Earlier this week, Alan Kohler wrote an article in Business Spectator on the misery created by the Irish housing bubble/bust and its lessons for Australia:

After 2002, when Ireland joined European Monetary Union and adopted the euro, the two things combined to create a massive property boom and, in essence, the government was able to replace corporate taxes with much more revenue from property taxes.

Between 2000 and 2008, the state pension doubled, average public service salaries increased 59 per cent, the standard income tax rate fell from 26 per cent to 20 per cent and the top rate from 48 to 41 per cent.

Despite this, Ireland, like Australia, entered the global financial crisis with low public debt. But its prosperity was built on the quicksand of a property bubble.

In 2007, stamp duty and capital taxes yielded €6.7 billion; this year that will fall to €1.6 billion. As a result, the budget deficit has ballooned to 11.7 per cent of GDP, even after big spending cuts in the past two years, and gross public debt is suddenly at 95 per cent of GDP, rising to 102 per cent in 2013…

The bigger problem was Charlie McCreevy who, as finance minister in two stints during the 90s and then again 1997, disastrously cut taxes and increased government spending.

Specifically, in 1997 he cut the capital gains tax rate from 40 per cent to 20 per cent and extended property tax concessions, which directly led to the explosion in property speculation, which in turn led to the collapse of the Irish banking system.

When the boom ended, government spending went from 28 per cent to an unsustainable 44 per cent of GDP.

Ireland thought the property boom would last forever and lived it up. Yes, the boom was created by out-of-control bankers and rich speculators, and the politicians took the government along for the ride, but in the end that doesn’t matter. Government spending now has to be cut even if bank bondholders are forced to lose their shirts.

Needless to say, the Australian government should learn from Ireland’s mistakes.

Indeed, in 2004 Ireland was the toast of Europe and one of the world’s wealthiest countries:

Ireland is one of the world’s wealthiest countries since its economy has grown nearly five-fold since 1973. It boasts one of the world’s highest levels of GDP per capita, some 20 percent above the European average—while 30 years ago it was 35 percent poorer than the average….

Ireland’s economic growth model has been hailed as an example of development done right, with everyone from professors in Pittsburgh to investment agencies in Armenia trying to figure out how to replicate the success of the Celtic Tiger.

And in 2005, The Economist judged Ireland to have the best quality of life in the world.

How things change. Once house prices began deflating, the world discovered that Ireland was not so special after all and that their economy was just another unsustainable credit bubble that burst violently.

The below chart shows the extent of Ireland’s housing bubble/bust:

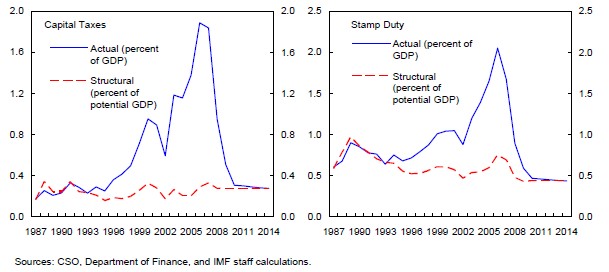

And the below IMF Charts show the extent of Ireland’s dependence on property taxes and how these sources of revenue have dried-up:

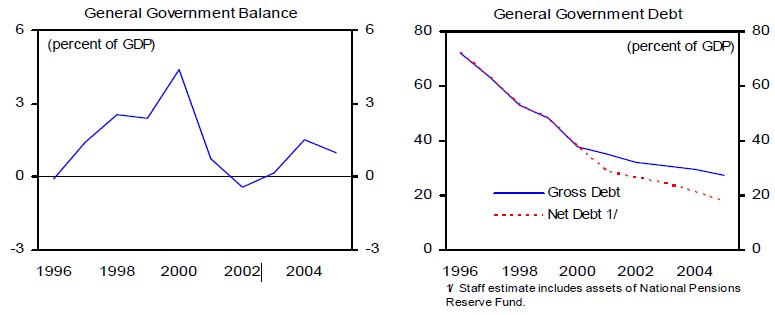

Not surprisingly, given the spikes in stamp duty and capital gains taxes between 2005-06, Ireland’s public finances were looking pretty good prior to the onset of the Global Financial Crisis (see below IMF charts):

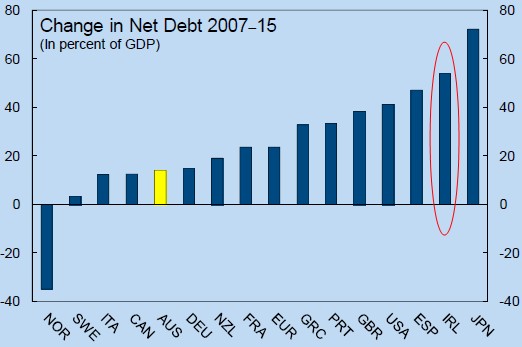

However, following the collapse of property taxes and the costly bail-out of its banks following the bursting of its housing bubble, Ireland’s net debt has exploded. In fact, the IMF forecasts that Ireland’s net debt will increase by around 50% of GDP over the period 2007 to 2015 (see below IMF chart).

