We all know that the US housing market is in bad shape. Following the onset of the sub-prime turned ‘Global Financial Crisis’ (GFC), US house prices have tanked to be near their long-run trend:

Some markets where supply restrictions were present – most notably California, Nevada and Florida – have fallen hardest, whereas those with liberal land release policies, such as Texas, have held up quite well:

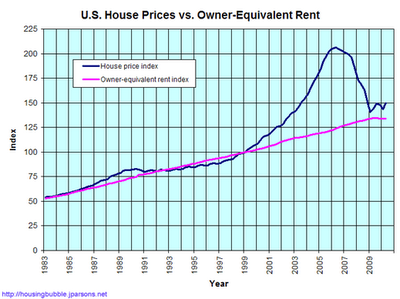

And US house prices relative to rents still appear to be moderately overvalued compared to their long-run trend:

Nevertheless, despite the large correction to date, it appears that US house prices still have a long way to fall. Below is an overview of the main headwinds likely to place further downward pressure on US house prices for many years to come.

Flooded market:

According to Eye on the Globe, there is currently around 4 million existing homes for sale in the US, which is equivalent to just under 12 months supply based on the latest monthly sales rate (4.1 million annualised). Supply and demand are said to be in balance when there is 4.5 to 6 months of inventory. Accordingly, the below chart, which tracks house prices against supply, suggests that US house prices could fall by another 20%.

Shadow housing inventory: the coming avalanche?

The ‘Shadow Inventory’ of homes comprises distressed houses highly likely to hit the market in the not too distant future. Estimates of the size of this Shadow Inventory vary. Seeking Alpha blogger, Keith Jurow, estimates this inventory to be just under 7 million properties currently, comprising:

- 4.5 million homes whose loans are delinquent 90 days or more;

- 95% of loans delinquent 60 days or more, totalling 720 thousand homes;

- 70% of loans delinquent 30 days or more, totalling 1.25 million properties; and

- 500 thousand bank-owned repossesed (REO) homes yet to be listed for sale.

Meanwhile, mortgage research firm, Amherst Securities Group LP, is even more alarmist predicting that over 11 million homeowners – 1 borrower in every 5 – will default and lose their home unless the government takes more radical intervention. The below table provides a breakdown of Amherst’s predicted defaults.

ARMageddon:

Over the next 12-18 months, tens of billions of dollars worth of adjustable rate mortgages (ARMs) and Alt-A mortgages are expected to re-set to higher interest rates (see below chart):

ARMs are similar to Australia’s variable rate mortgages, except that many were issued to borrowers with low ‘teaser’ rates whereby for a period of 3-5 years, the repayment level was set lower than the interest charged on the loan, with the balance added to the mortgage principal. The upward re-setting of these teaser rates is shown in the chart above by the light yellow bars. Similarly, the Alt-A mortgage rate upward re-sets are shown by the dark yellow bars. Alt-A are those mortgages deemed to be lower quality than Prime mortgages but higher quality than Subprime mortgages.

Although the US housing market has moved beyond the sub-prime mortgage rate re-sets (light green), the bulk of the ARM and Alt-A re-sets are still to come, which is likely to lead to further loan delinquencies and defaults, as well as depressed prices.

Unemployment near depression levels:

The Third Wave Group provides an excellent overview of some of the key issues afflicting the US economy. Core among these is the near depression-level of unemployment. According to Third Wave, the U-6 unemployment rate is now a whopping 17.1%. U-6 includes, among other things, people that want a job but gave up officially looking, people with part-time jobs that want a full-time job, and people who dropped off the unemployment rolls because their unemployment benefits ran out. A closer examination of the other forms of unemployment paints an equally sober picture.

Structural unemployment, defined as those people unemployed for more than 27 weeks now stands at 6.4 million. To give this number some perspective, it is a measure that has very rarely ever gone over 2 million.

Part-time employment gives some indication of the true depth of the problem – 612,000 more people are working part-time for economic reasons than last month. This is a truly huge monthly move and takes to 9.5 million the number of workers who wish to work more but more hours are not available. The significance of this figure is that there are 9.5 million workers whose hours need to be increased before companies actually start hiring new workers.

