Back in December, I wrote the following:

In the early-1990s, non-bank lenders entered the Australian mortgage market and began raising funds via securitisation on wholesale debt markets. The rise of these non-bank lenders caused an intensification of competition amongst mortgage lenders. With no formal regulator and no rules outside of regular trade practices and corporations law, they led the decline in Australian credit standards by introducing ‘innovative’ loan products like low-doc loans in 1997, then ‘no-doc’ loans in 1999, and more recently they were beginning to issue ‘non-conforming’ (sub-prime) loans just before the GFC intervened.

Faced with this new competitive threat, Australia’s banks responded in kind by reducing their deposit requirements and tapping new sources of funding offshore, much of it short-term. Gone were the days of requiring a minimum 20% housing deposit and restricting home loans to an amount that could be repaid with 30% of a household’s gross earnings. Instead, banks accepted 5% housing deposits and lent households an amount that, after loan repayments, left them with just enough money to ensure that they stayed above the Henderson poverty line.

The massive increase in the availability of credit sporn from this increased competition, combined with unresponsive housing supply, has resulted in the housing bubble that Australia experiences today….

The funding models used by the banks and non-bank lenders alike to fund housing were found to be unsustainable after the GFC. Both the banks and non-banks had a dangerously high reliance on short-term wholesale funding, which seized-up amid heightened risk aversion during the GFC. The non-banks and many smaller APRA-regulated institutions were also heavy users of securitised debt markets, which similarly froze-up post GFC. As such, the Government was called upon to guarantee banks’ wholesale funding and buy up to $16 billion of residential mortgage-backed securities (RMBS) in order to ensure that credit continued to flow into Australia’s housing markets, thus keeping the housing ponzi alive.

Today, we received further confirmation in the Fairfax press that the pre-GFC practice of banks borrowing heavily offshore to feed Australia’s housing bubble is becoming unviable.

JANUARY and February are usually the biggest months for banks to raise funds on global markets, but pricing for debt has skyrocketed since the end of last year.

This does not bode well for home owners. Banks are likely to come under further pressure to continue raising interest rates — even if the Reserve Bank keeps rates on hold.

Intense competition for funds from cash-strapped European governments and other banks has been increasing borrowing costs on global markets. The banks commonly blame this for forcing interest rates higher on loans….

Credit market jitters — mostly linked to lingering concerns of default by Portugal, Greece and Ireland — have coincided with the period that is traditionally the busiest for Australian banks borrowing from wholesale markets.

Australia’s big banks will need to borrow more than $130 billion from local and overseas markets in the next year to help fund their lending books. Global pension funds, including Australian superannuation funds, are the biggest investors in bank bonds.

But billions of dollars in funds already raised by banks including Commonwealth, ANZ and National Australia Bank since the start of the year have been costing more than this time last year….

Locally, Commonwealth Bank has the biggest requirement from wholesale markets, eyeing more than $50 billion over 2010-11. Westpac is looking to raise as much as $35 billion and NAB is looking to borrow up to $30 billion. ANZ plans to raise $20-$25 billion…

Greg Canavan from the Daily Reckoning today published some nice analysis of the funding pressures now facing Australia’s banks and the implications for house prices and the Australian economy.

The banks are now competing for capital with bankrupt governments. Markets are demanding a higher rate of interest to lend to these governments so in turn, the banks need to pay more.

After many years of not caring, debt markets are starting to price risk sensibly…

This has important implications for the Australian banking sector and the economy. A higher cost of credit means we probably won’t see a rebound in lending anytime soon. Banks won’t expand their balance sheets, which means their share prices will stagnate.

Even worse though, the higher cost of credit will hurt the property sector. Over the past decade, cheap and plentiful credit has propelled the property market higher and higher. Based on capital city prices, Australian residential property is one of the world’s most expensive.

But with credit now coming at a higher cost, you will see house prices begin to fall. Residex recently reported that Australian capital city house prices fell an average of 1.1% in December, with year on year gains of 5.1%.

That annual gain is less than the cost of funding, so in real terms property investors are going backwards.

Remember, property is a highly geared investment, so even small falls can have a major impact on investors’ equity.

This will put further pressure on the banks and balance sheets of a highly indebted household sector.

The equity market is not the only asset class topping out. Residential property is joining in. Will there be a crash though? Maybe. But we think that will only happen if unemployment starts to rise.

The two income household is one of the major drivers of property prices. As long as there is employment income to service debt, you probably won’t see major price falls.

But here’s a twist. Australia’s extremely low unemployment rate has come at the expense of declining productivity. We may be near full employment, but as a group we’re becoming less productive.