Now Ireland’s economy is experiencing its third year of recession in which its unemployment rate has risen from under 5% to nearly 14%:

Ireland has been following a self-imposed stark austerity program for almost two years, cutting public spending and raising taxes. Despite this, the budget deficit remains at around 14 per cent of GDP, as the sharp contraction in the economy has caused tax receipts to collapse. At the same time, the Irish government faces a higher spending on social security benefits now that the country’s unemployment rate has climbed to 13.7 per cent. Fears that the Irish government will struggle to reduce its borrowings has pushed the interest rate that Ireland pays on its benchmark 10-year bonds close to 300 basis points more than comparable German bunds.

So what caused Ireland’s property bubble and what lessons does their predicament provide for Australia?

The usual suspects:

As is the case with all housing bubbles, Ireland’s was fuelled by two inter-related culprits: easy credit and speculation.

A recent article by Saul Eslake provides a nice explanation of how low interest rates and easy credit fuelled Ireland’s housing bubble:

Once Ireland joined the euro at the beginning of 1999, short-term interest rates in Ireland were no longer set in Dublin in accordance with Irish conditions, but rather in Frankfurt in accordance with conditions in the euro zone.

Thus Irish short-term interest rates fell from about 6 per cent, where they had remained during the second half of the 1990s (which the Central Bank of Ireland had deemed appropriate for an economy that had been growing at rates of 8-11 per cent a year) to 3 per cent (which the European Central Bank considered appropriate for an economy that had been growing at about 2.5 per cent a year).

From then until the onset of the financial crisis, short-term interest rates averaged 3.25 per cent a year in Ireland, as they did in the euro zone, even though Ireland’s economy grew at an average annual rate of almost 6 per cent (compared with less than 2 per cent for the euro zone) and Irish inflation averaged 3.5 per cent a year (compared with 2.25 per cent a year for the euro zone).

Because Irish interest rates were substantially lower than they should have been for an economy growing as fast as Ireland’s was, Irish households and businesses borrowed (and Irish banks lent) far more than they would otherwise have done, resulting in (among other things) an unsustainable property boom in which Irish house prices more than doubled in less than seven years (they have since fallen by almost a third).

In order to explain the second cause – investor speculation – I have borrowed heavily from the Ireland Central Bank’s (ICB) 2007 Financial Stability Report.

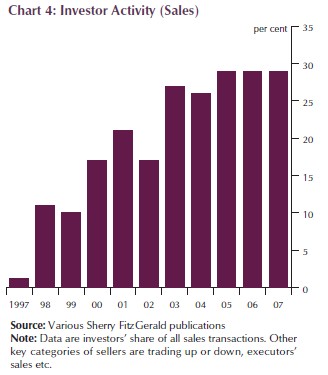

Like in Australia, lending restrictions on investor mortgages were relaxed in the mid-1990s, which enabled property investors to borrow at the same interest rate and on similar terms to owner-occupiers. This led to a surge of property investment, as shown by the below ICB chart.

In fact, as at June 2007, investors accounted for around 27% of total mortgage lending – slightly below Australian investor’s share of 30% of total mortgage lending.

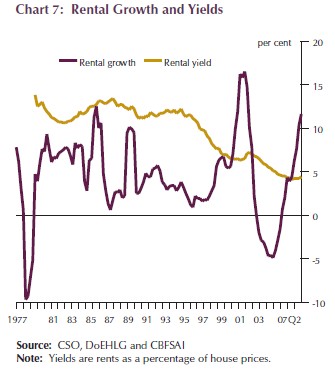

And like in Australia, the sharp rise in property prices prior to the global financial crisis (GFC) forced rental yields down:

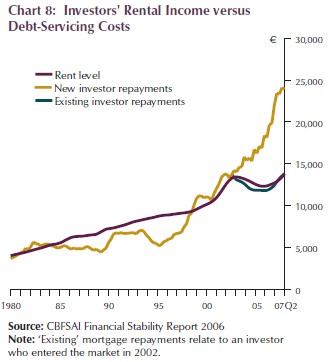

As such, recent investors were cash flow negative in 2007, since rental income nowhere near covered holding costs:

So just as property investors in Australia rely predominantly on capital appreciation to make ends meet, investors in Ireland were doing the same.

