No doubt many readers have heard that the Australian Government is looking to follow Canada’s lead and implement a Government guarantee of residential mortgage-backed securities (RMBS), in order to foster greater competition in mortgage lending and reduce the power of the big four banks.

Following on from David Llewellyn-Smith’s critique of this proposal, I thought it timely to provide an examination of the Canadian Government’s guarantee of its RMBS market, and show readers why adopting a similar approach in Australia is a terrible idea. In doing so, I have borrowed heavily from Canadian financial blogger, Ben Rabidoux, as well as my previous article on the Canadian Housing Bubble.

Canadian Housing Mortgage Corporation (CMHC): the Great Enabler

The government-owned CMHC is Canada’s national housing agency. CMHC works by acting as the guarantor for any mortgage where the purchaser is unable to pay a specified amount as a down payment (20% for residential properties). Essentially CMHC guarantees the full value of the loan so as to protect the lending institution in the event that the buyer defaults on their mortgage and the bank is unable to recover the full value of the loan by selling the home.

For example, imagine a home buyer purchases a $500,000 home with a 5% down payment, leaving a mortgage of $475,000. Since the home buyer does not have the required 20% deposit, they pay CMHC an insurance fee and CMHC then guarantees that they will cover any losses if the borrower defaults, thereby ensuring that the lending institution makes a profit. A year later, the economy enters a downturn causing house prices to fall 10%. The borrower loses their job and is no longer able to make their repayments, thereby defaulting on the mortgage. The bank takes possession and sells the house for $450,000 (10% discount), leaving them with a $25,000 loss. The bank approaches the CMHC, which promptly hands over the money to the bank.

It is not hard to see that Canada’s mortgage system contains high levels of moral hazard. In a mortgage market free of government manipulation, a lending institution would carefully consider what interest rate to charge a person. They would take into consideration their credit worthiness, payment history, and down payment since negative equity is one of the important determinants of default rates. However, with their default risk removed via the CMHC, Canada’s banks are able and willing to lend to people with little money, no savings history and little prospect of repaying their loans. Put another way, CMHC enables the banks to provide the cheapest, lowest mortgage rates to those with the highest default risk – Canada’s own version of sub-prime.

Sound familiar? The CMHC is essentially the same as the United States government-sponsored Federal National Mortgage Association (Fannie Mae) and the Federal Home Mortgage Corporation (Freddie Mac), which provided insurance against default risk to a large proportion of risky low-deposit loans in the United States and whom required massive taxpayer bail-outs following the bursting of their housing bubble.

No wonder, then, that the Canadian banks are ranked the “safest” in the world – most of the credit risk on their loans is being carried by Canadian taxpayers!

Canadian Taxpayers: on the Hook for Billions

A series of reforms over the past decade have significantly increased CMHC’s exposure to mortgage default risk.

In 1999, the National Housing Act and the Canada Mortgage and Housing Corporation Act were modified, allowing for the introduction of a 5% down payment.

In 2003, CMHC removed the price ceilings limitations, thereby insuring any mortgage regardless of the cost of the home.

In 2007, CMHC allowed people to purchase a home with no down payment and ammortise it over 40 years. This was changed back to a 5% down payment requirement and a maximum amortisation of 35 years in late 2008.

Finally, in an effort to support the housing market in 2008 (when affordability fell sharply and the economy tanked), the Canadian Government directed the CMHC to approve as many high-risk borrowers as possible in order to keep credit flowing. As a result, the approval rate for these risky loans went from 33% in 2007 to 42% in 2008. By mid-2007, the average Canadian home buyer who took out a mortgage had only 6% equity in their home, suggesting the risk of negative equity is high even if there is only a moderate correction.

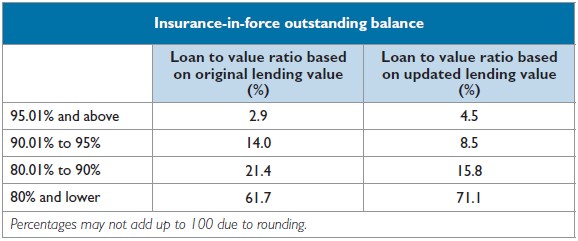

As you can gather from the above analysis, Canada’s mortgage underwriting standards are not exactly conservative. Extending 5% deposit, 35-year amortisation mortgages to individuals at the bottom of the interest rate cycle is a recipe for disaster (click to see a chart of Canada’s mortgage interest rates). Mortgage rates now have nowhere to go but up, which could generate significant mortgage stress amongst recent highly leveraged buyers and a wave of defaults and forced sales, particularly amongst the 29% of CMHC-insured borrowers with less than 20% equity in their home (see below table). There is also the risk that many recent buyers could find themselves in negative equity, whereby home values fall below borrowings, leading to a sharp drop in consumer spending, a reduction in economic growth, and job losses.

{kind=link}

However, perhaps the scariest aspect of Canada’s mortgage system is that the CMHC is terribly under-capitalised, potentially exposing Canadian taxpayers to significant losses should Canada’s housing market enter a protracted down-turn. As at 31 December 2009, the CMHC had only $9.3 billion CAD of shareholder capital but a whopping $473 billion CAD of outstanding insured loans. Should a housing correction occur, and significant defaults take place, there is very little capital available to absorb losses. Rather, like in the United States, Canadian taxpayers would be called upon to stump up funds to bail-out the banks for their risky mortgage lending.

Australia’s Current Mortgage System is Far Superior

If the above analysis hasn’t proven that the Australian Government’s proposal to adopt a Canadian-style mortgage system is foolhardy, perhaps we should hear what Canada’s leading public policy think tank, the Fraser Institute, has to say on the matter. In March 2010, it released a study highlighting the risks to taxpayers from the CMHC-insured system and suggested a privatised mortgage market structure similar to the one Australia uses. This study also confirmed that the taxpayer risk from a housing collapse is greater in Canada than elsewhere:

“…the Canadian government is heavily exposed in the mortgage market because 43 per cent of all residential mortgages (including all loan-to-value mortgages over 80 per cent) are backed by the government through the federally owned Canada Mortgage and Housing Corporation (CMHC). The report recommends that the federal government follow Australia’s example by opening Canada’s mortgage insurance market to full competition including the privatization of the CMHC…

The report points out that the Canadian model has the majority of risk concentrated with the Government of Canada, and therefore the taxpayer liability is much greater in Canada than in Australia…

In the wake of the recent financial crisis, American taxpayers are facing an enormous future liability to pay for the government bailout of the financial industry. Canadian taxpayers could face a similar liability because our government is so heavily involved in the mortgage insurance market through the CMHC…

In order to lessen the taxpayer exposure and reduce the likelihood of a Canadian mortgage crisis, the government should emulate Australia and allow the private sector to take total responsibility for insuring and securitizing Canadian residential mortgages.”

So while Australia is looking to emulate Canada’s mortgage market, Canada is examining ways to become more like Australia’s. Enough said.

Cheers Leith