Canada and Australia have a lot in common. Both economies are commodity exporters. Both countries largely dodged the global recession that has recently shocked the developed world. And both countries are said to have world-beating banking systems, with Canada’s ranked as the strongest and Australia’s ranked third strongest in the world by the World Economic Forum’s Global Competitiveness Report 2009-2010.

As in Australia, there is currently widespread debate in Canada about whether the country is experiencing a speculative housing bubble or asset inflation based upon sound fundamentals. Last week, two opposing think tanks – The Canadian Centre for Policy Alternatives (CCPA) and the C.D. Howe Institute – released papers on the Canadian housing market. The CCPA paper warns that bubble-like conditions have developed in some of Canada’s key housing markets and attempts to model the potential fallout if the bubble bursts under a number of scenarios. Whereas the C.D. Howe Institute paper argues that a US-style housing bust is highly unlikely due to Canada’s more sensible housing policies and, instead, predicts only a modest decline in Canadian house prices.

So which think tank is right? Is Canada’s housing market and economy at risk of a housing correction or crash, or would Canada’s ‘strong’ banking system, supposedly tight lending standards, and solid economic fundamentals prevent significant house price falls from occurring? Let’s examine the arguments and data.

Uneven house price growth:

The below chart, taken from the CCPA report, plots average residential real estate prices since 1980. The graph shows that house prices rose sharply from 2000 which, like Australia, is proclaimed as being the beginning of Canada’s housing bubble.

As you can see, like Australia, Canada’s housing market has shown remarkable resilience throughout the global recession, registering only a brief fall as the recession hit in 2008, then quickly regaining its upward march in 2009/10.

The CCPA report also provides the average inflation-adjusted housing prices in Canada’s six major cities – Vancouver, Edmonton, Calgary, Toronto, Ottawa and Montreal – between 1980 and 2010 (shown below).

There are three interesting observations relating to this chart. First, excluding Vancouver, between 1980 and 2000, the historical price range for Canadian housing was typically between $50,000 and $100,000 in inflation-adjusted 1980 Canadian dollars.

Second, there were three housing bubbles experienced in Canada over the period 1980 to 2000: the 1981 Vancouver housing bubble/bust; the 1989 Toronto bubble/bust; and the 1994 Vancouver bubble, which deflated gradually over nearly 5 years.

Third, housing price-to-income ratios have also expanded across Canada’s major cities. For the 20 years prior to 2000, housing prices remained between 3.0 and 4.0 times median annual incomes. Today, however, housing prices have increased to between 3.8 and 9.3 times median incomes according to Demographia’s 6th Annual International Housing Affordability Survey, with Ottawa being the most affordable city and Vancouver being the most expensive.

According to the CCPA, “Canada is experiencing, for the first time in the last 30 years, a synchronized housing bubble across the six largest residential real estate markets… Today, all major cities in Canada are experiencing housing price increases that are beyond their historic $50K–$80K range. They are all over $100,000 in inflation-adjusted dollars.”

Whilst Canada’s house price accent has been pervasive, it has yet to reach the dizzying heights of the United States or Australian housing bubbles. As shown by the below chart, average house prices in Canada’s six largest cities have risen by 101% since 2000, whereas prices rose by 121% in the United States at their peak and have risen a whopping 155% in Australia.

Nevertheless, prices are clearly bubbly in some areas of Canada, with two of the six cities (Vancouver and Toronto) ranked as “severely unaffordable” and three of the six cities (Montreal, Calgary and Edmonton) ranked as “seriously unaffordable” by Demographia. In fact, Vancouver is ranked as the most unaffordable city out of the six countries surveyed (Australia, Canada, Ireland, New Zealand, United Kingdom, and United States).

Drivers of the house price boom:

