Why regional property values are stronger than the capital cities

Since the onset of the COVID-19 pandemic in March 2020, regional property values across Australia have experienced explosive growth.

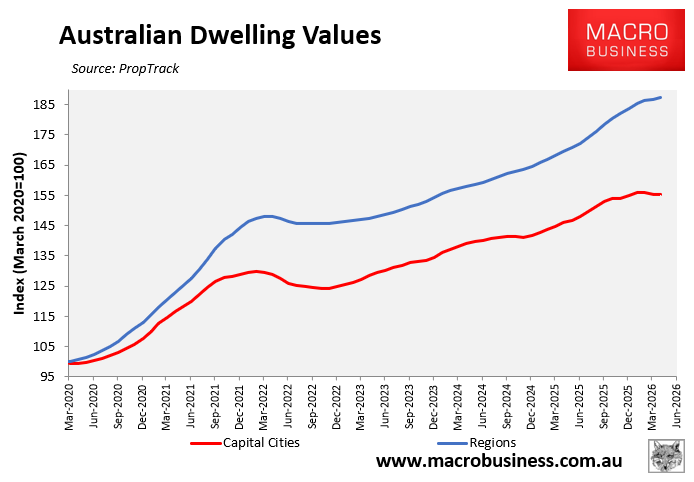

As illustrated below, PropTrack’s monthly dwelling values index has recorded 87% growth across the combined regions since March 2020, significantly stronger than the 55% growth recorded across the combined capital cities.

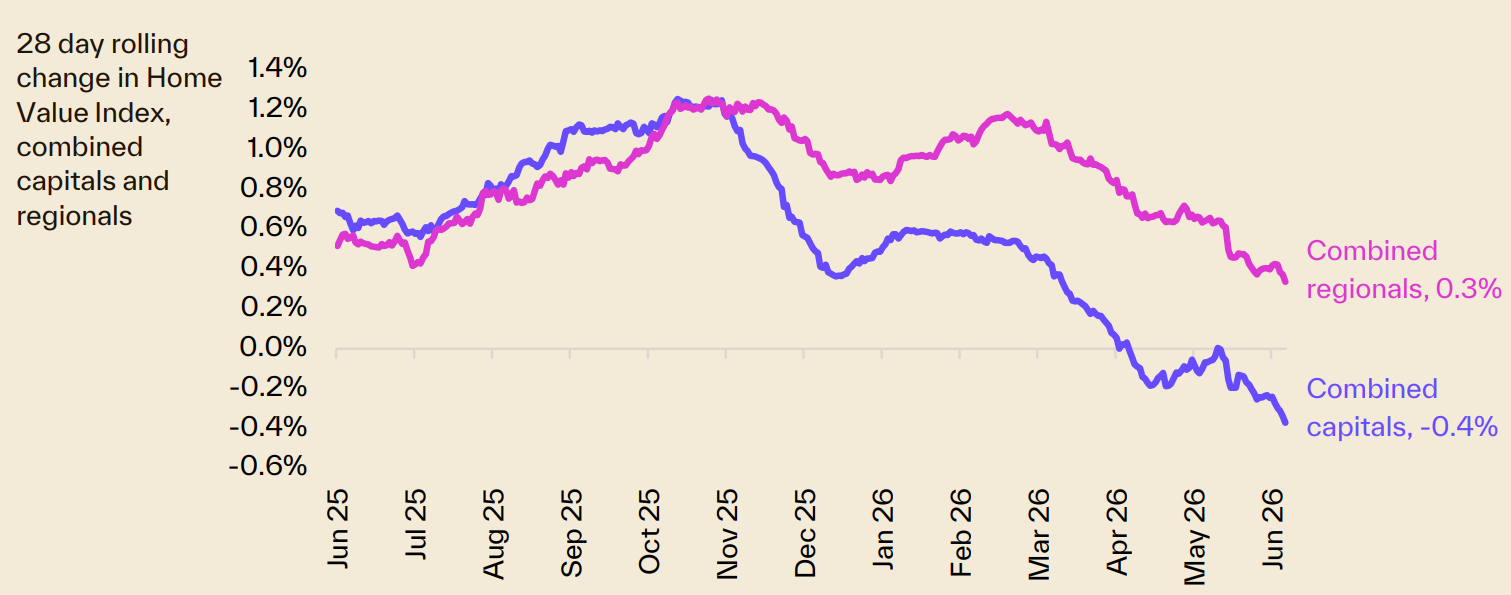

Cotality’s daily dwelling values index has also recorded stronger growth across the combined regions (0.3%) than the capital cities (-0.4%) over the past 28 days.

Source: Cotality

The latest Regional Movers Index, a joint Commonwealth Bank and Regional Australia Institute (RAI) initiative, suggests that regional Australia is no longer a “second choice”. Internal migration from cities to regions has surged to record levels, driven by affordability pressures, lifestyle preferences, and the normalisation of hybrid work.

The Regional Movers Index recorded its highest level of migration on record between January and March 2026.

Moves from capital cities to regions were 29.7% higher than moves in the opposite direction.

Capital‑to‑regional moves made up 11.9% of all internal migration, up 20.1% from the previous quarter and 4.7% year‑on‑year.

RAI CEO Liz Ritchie claimed that “Regional Australia is no longer a second choice – it’s the smart choice”.

Affordability advantages are likely driving the shift to the regions, with the median capital‑city home price at $1,012,000 in May, well above the median regional home price of $723,000.

Many first home buyers are being priced out of capital cities and turning to regional markets.

Regional areas also offer larger homes, outdoor space, and lower density. And hybrid work arrangements have made living further from CBDs more feasible.

Movement to regions has been rising since 2018, with only a brief dip in 2023.

Demand for regional houses rose 20% year‑on‑year, compared with 10% in the capitals. Regional units also saw higher demand growth (i.e., 14% versus 9%).

As a result, many regional areas now face tight supply, pushing prices higher.

While more Australians are choosing to live in the regions, the opposite is true for migrants, who overwhelmingly choose the capital cities.

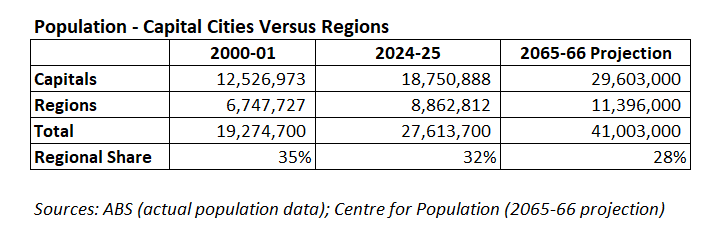

In 2000-01, Australia’s regions accounted for 35% of the population. As of 2024-25, the latest available data from the ABS shows that the regions’ share of Australia’s population has declined to 32%.

The Centre for Population’s 2025 Population Statement projects that Australia’s population will grow by 13.4 million people over the 41 years to 2065–66.

Most of this 13.4 million growth (81%) is projected to occur in the capital cities, which are expected to swell by 10,850,000 over the next 41 years. Australia’s regions are projected to only grow by 2.5 million.

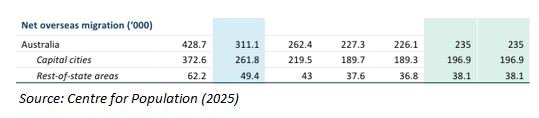

The Centre for Population also projects that the overwhelming majority (84%) of net overseas migration will flow to capital cities rather than to Australia’s regions.

Consequently, by 2065-66, the regions are projected to comprise only 28% of Australia’s population, a decrease of 7 percentage points from 2000-01.