APRA waves wet lettuce at bank offshore funding

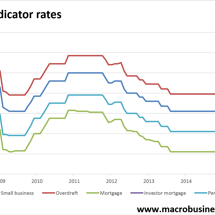

By Leith van Onselen Australian Prudential Regulatory Authority (APRA) chief, Wayne Byers, has continued his arse covering roadshow, cautioning the banks about their exposure to offshore funding markets.