Population growth is often cited as a causal factor in the overvaluation of Australian real estate. And indeed, strong population growth is a factor, particularly in recent years when housing starts have diminished, most especially in NSW.

But one infrequently quoted housing statistic that calls into question the strength of population growth causation is what this blogger likes to call housing velocity. That is, how quickly established dwellings have been changing hands over the past two decades.

This measure can be viewed as a proxy for the degree of ‘flipping’ in the market – the practice of turning over homes quickly and cashing out the capital gain.

The term flipping arose in the US where it became such a popular practice at the peak of the housing frenzy that it spawned its own lifestyle program. Not surprisingly, the program ultimately collapsed under the weight of its own corruption.

Australia has a different breed of the practice for a number of reasons. These include negative gearing and depreciation for investors and a 12 month live-in condition for owner-occupiers if they wish to avoid capital gains tax. Probably meaning Australia has longer maturity flippers (if you’ll pardon the oxymoron).

Nonetheless, if we compare the number of dwelling transfers (sales) with population growth, housing velocity remains a reasonable measure of the level of speculative or investor interest in property.

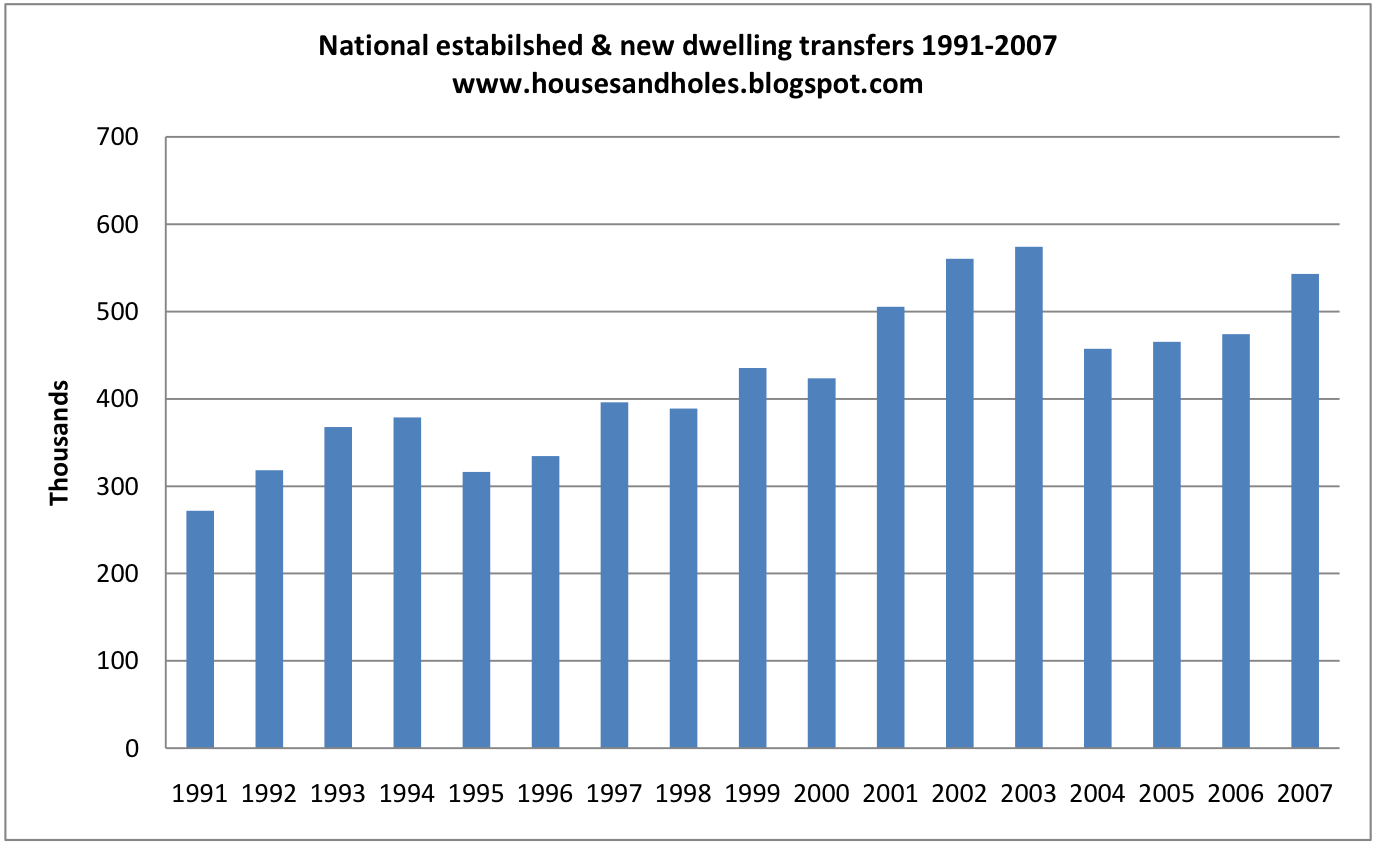

The above chart tracks the number of properties changing hands per annum from 1991 to 2007. It tells a clear tale of a rising trade in houses. A 100% rise in fact.

