When it comes to the tax system, fortunes favour the old

There is growing concern that Australia’s tax and transfer system disproportionately benefits older, wealthier retirees while placing a rising burden on younger workers.

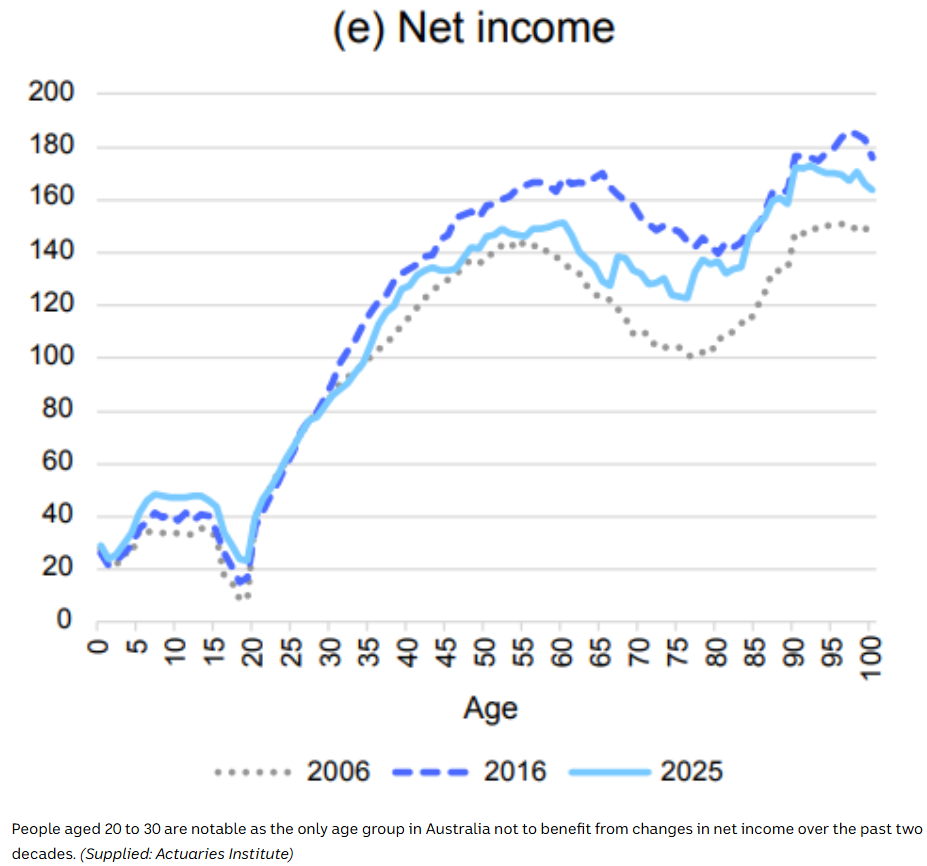

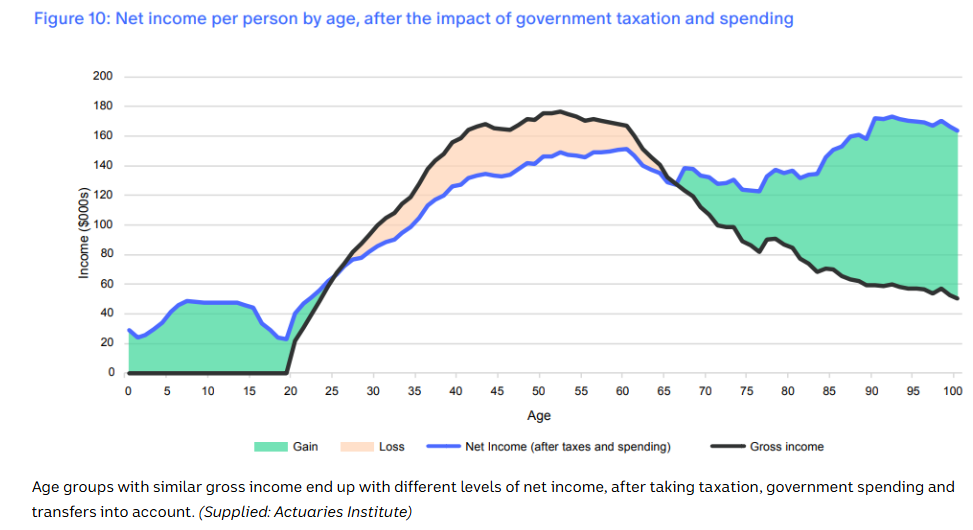

Analysis from the Actuaries Institute shows that two Australians earning the same gross income can end up with vastly different net incomes purely because of their age.

