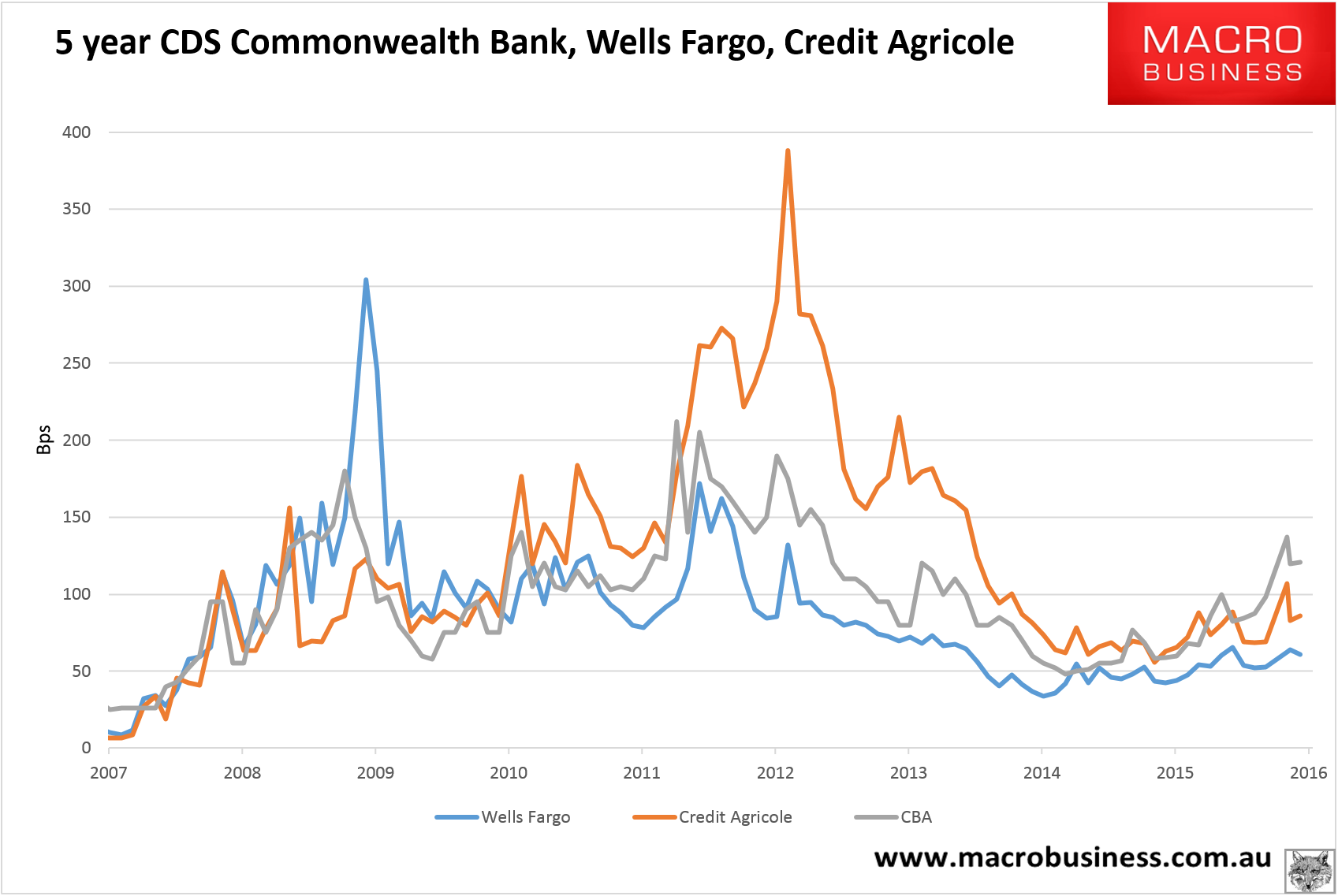

The Aussie bank funding cost rocket appears still relatively well-fueled. Yesterday the price of our US and European bank proxies both fell marginally as oil eases credit spreads globally again. The CBA also eased very slightly to 120bps but it remains elevated:

