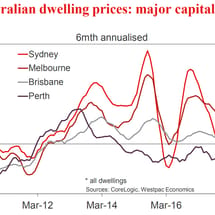

Biggest Sydney house price decline in 9 years

By Leith van Onselen The slow deflation of Sydney’s housing market eased this week, with values falling only 0.01% in the week ended 19 April, according to CoreLogic: Sydney home values have now declined by a cumulative 4.4% over the past 32-weeks, with values also down 4.3% over the past 37 weeks.