Many economists are suggesting that the unemployment situation is not getting better but is in fact continuing to deteriorate. The US is suffering a permanent destruction of jobs in industries such as housing and finance and looking ahead, there are no discernible drivers for increased working hours let alone new jobs. Many of the states in the US are broke, bloated with public servants and have frightening unfunded pension obligations. They are going to be forced to start shedding jobs which will certainly not improve either the employment situation or resurrect the all important consumer.

The government has tried everything it can think of to create jobs. Ironically, almost every measure they’ve employed has only made matters worse. All the government money that has been thrown at the problem in the form of stimulus, bailouts and quantitative easing has only propped up the leverage in the system, preventing the Ponzi era malinvestments from being cleared which has led to a zombie economy which in turn does nothing to create jobs.

The extent of the unemployment problem in the US is given historical perspective by the following chart – the current situation stands alone when measured against all post World War II recessions.

The current situation does not even compare favourably to the Great Depression which had a peak unemployment rate of 25 per cent. US unemployment is currently over 17 per cent (the U-6 figure needs to be used for a more realistic comparison although there are variations between the two measures) but it must be remembered that peak unemployment during the Great Depression did not occur until three years after the 1929 stockmarket crash; it has been less than two years since the start of the Global Financial Crisis (Third Wave Group, 9 October 2010).

Mortgage finance socialised:

Americans that are lucky enough to have retained their jobs are finding it more difficult to obtain finance. Risk has simply become so high in the US housing market that private money has largely pull-out of mortgage lending. This retreat from mortgage lending is most evident in the jumbo mortgage market (comprising mortgages above conventional limits), where loan issuance has fallen from $US650 billion in 2003 to $US92 billion in 2009 (see below chart). Meanwhile, government loans account for 90% of current originations.

The buyer pool is also compromised by the fact that 17% of borrowers now have impaired credit histories because of default. The typical qualifying time for a new mortgage after default is from 3 to 7 years.

Foreclosure fraud: the mortal blow:

If the above factors aren’t enough to test the US housing market’s mettle, the latest foreclosure controversy, dubbed “foreclosuregate”, has the potential to plague the market for the next decade and freeze the global financial system.

By far the best explanation of this situation that I have read is found at The Whisperer. Sorry for the marathon quote, but he/she has summarised the situation way better than I could:

The ramifications of this systemised fraud cannot be underestimated.

First, there are around $US2.6 trillion of mortgage-backed securities (MBS) within the global financial system. But without clear title, many of these MBS could have no asset backing, rendering them worthless. Many investors could, therefore, attempt to seek legal recourse to try to force the issuing institutions (mostly the biggest banks) to buy these MBS back. If the investors succeed, the damage to the banks’ balance-sheets would be enormous, potentially rendering them insolvent. Even worse, since the largest banks have been deemed ‘too-big-to-fail’, the US taxpayer could again be called upon to foot the bill.

Second, if past foreclosures were deemed invalid by the courts, banks and servicers could also face crippling lawsuits from affected homeowners.

Third, since many Americans owe more on their mortgage principal than they can ever hope to recoup, there is potential that they will purposely stop making payments (default) in the knowledge that they will not be foreclosed upon any time soon. Mortgage research firm, Amherst Securities Group LP, reports that a family who defaults could live ‘rent-free’ for 20 months on average before being evicted.

Fourth, without clear property rights, home buyers will likely evaporate, sending home prices sharply lower. According to Seeking Alpha blogger, Jeff Nielson:

GFC 2.0?

Is this the start of the sequel to the GFC? Could financial markets seize-up like in 2008 when Bear Sterns and Lehman Brothers collapsed? Only time will tell.

What we can say is that the US economy is in poor shape. The enormous private debt problem remains unresolved. The banking system is effectively insolvent, living off life support courtesy of the US Government. The US Government is operating the world’s largest Ponzi scheme – effectively repaying maturing bonds and interest by issuing more bonds, many of which are being purchased by the Fed money printers. And lets not forget the looming crisis in individual US state funding, massive looming obligations in pensions, social security and health care, as well as depression-level unemployment.

Interesting times indeed.

Till next time.

Cheers Leith

Any U.S. home which has been bought / sold more than once in the last five years, and any / every home with a mortgage tied to one of these fraud-factories cannot be trusted when it comes to being able to purchase clear title.

This means that any prospective buyer of a U.S. home must do extensive research on that property before ever making an offer, especially if they are considering making a purchase in the fraud-capitals of the U.S. housing market: Florida, California, Arizona, and Nevada. In the case of any home which has been tainted by Wall Street fraud, any sane buyer will simply walk away.