However, once property prices began to fall, Ireland’s over-geared investors rushed for the exits, thus helping to force house prices down. The risk of investors fleeing the property market en masse was acknowledged by the ICB in 2007 just prior to the crash:

…buy-to-let landlords, acting as dispassionate investors rather than emotionally involved owner occupiers, might decide more quickly than owner occupiers to dispose of properties in the event of a house-price fall, and this could potentially destabilise the wider housing market. The concern is a mass exodus of investors at the same time would put additional pressure on an already fragile market, causing a quicker downward spiral than would have otherwise been the case.

Still, in true central bank fashion, the ICB rejected the notion that Ireland would experience a sharp housing correction, instead predicting a soft landing due to strong underlying fundamentals:

Regarding future house price developments, factors that will have an influence on the future direction of house prices are investors’ participation in the property market, the sustainability of current rates of immigration and the future direction of monetary policy. The underlying fundamentals of the residential market continue to appear strong, as evidenced by rent increases. The central scenario is, therefore, for a soft, rather than a hard, landing.

Lessons for Australia:

The Australian and Irish economies have some major differences. Most importantly, Australia controls its own monetary policy and has its own currency. As such, it has the ability to set interest rates to stimulate/slow growth and its flexible exchange rate acts to smooth positive (negative) shocks via appreciation (depreciation) of the Australian Dollar.

By contrast, Ireland does not control its monetary policy or currency. The former is determined by the European Central Bank, effectively set by the larger European economies, Germany and France. Likewise, since their currency is the Euro, they are unable to devalue in order to regain competitiveness. In this regard, as long as Ireland remains in the euro, its economic anguish will not end.

Despite the important differences between the two economies, the implosion of the Ireland property market offers some important warning signs for Australia.

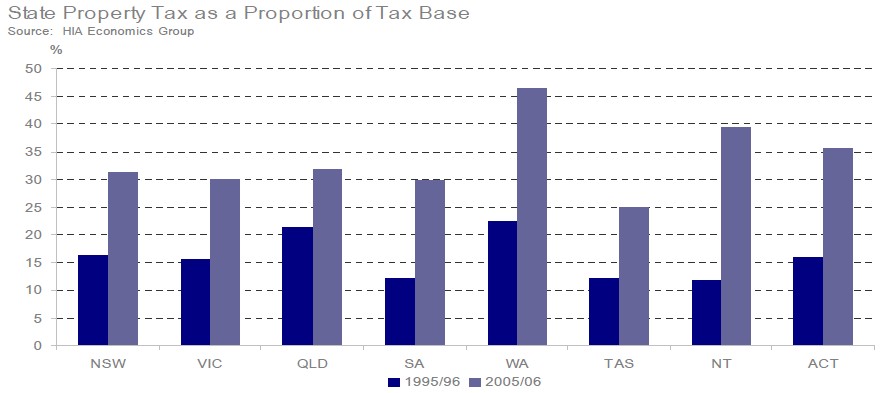

First, like Ireland, Australia’s governments have grown overly addicted to property taxes, which have been largely squandered on tax cuts and wasteful recurrent spending. To highlight this point, consider the below chart showing the growth of state property taxes as a proportion of the tax base.

The story is similar at the federal level where tax collections have surged on the back of growing property values and rising debt levels, which has boosted consumer spending, employment and the economy more generally.

Now you don’t have to be a rocket scientist to predict what will happen if Australia’s housing market corrects – government finances will take a hammering as consumer spending dries-up, unemployment rises, tax collections fall, and welfare payments rise. And the impact will be a whole lot worse should Australia’s other economic pillar – mining – experience a sharp contraction of demand and falling commodity prices.

Then there is the issue of Australia’s large pool of loss-making property investors – 1.2 million of them as at 2007/08. Just like in Ireland, there is the risk that they will sell en masse once they realise that the days of easy capital appreciation are over and house prices might actually fall. This rush for the exits is likely to gather pace as the Baby Boomer’s retire.

Let’s hope that the bulls are correct and the China growth story continues well into the future. Otherwise, the Australian economy is cruising for a bruising.

Cheers Leith