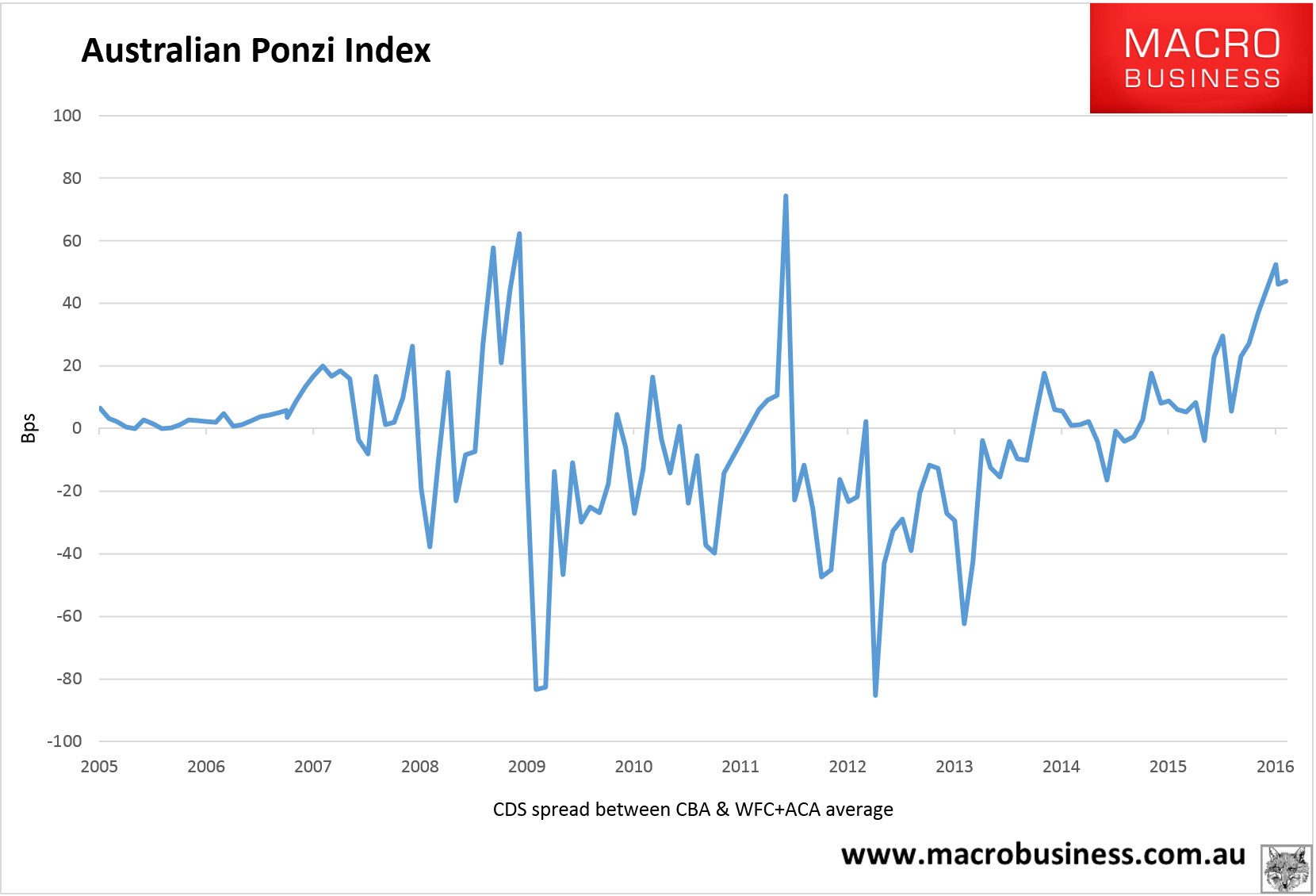

The Ponzi Index rose a couple of points:

Fairfax has a nice chart showing how popular the bank short is getting:

Advertisement

The big bank short is getting more popular, but also more expensive.

As the chart below shows, short interest in the big four lenders has more than tripled in under a year.

In that time big banks stocks are down by around 20 to 30 per cent; which means the shorts have generally fared okay and avoided the widow-maker fate that has befallen the shorts before them.

But as the confidence of the shorts grow they are confronted by a new challenge; that they must effectively fund the dividend which is owed the owner of the shares they’ve borrowed. And as the share price of the banks have fallen, the dividend as a percentage of the price has continued to rise. For hedge funds willing to get on board now, its a far more expensive proposition to short bank stocks.

For instance, ANZ’s gross dividend yield is now 11.2 per cent, which means a hedge funds that are initiating a short position now, effectively require a decline of about that value from here; or a cut in the dividend.

Definitely some potential for increased volatility there, down and up.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.