Has anyone else found Alan Kohler’s recent spruiking of Australian residential property annoying? Twice in the past week Kohler fronted the ABC News Finance Report claiming that Australia has a chronic housing shortage that would prevent house prices from falling.

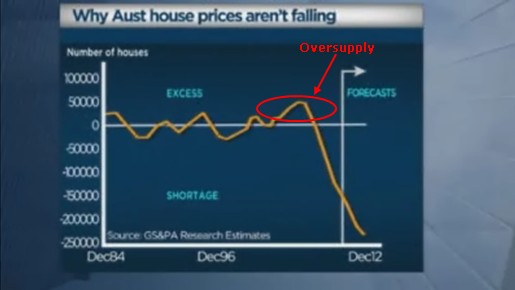

In Kohler’s first finance report, from Monday 27 September, he provides the below chart (shown from 1.18 in the video) claiming that Australia’s housing shortage will reach a whopping 250,000 units by 2012:

But if you examine this chart closely, you’ll notice that Australia had a housing oversupply between 2002 and 2006 (circled in red). My question to Mr Kohler, then, is as follows: if Australia’s recent housing shortage has played such a major role in Australia’s recent house price growth, then why didn’t house prices fall, or at least remain flat, in the early-to-mid 2000s when Australia had a housing oversupply?

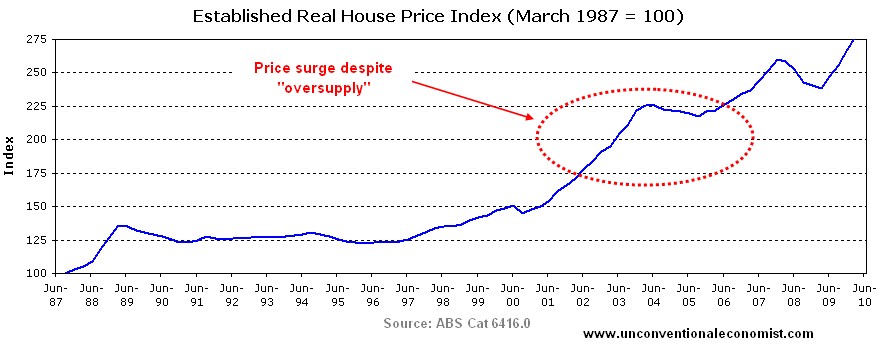

Because when one examines the house price data, it shows that Australia’s real (inflation-adjusted) house prices boomed over this period (shown below).

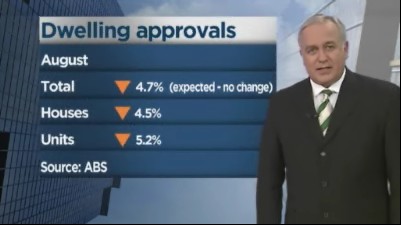

In Alan Kohler’s second finance report, from Thursday 30 September, he again spruiks the housing shortage argument, but this time claims that the 4.7% fall in building approvals in August would prevent house prices from falling “because there is still no supply“.

He then provides an update of the RP Data Rismark monthly house prices for August. The screen shot below shows that Brisbane’s prices fell 2.3% in the month:

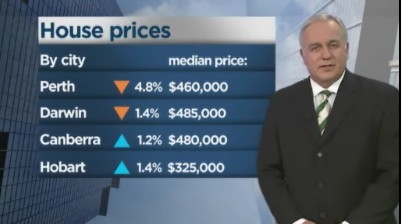

In the next screen shot, Kohler shows that Perth’s house prices fell a whopping 4.8% in the month:

My question, now, to Kohler is as follows: if tight housing supply (shortages) would supposedly prevent house prices from falling, then why did Brisbane’s and Perth’s house prices fall so significantly in August?

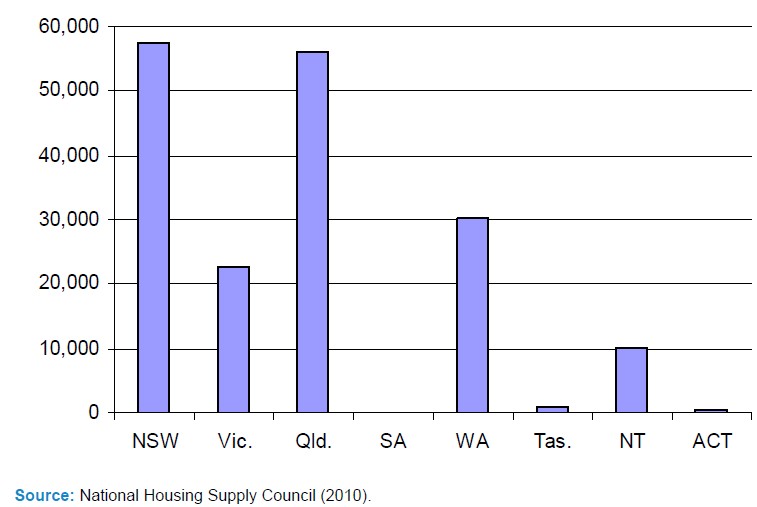

You see, according to the National Housing Supply Council’s State of Supply Report 2010, Queensland and Perth both have an acute housing shortage (see below chart) which, according to Kohler, should have prevented prices from falling. To add insult to injury, the latest Australian Bureau of Statistics’ population growth data shows that both states have experienced the fastest population growth in the country over the past year – 2.3% in Western Australia followed by 2.2% in Queensland – which similarly should have supported house prices.