A big part of the reason for this is that Australia has over invested in property, an unproductive asset. The balance sheets of the big four banks are overwhelmingly tilted towards residential property. As a percentage of Australian assets, the average is somewhere around 65 per cent.

So the majority of money borrowed by banks (from you, the depositor, and overseas lenders) goes into housing. This does not increase our productive capacity.

Along with the benefits of the China boom, this is why there is fear of a wages breakout in Australia. And this is why Glenn Stevens at the RBA still has his finger on the interest rate button despite numerous signs of a weak domestic economy.

Wealth is many things but it’s not higher asset prices pushed up by cheap credit. Tops are beginning to form. It’s time to be conservative.

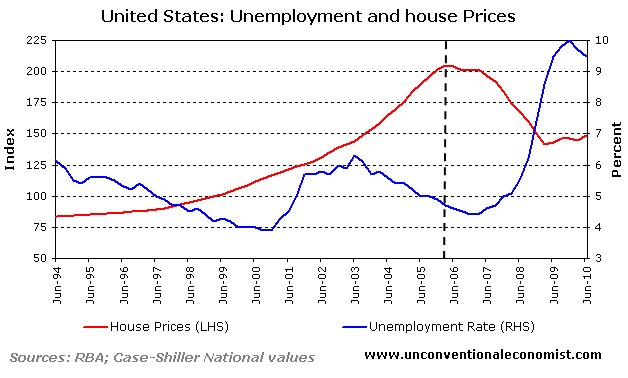

Nicely put Greg. I agree with everything that you have said except for one point: that Australia needs unemployment to rise before house prices will fall. This certainly was not the case in the United States, where house prices fell for a year before unemployment began to rise (see below chart).

The reason why falling house prices would likely lead rising unemployment is actually quite logical. When house prices rise, Australians feel richer, which spurs consumer confidence, spending and employment growth. A positive feedback loop often develops whereby households take on more debt, causing housing values to rise further and the process of confidence, spending and employment growth to repeat.

But home values and debt levels can only rise so far and, sooner or later, the process of debt feeding asset prices feeding confidence, consumer spending and employment growth goes into reverse (i.e. deleveraging). House prices stop rising (or fall) and highly-indebted households begin to reduce their spending and repay debt. Sectors reliant on consumer spending contract and unemployment rises. Consumer confidence falls, leading to further frugality, house price reductions and job losses.

I believe Australia is currently at the early stages of such a deleveraging process.

Fellow blogger, Financial Follies, appears to share similar sentiments. Today he wrote an excellent article on some of the risks facing the Australian economy. Here is some of what Financial Follies had to say:

…You might have read reports of a recent study by the IMF, which surprisingly concluded that Australian house prices were only mildly overvalued. The IMF argued that there were solid fundamental reasons for Australia having the most expensive property prices in the world. And one of the key reasons they cited is the massive rise in Australia’s terms of trade.

You can see from the chart below that, indeed, inflation-adjusted house prices have basically increased in line with Australia’s terms of trade over the past two decades.

This raises an obvious question. If you agree with the IMF’s logic, doesn’t this imply that house prices have to fall when the once in a generation boost to the terms of trade reverses?

Now, Australia’s terms of trade has gone through long rises and falls over history without huge problems. And a decline in the terms of trade wouldn’t necessarily have to be a big problem if Australia had invested the proceeds of the current boom productively. But instead, Australians have turbocharged the boom by taking on record levels of personal debt (see below), mainly to purchase houses. And the Australian banks are financing a good part of this mortgage debt not through deposits, but through a potentially unstable source of funding: the international bond markets.

So we are now left very highly leveraged, and the valuation of the biggest asset that most Australians own (their houses and investment properties) as well as their ability to service this debt (and the banks’ willingness to keep extending credit) is dependent on the continuation of the commodity boom. The enormous level of personal debt means that Australians today are highly vulnerable to potential shocks in the economy, whether from a slowdown in China, or from higher interest rates.

The chart below, from an excellent post at deflationite.com, shows just how unbalanced the Australian economy has become over the past two decades. You can see that in 1990, the majority of Australian bank lending was being channeled into business investment, or investment in Australia’s future productive capacity. But over the past two decades, the portion of bank credit allocated to business investment has steadily shrunk. In place of this, we have seen massive growth in property-related lending, to the point where one in seven Australians today owns one or more investment properties.

In essence, Australians have been behaving as if the commodity boom and the days of easy credit will last forever. Nobody can predict the timing, but they won’t. Now, that doesn’t have to mean disaster, but we’re kidding ourselves if we think the adjustment is going to be easy.

As explained by the above bloggers, there are clearly significant downside risks to the Australian economy and housing market. Anyone extrapolating the past decade’s performance into the future is likely to be sorely disappointed.

Cheers Leith