For those who decide they must buy a particular home, at the very least you will have to hire a lawyer to do a detailed analysis of the title. Given how complicated these Wall Street webs of fraud are, hiring a lawyer won’t guarantee good title, but it will give you someone to sue, if your home is later taken from you (by the rightful owner).

The most-obvious warning siren applies to foreclosure sales. Previously seen as a way to get a cheap home, it now appears more like a way to buy a home with a ticking-bomb inside it…

Let’s go back to the subprime mortgages that almost destroyed the world banking system in 2008.

Securitizing mortgages was a way of taking the cost of a mortgage off of a bank’s books and improving their bottom line.From 2005 onward the securitization chain ramped up and out of control.

Bundling and selling-off securitized mortgages was a virtual licence to print money and Wall Street wanted as many mortgages to bundle as they could get their hands on as quickly as possible and as cheaply as possible.

In order to maximize the revenue stream in the securitizaton process, the subprime lenders, trusts and banks cut as many corners as possible to save money. Included in this cost-cutting was the cost of record keeping.

Banks, trusts and subprime lenders didn’t keep very good records in their rush to shove money to middle America and fuel the massive housing bubble.

They didn’t keep good records and, in the process, they violated individual state laws mandating that they had to file records with the local state county clerks on who owned what mortgage title. This isn’t to say records weren’t kept.

What the banks/trusts/subprime lenders did was to digitize mortgage titles into a privatized system called the Mortgage Electronic Registry System, or MERS. And it did these transfers by trading excel spreadsheets among the banks and trusts rather than endorsing the mortgage notes as required by their own contracts, by state real estate law and by IRS rules.

Today MERS is the registered owner of a security interest in 60 million properties representing 60% of all the mortgages in the United States.

More importantly… since 2005 and through to 2008, 97% of the loans that originated in the United States are in the MERS system.

But it now appears that, on a widespread and probably pervasive basis, they did not take the steps necessary to legally own the mortgage note on the properties they registered.

This means that in 45 out of 50 US states, the lending institutions who have mortgages registered in MERS lack the legal right to foreclosure on the properties they claim to own.

A trend started when the foreclosures started to ramp up in earnest in 2006. When some foreclosed homeowners (and some foreclosure courts) began demanding that the proper paperwork be produced in order for the foreclosure to be carried out, the banks/trusts didn’t have it.

So the industry simply created a system where the foreclosure services would hire ‘foreclosure mill law firms’ whose business it was to simply forge documents showing – or we should say – purporting to show that they had a legal right to foreclose.

The document mill signatories have come to be called ‘robosignors’, people whose names appear on thousands of mortgage documents. Investigations from the likes of the New York Times have revealed that, although the same name appears on thousands of mortgage transfer forms, the signatures are clearly different and forged throughout all those documents. When tracked down, these signatories admit that they really did not have any knowledge of what it was they were signing.

The system is so organized that there is a company called Lender Processing Services (LPS) which has allegedly created the means to systematize this fraud. Lawyers used the LPS system to request which affidavits and documents they need [forged].

LPS then has document mills where they can magically make an authorized ‘Vice-President of whatever you need’ and send you backdated signed documents saying that you have the right to foreclose on the property you are interested in.

But recently US courts have begun sanctioning fraud charges against loan servicers [whom administer the mortgage-backed securities] as details of what has been going on becomes apparent….there have been instances where homeowners have had to go to court to fight the foreclosure process. It turns out that in a couple of cases, the banks made a mistake in the address of the property they were foreclosing on. Turns out the house the foreclosed on NEVER had a mortgage to begin with… the owner having paid cash to buy the house.

The civil suits say that in a significant number of cases, banks do not have proper title to the homes on which they are foreclosing. Worse, these lawsuits allege that the supporting documentation they are producing to support their claims has been fraudulently created and presented to the courts.

These lawsuits are about to open up a massive can of worms that speaks clearly and directly to the fact that securitized (collateralized) debt on a vast number of mortgages have no paperwork, lost paperwork or paperwork that has been duplicated many times in many collateral debt instruments.

Bank of America, J.P Morgan and GMAC have halted all foreclosure proceedings in the affected states. [And there are now calls for all institutions in the US to follow suit].