Economics 101:

As I have explained previously, unresponsive housing supply results in greater house price volatility – both on the way up and the way down. Such a situation can be explained using basic supply and demand analysis, as shown in Figure 1.

Q0 and P0 represent the initial equilibrium situation in the housing market. Initial demand is provided by D0, whereas supply is shown as either SR (restricted) or SU (unrestricted), depending on whether land supply constraints exist.

Following an increase in demand, such as a surge of investors following changes to tax rules (e.g. Australia’s CGT reduction in 1999), the demand curve shifts outwards from D0 to D1. When land supply is restricted, house prices rise sharply from P0 to PR. By contrast, when supply is unrestricted, prices rise more gradually from P0 to PU.

The situation works the same way in reverse. For example, if there was a sharp fall in demand following a contraction in credit availability or a sharp decrease in Australia’s Terms of Trade, causing demand to fall from D1 to D0, then prices fall much further when land supply is constrained.

The key point of this analysis is to show that declines in demand can bring sharply falling house prices even when supply is constrained and housing shortages exist. So contrary to Kohler’s claims that Australia’s apparent housing shortage would prevent house prices from falling, the opposite is in fact the case.

Some economic history:

The economic theory explained above is supported empirically. In the years leading up to the US housing crash, parts of the US – particularly, California, Florida, Nevada and Arizona – operated highly restrictive land use policies and regulations that hindered the ability of housing supply to adjust to changes in demand. In contrast, Texas operated liberal, market-oriented land use policies that enabled builders to provide sufficient new housing at affordable prices.

As shown in the below chart, when credit standards and interest rates were loosened in the early 2000s and demand boomed (particularly speculative demand), prices rose sharply in the supply-restricted states, but remained relatively flat in Texas.

Then, in early 2007 when the sub-prime crisis manifested itself in rising unemployment and contracting credit, resulting in large reductions in housing demand, prices fell sharply in the supply-restricted states, but again remained relatively flat in Texas.

In fact, the housing supply situation in California just prior to the crash sounds eerily similar to the situation currently in Australia:

The California Building Industry Association (CBIA) continues to express alarm over what it calls an ongoing housing crisis in Southern California. Alan Nevin, the association’s chief economist, projected in a 2006 CBIA Housing Forecast that only 185,000 to 205,000 building permits will be granted this year, far short of the 240,000 new homes needed each year.

Southern California has been experiencing a massive population boom in recent years and it’s believed that 6 million new residents will be living in the region by 2020. The population increase, coupled with the housing shortage, has the CBIA worried that it will be increasingly difficult for first-time homebuyers to find a moderately priced unit (9 February, 2006).

Let’s also not forget that similar housing shortage arguments were used as a reason why prices would not fall in Britain and Japan in the late 1980s / early 1990s. Both regions, then, experienced large house price slumps, with Japan’s house prices still less than 50% of the peak value reached two decades ago, whilst Britain’s house prices fell to their lowest multiple of income ever record in 1997.

What Alan Kohler and other commentators need to understand is that Australia’s restrictive urban planning structure should not necessarily be viewed as a bullish indicator for house prices. Rather, whilst supply constraints help to explain the strong house price growth experienced in Australia’s capital cities, these same constraints would likely drive house prices down when the inevitable housing correction arrives.

The disappointing aspect of Kohler’s commentary is that it builds upon the common misconception that house prices in Australia are a one way bet – that the only way is up. In turn, this type of commentary invites greater investor speculation and encourages first-time buyers to leverage-up and purchase a home before they ‘miss out’. But with house prices already severely overvalued by every measure, and Australian households among the most indebted in the world, you have got to ask yourself whether such encouragement is warranted and in the national interest?

What happened to the growth?

Finally, towards the end of Kohler’s second finance report, he displays the below chart, taken from the RBA Financial Stability Review (Graph 21), and notes that “Australia has not had the biggest rise in house prices in the past 8 years, New Zealand has”.

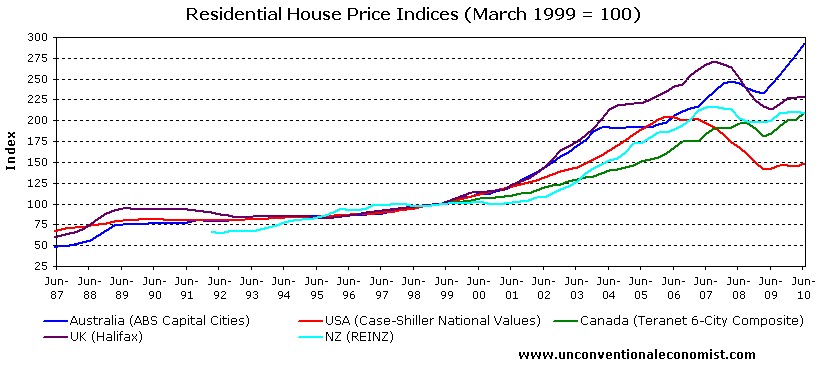

However, had Kohler gone back before 2002, he would have found that Australia’s house price growth has far exceeded New Zealand’s as well as other comparable countries (see below).

To be fair to Kohler, we can’t blame him for this oversight since he was merely reporting on the RBA report. But one has to wonder why the RBA appears to have deliberately understated Australia’s house price growth by selecting a starting point where Australia’s house prices had already risen strongly relative to other countries.

Till next time.

Cheers Leith