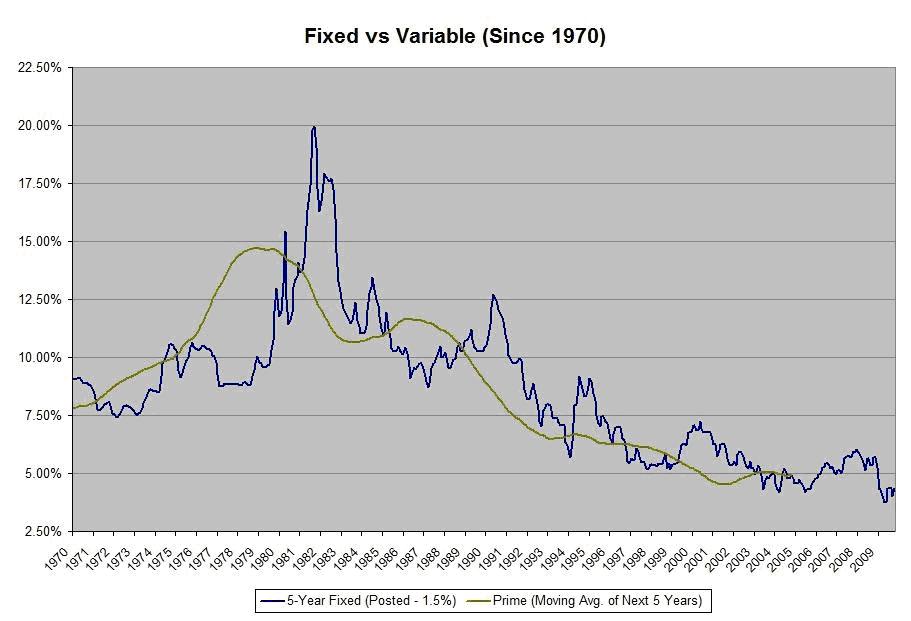

Canada’s house price growth since 2000 appears to have been driven by the usual suspects – an increased ability and willingness of Canadians to take on higher levels of debt. As shown by the below chart, variable and fixed mortgage rates have been on a downward march for the past 30 years.

In fact, variable mortgage rates reached a low of only 2.25% in 2009/10. They have since recovered to 2.75% as at September 2010. Discounted five year fixed rates are currently sitting at around 4%.

Combined with the lower cost of borrowings, Canada has also significantly loosened mortgage eligibility criteria, culminating in the recent introduction of the zero-deposit, 40 year mortgage. Previously, borrowers were required to provide at least a 5% deposit with 25-year amortisations. Further, the amount that Canadians can borrow has increased, with many individuals in 2009 being granted loans in the $500,000 to $800,000 CAD range provided their household income ranges from 110,000 to 170,000 CAD.

With the easier access to housing credit, it is little wonder that Canada’s households have significantly increased their borrowings which, in turn, has fuelled house price growth. As shown below, Canada’s household debt as a share of personal disposable income has increased steadily since 2000 in line with house price growth. However, Canada’s household debt levels, which was 147% of disposable income as at the 1st quarter of 2010, still has a way to go before it reaches the lofty heights achieved by the United States and United Kingdom prior to the onset of the global recession.

Canada’s household debt levels also have a way to go before they reach Australian levels (currently 157% of disposable income). The below chart, produced for the benefit of my Australian readers, plots the growth in household debt levels in Australia. As for Canada, the United States and United Kingdom, household debt levels surged post-2000 and is a key explanation of the housing price bubbles that developed in these nations.

According to the CCPA report, population growth and housing supply do not appear to have played a significant role in pushing up Canada’s house prices. As shown in the below table, the number of people per dwelling has actually been falling in the two bubbliest cities – Vancouver and Toronto.

“Presumably, prices will be bid up if there are more people bidding on the same number of houses… However, the trend is in the opposite direction. The stock of private dwellings is actually increasing at a faster rate than population growth, meaning that more houses are being built than people are being added to the population. The trend is happening even faster in Vancouver where prices are higher than Toronto. Builders are keeping up with population growth and then some.”

The CCPA’s finding that housing supply has had little impact on prices is supported by a recent Bank of Canada Working Paper, which found…”that the housing stock was overbuilt at the end of 2008 by 2 per cent…. there was likely overbuilding by the end of 2008 in Saskatchewan, New Brunswick, British Columbia [home of Vancouver], Ontario [home of Toronto], and Quebec [home of Montreal].”

A similar situation has developed in Australia where the number of people per dwelling has fallen steadily for the past 50 years, from 3.6 in 1960, 2.75 in 1990, 2.62 in 2000, and 2.56 in 2008. So, like Canada, the growth in the number of dwellings in Australia has actually outstripped the increase in the population and, therefore, the average number of occupants per dwelling has declined.

Are things all that different up north?

The C.D. Howe Institute argues that there is little risk of a US-style housing bust in Canada:

“Canadian housing policies, which avoided the sharp decline in underwriting standards seen in the US, worked well in reducing the possibility of a housing bust in Canada during 2008-2009, and continue to mitigate the risk of a massive wave of defaults in the future…

Compared to the US, Canada has maintained tighter conditions on government backstopped insurance against mortgage default. The Bank Act requires all federally regulated institutions to purchase mortgage insurance on loans with down payments of less than 20 percent (25 percent before 2007). This mortgage insurance is explicitly backstopped by the federal government, as the federal government guarantees the insurance provided both by the Canadian Mortgage and Housing Corporation (CMHC) and its private market competitors. All high loan-to-value (LTV) mortgages (greater than 80 percent) insured through this program must satisfy underwriting standards that specify maximum loan-to-value ratios, maximum amortization periods, and minimum standards for credit worthiness and mortgage documentation…

This difference in government policy has helped to discourage the build-up in Canada of a large number of high-risk mortgage loans… The small number of high-risk loans underwritten suggests that the modest decline in Canadian house prices predicted for 2011 (TD Economics 2010) is very unlikely to trigger a US-style surge in foreclosures.”