Over the same period population rose 24%.

The chart begins in 1991, when, to be fair, Australia was still emerging from recession. But 1992 is a more typical year and the increase between that year and 2007 is still a whopping 71%. Well above population growth.

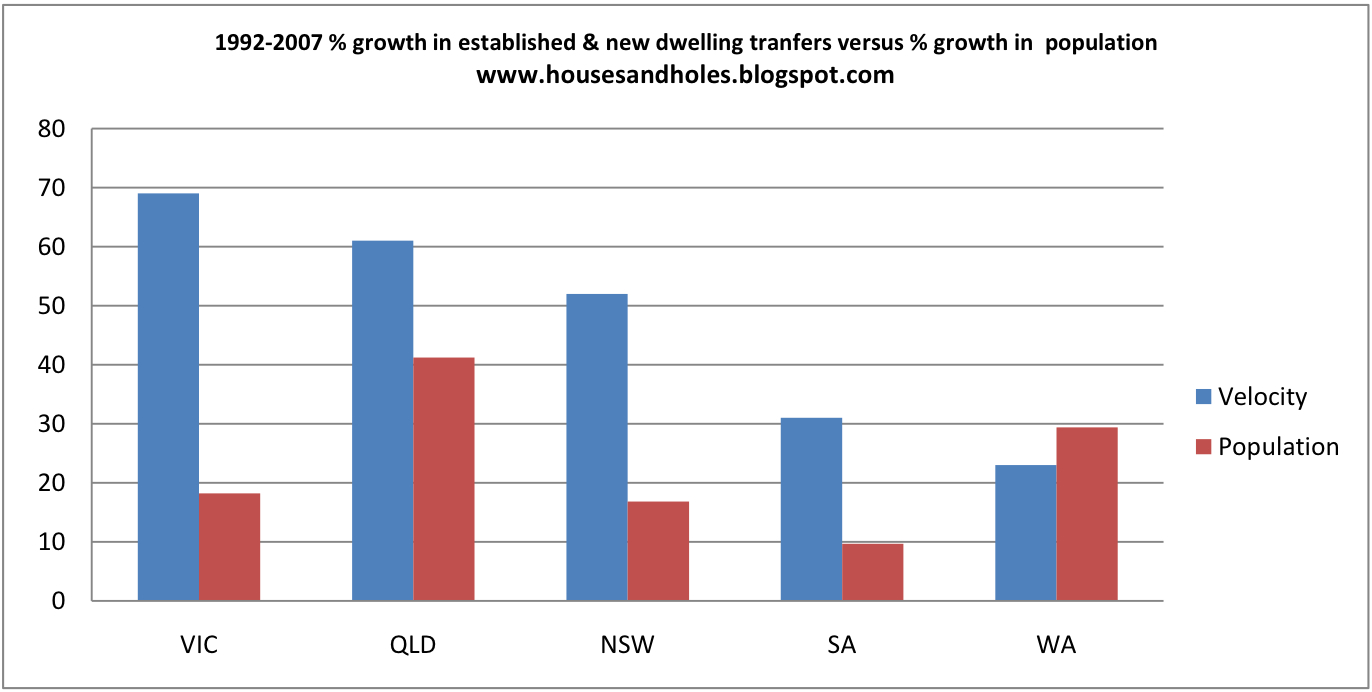

Now, this analysis does not claim to be exhaustive. There are many variables in the equation, not least being the number of demolitions of old homes for new and an increasing trend toward labour mobility. Nonetheless, a state-by-state breakdown reinforces the conclusion that the gap between population growth and turnover is the result of speculation.

Of the major states, WA appears best placed to claim a population-driven housing market. However, if you go back one year, the percentage growth in turnover from 1992 doubles. Go back another year and it triples. WA is simply on a different housing cycle owing to its huge exposure to commodity prices.

That leaves Qld as the strongest case for a population-based revaluation of property. And the sunshine state has run the highest per capita rate of housing commencements of the big states for many years, providing a supply-side offset to population growth. We might, therefore, expect high turnover growth.

Finally, we have NSW, VIC and even little SA, where the gap between percentage population growth and the percentage growth in dwelling transfers develops into a yawning chasm. Draw your own conclusion.

N.B. All data is either Australian Property Monitors or ABS.