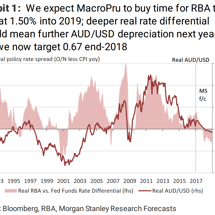

Australian dollar hollowed out as yield spread keeps crashing

New narrows today for the carry trade into Aussie dollars as the yield spread on the two year bond hit 45bps overnight, it’s narrowest since April 2001: The last time the spread was this narrow, the Aussie dollar was trading at 49 cents.