycle of supply and demand, jewellery and Indian wedding seasons…” he said.

“All those things are passe, forget about them.”

Gold is being driven by “a fundamental, global and growing insecurity, a fundamental, global and growing lack of confidence of the world in everything they were brought up to believe in”.

All this means that “gold’s future is assured”, Munk said.

Summary

I’ve outlined two possible signs amongst other evidence that derivative gold prices (in USD) maybe further along the “exuberant” phase of a bubble than first thought. Like other asset classes, particularly property, gold has its boisterous supporters ready to confirm their bullish bias and rightly feel indiginant when this evidence is scrutinised rationally. Is it then time to then stand aside, take profits or even contemplate a short of the shiny metal?

Paradoxically, it may be time to explore how to best go long gold, and particularly for holders of AUD. In my next article, I’ll explain my methodology on how to both hedge and trade gold, covering the available products and investment strategies.