Whilst I agree that Canada’s mortgage underwriting standards are tighter than those displayed by the United States in the lead up to the sub-prime crisis, I certainly do not consider them conservative. Extending zero deposit, 40-year amortisation housing loans to individuals at the bottom of the interest rate cycle is a recipe for disaster. Mortgage rates now have nowhere to go but up, which could generate significant mortgage stress amongst recent highly leveraged buyers and a wave of defaults and forced sales. There is also the risk that many recent buyers could find themselves in negative equity, whereby home values fall below borrowings, leading to a sharp drop in consumer spending, a reduction in economic growth, and job losses. According to Wikipedia, throughout 2007, the average Canadian home buyer who took out a mortgage had only 6% equity in their home, suggesting the risk of negative equity is high even if there is only a moderate correction.

There also appears to be high levels of moral hazard inherent in the Canadian mortgage lending system by virtue of the role played by the government-owned Canada Mortgage and Housing Corporation (CMHC). The CMHC insures mortgage lenders against mortgage default on mortgages with less than 20% deposits, thereby transferring the risk of default to the Government. So if the individual receiving the loan went bankrupt then the bank who gave the loan would not lose money, but instead would be reimbursed by the government via the CMHC. But by removing all the default risk, the CMHC enables Canada’s banks to lend to people with little money, no savings history and little prospect of repaying their loans. Put another way, it enables the banks to provide the cheapest, lowest mortgage rates to those with the highest default risk – Canada’s own version of sub-prime.

Sound familiar? The CMHC is essentially the same as the United States government-sponsored Federal National Mortgage Association (Fannie Mae) and the Federal Home Mortgage Corporation (Freddie Mac), which provided insurance against default risk to a large proportion of risky low-deposit loans in the United States and which required massive taxpayer bail-outs following the bursting of their housing bubble.

No wonder, then, that the Canadian banks are ranked the “safest” in the world – most of the credit risk on their loans is being carried by Canadian taxpayers! The scary thing is, as at 31 December 2009, the CMHC had only $9.3 billion CAD of shareholder capital but a whopping $473 billion CAD of outstanding insured loans. Should a housing correction occur, and significant defaults take place, there is very little capital available to absorb losses. Rather, like in the United States, Canadian taxpayers would be called upon to stump up funds to bail-out the banks for their risky mortgage lending.

How bad could it get?

The CCPA Paper simulates the potential house price reductions if the Canadian housing market corrects under three possible scenarios.

Scenario 1: Market correction through price deflation:

The first scenario replicates the 1994 Vancouver market correction. As shown in the below chart, prices unwind in an orderly fashion over a three and a half year time frame.

In this scenario, the cities with the highest rate of price appreciation from its previous stable price (Edmonton and Montreal) experience the sharpest price falls.

Scenario 2: Bubble bursting slowly:

The second scenario replicates the 1989 Toronto real estate crash. It is worse than scenario 1 since it draws out larger losses over a five year time frame.

Scenario 3: Bubble bursting rapidly and steeply:

The third scenario replicates the recent United States housing crash in the nine worst hit bubble cities. It assumes that mid-2009 represented the new equilibrium for house prices in these cities.

Although scenario 3 is not actually the worst of the three scenarios for ultimate price declines, it is by far the worst in terms of the speed of decent, with the correction taking place in under three years.

How likely?

Whilst I do not pretend to be an expert on the Canadian housing market, I do believe that a price correction, at least in the most unaffordable cities of Vancouver and Toronto, is highly likely. Both cities have experienced housing corrections over the past 30 years and, given the extent of their overvaluation, there is every likelihood that they will experience one again in the foreseeable future.

I do not buy into the argument that because Canada’s lenders avoided the worst of the excesses of the United States (i.e. fixed rate mortgages, non-recourse lending, sub-prime lending), that Canada would necessarily avoid the same fate. This was a global bubble and house prices are down in many countries that had seen strong house price rises over the past decade and whom did not drop lending standards to the same degree as in the United States.

The Canadian economy is also likely to meet substantial head winds in the coming years, which could hurt their housing market. First, Canada is as reliant on exporting to their neighbour to the south as Australia is exporting to China. But with the United States economy likely to remain depressed, Canada’s export growth is likely to be sluggish, resulting in fewer jobs, lower consumer spending and growth.

Second, the Baby Boomer generation’s retirement is likely to adversely affect Canada’s housing market. According to a recent Bank for International Settlements research paper, Canada can expect population ageing to reduce house price growth by over 40% over the next 40 years compared to what would occur if Canada’s age structure remained neutral (see below).

Ultimately, whether Canada experiences a United States-style housing crash or a more gradual deflation is a mute point. Both scenarios will hurt. What I can say with confidence is that the days of solid house price growth are over. Too much debt, ageing demographics, and rising interest rates have put an end to that.

Till next time.

Cheers Leith

Article also posted on Seeking Alpha.

{kind=link}