My cousin, Peter van Onselen, writes for the Australian. In my opinion, he is one of the more insightful and balanced commentators on their roster (of course I am biased). Today he published an article explaining the political sensitivities and difficulties of reforming Australia’s housing policy, in particular our overly generous taxation concessions (such as negative gearing) as well as freeing-up the supply-side of the housing market in order to speed-up land release.

…Or what if the government moved to restrict the number of investment properties people could negative gear their incomes against? That might be a way to take some of the upward pressure on prices out of the equation, but it would leave existing investors upset, and there is an argument that it could constrict what is already a tight rental market.

Fewer people investing in property means fewer rental properties available. When supply is already a problem, people in lower socio-economic circumstances don’t need that. [my emphasis]

Given the “negative gearing assists the rental market” claim seems to be getting air-play once more, it’s time for a refresher on why negative gearing is a costly policy mistake that does little to improve the availability or affordability of rental accommodation.

One expensive policy:

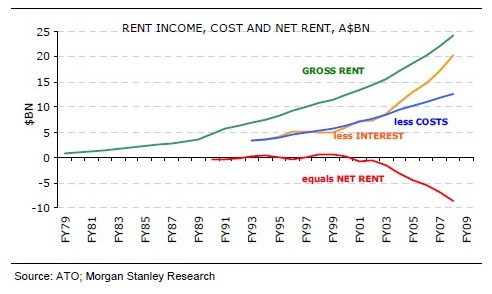

The reintroduction of negative gearing in 1987, in concert with the halving of the Capital Gains Tax (CGT) rate in 1999, led to a surge of property investment in Australia. The below three charts come from Morgan Stanley. The first chart shows the number of taxpayers claiming rental income to the Australian Taxation Office (ATO) skyrocketed from 608,000 taxpayers in 1988/89 to 1,765,000 taxpayers in 2007/08 – 13% of the total.

With house prices booming and rents remaining flat, the proportion of taxpayers where rental income does not cover costs increased from around 50% in 1993/94 to 70% in 2007/08:

This increase in property investment in Australia was also assisted by a significant increase in credit provision to property investors. From the mid-1990s, investors were permitted to purchase an investment property via accessing equity in their own home, without having to contribute any cash up front. Lending criteria on investment loans were also relaxed and became much the same as loans to owner occupiers, as did the interest rate charged. Lenders also began competing aggressively for investment loans and offered products specifically designed to attract investors, such as the split-purpose and interest only loan.

Impact on rental market:

Despite the massive surge of property investors and the huge subsidies provided by Australian taxpayers, negative gearing has done little to:

- increase the availability of rental accommodation; or

- reduce its cost.

The data on new home construction by investors is even more damning. As shown below, there was a surge in investor loans for second-hand properties from around 2000 onwards, coincident with the reduction in CGT. By contrast, loans for new construction have remained relatively flat for the past 25 years. As a comparison, the ratio of investor lending for existing dwellings to new dwellings was around 2:3 in 1985; 7:1 in 2000; and 13:1 currently.

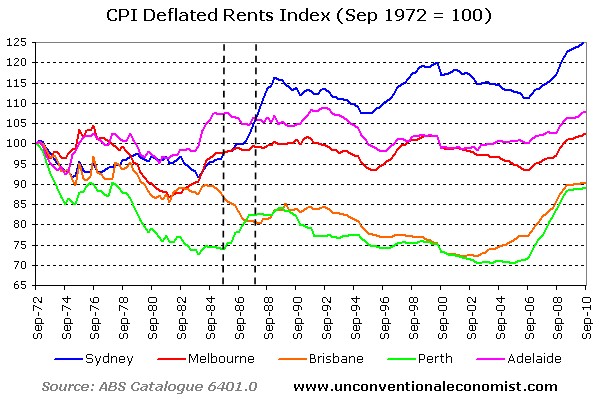

It’s true, according to Real Estate Institute data, that rents went up in Sydney and Perth. But the same data doesn’t show any discernable increase in the other State capitals. I would say that, if negative gearing had been responsible for a surge in rents, then you should have observed it everywhere, not just two capitals.

Based on the above evidence, there is clearly little merit in Australia’s tax concessions for property investment. Negative gearing and the CGT concession do not provided any incentive to invest in new housing because they are available for both existing homes as well as new ones. And since these concessions do not increase housing supply, they also do not put downward pressure on rents.

Cheers Leith