Categories

Iron ore price

Daily iron ore price update (fade)

Here are the iron ore charts for September 16, 2015: Spot down with Tianjin falling 0.7% to $56.

David Llewellyn-Smith

10 years ago

1

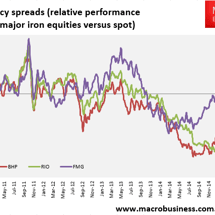

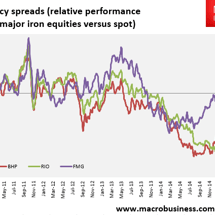

BHP, RIO and FMG surge as iron ore falls

David Llewellyn-Smith

10 years ago

3

Ivan the terrible feels the pain

From the FT: Glencore launched a $2.5bn share placing on Tuesday as the miner-cum-trader moved quickly to implement a $10bn package of measures to cut its large debt load and safeguard its investment grade credit rating.

David Llewellyn-Smith

10 years ago

2

Daily iron ore price update (slippy)

Here are the iron ore charts for September 15, 2015: Qingdao down and Tianjin down even more by 1.9% to $56.40.

David Llewellyn-Smith

10 years ago

1

Daily iron ore price update (“permanent decline”)

Here are the iron ore charts for September 14, 2015: Spot down sharply with Dalian hinting at more falls today.

David Llewellyn-Smith

10 years ago

8

BHP, RIO flat, FMG up as China weighs

Big iron ore not having much fun today with RIO and BHP down half a percent but FMG is better up 2.5%: Idiocy spreads continue to close: And juniors to die.

David Llewellyn-Smith

10 years ago

3

The dumbest RIO spruik yet

From the Motley Fool: A frustrating aspect of investing is when external factors affect the financial performance and share price of a company in which an investment has been made.

David Llewellyn-Smith

10 years ago

10

Big dirt is in big trouble

According to the AFR, iron ore is defying the doomsayers: UBS mining analyst Glyn Lawcock says the latest trading band is at odds with most market commentators, who were been tipping a fall back below $US50 a tonne.

David Llewellyn-Smith

10 years ago

7

Daily iron ore price update (rebooted forecasts)

Here are the iron ore price charts for September 12, 2015: Spot is unchanged on Friday’s holiday.

David Llewellyn-Smith

10 years ago

4

Mining FIFO to become R2D2?

Chris Becker

10 years ago

18

Daily iron ore price update (FMG hope)

by Chris Becker The rally in iron ore continues!

Chris Becker

10 years ago

19

Daily iron ore price update (rally)

by Chris Becker The rally continues in the iron ore price complex, on the back of speculation of more stimulus, but in context this is just another blip in the long running downtrend.

Chris Becker

10 years ago

5

Daily iron ore price update (imports down)

by Chris Becker Find below the latest prices from the iron ore complex: There’s been a not unexpected breakout in spot and futures following last week’s holiday and very low volatility, but rebar continues to tell the fundamental story.

Chris Becker

10 years ago

12

Daily iron ore price update (BHP)

by Chris Becker Find below the latest prices from the iron ore complex, with markets reopening following China’s two day holiday.

Chris Becker

10 years ago

2

Daily iron ore price update (steel reality)

by Chris Becker Here are the latest prices and chart action from the iron ore price complex.

Chris Becker

10 years ago

2

Daily iron ore price update (Rio bull)

by Chris Becker With Chinese markets closed there’s not much action out there in the iron ore complex.

Chris Becker

10 years ago

2

Daily iron ore price update (parade glory)

by Chris Becker Yesterday was the last day of trading for the iron ore complex before the end of WW2 celebrations in China, and prices remained remarkably stable compared to their stock brethren.

Chris Becker

10 years ago

1

Daily iron ore price update (keep calm)

by Chris Becker Its been a wild ride of risk markets, but the iron ore/coal complex is brushing this all aside and remaining remarkably stable.

Chris Becker

10 years ago

3

Daily iron ore price update (S&P laugh)

by Chris Becker Iron ore prices barely lifted yesterday: As exports of iron ore from Australia to China increased 6% year on year to 155 million tonnes, yet earnings declined by 30% according to China Resources Quarterly.

Chris Becker

10 years ago

9

Daily iron ore price update (liftoff?)

Chris Becker

10 years ago

5

Dead cat struggles to raise ASX

Given the size of last night’s moves in the US and commodity markets, big iron ore and gas is behaving with veritable sobriety undoing only a small portion of recent damage.

David Llewellyn-Smith

10 years ago

1

Daily iron ore price update (Dalian melt-up)

Here are the iron ore charts for August 27, 2015: Tianjin benchmark firmed a little to $53.30.

David Llewellyn-Smith

10 years ago

7

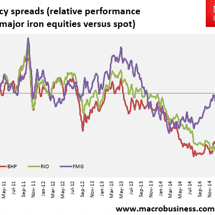

Big iron rallies with futures

Big iron is kind of off the canvas today with RIO down marginally and BHP as well as FMG up 1%: Idiocy spreads are still closing but it’s slowed right down.

David Llewellyn-Smith

10 years ago

Daily iron ore price update (parade)

Here are the iron ore price charts for August 26, 2015: Tianjin benchmark fell 30 cents to $53.10.

David Llewellyn-Smith

10 years ago

4

BHP’s grand delusion

Anyone that’s in the know understands that BHP is the round boy of the resources sector.

David Llewellyn-Smith

10 years ago

25

Newer Articles

Older Articles

Page

149

of

231

Newer Articles

Older Articles

Advertisement