That is, a 30‑year‑old earning $100,000 receives a net income of $85,700, whereas a 71‑year‑old earning $100,000 can receive a net income of $128,100, a difference of $42,400.

This difference arises from:

- Tax concessions for older Australians

- Eligibility for benefits

- Higher government spending on older age groups

- Lower effective tax rates on retirement income

The report finds that older Australians have enjoyed stronger income growth over the past 20 years and receive more government spending per person (especially in health). They also benefit from tax settings that reduce their effective tax burden.

By contrast, people aged 20–30 are the only age group whose net incomes have not improved over two decades. They face higher taxes relative to the benefits they receive and bear a growing share of the national tax burden.

The Actuaries Institute warns that Australia’s tax and spending system treats similar incomes differently based on age rather than means. As a result, the sustainability of age‑based spending is now in question and inequality between younger and older generations is widening and could reach record levels.

Co‑author Hugh Miller notes that while some of the gap reflects genuine need (e.g., health spending), a significant portion is due to policy design.

The report highlights how younger workers face stagnant wages, higher living costs, and reduced net income growth. They are contributing more to the tax system while receiving less back.

The Actuaries Institute concludes that Australia’s tax and transfer system is increasingly unfair to younger workers, who:

- Pay more tax

- Receive fewer benefits

- Have seen no net income gains in 20 years

- Are subsidising older generations despite earning less and facing higher living costs

Back in April, a retired bank economist, Jeff Oughton, said that young Australians should be “marching in the streets”, because they are facing high income taxes, stagnant wages, and soaring public debt.

“Rich people like me who stopped working at 53 and have been wandering the world travelling and volunteering, their tax rates in retirement are effectively zero”, Oughton said.

“But all the young people have an intergenerational shit sandwich”.

Former Treasury secretary Ken Henry noted that the share of over‑65s paying income tax has fallen from 27% to 17%.

Retirees can hold up to $2 million in tax‑free super, plus special senior tax offsets.

A self-funded retiree couple can have $4 million in super, unlimited home equity, and $60,000 in outside income — and still pay zero income tax.

Meanwhile, older Australians rely heavily on taxpayer-funded healthcare, aged care, and other services.

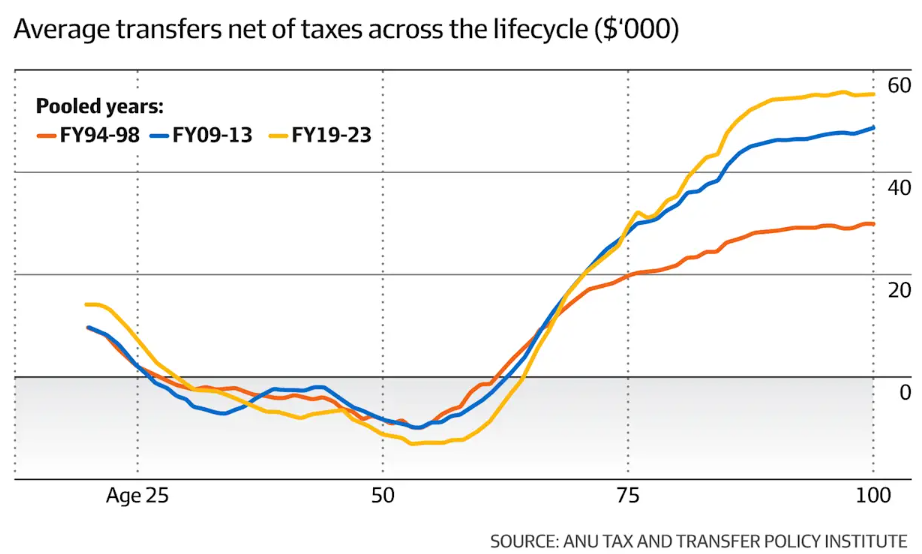

ANU research shows that over‑60s now have incomes that are 95% of working‑age Australians, up from 61% in the 1990s.

Over‑60s also earn 160% more than 18–30‑year‑olds, fuelling claims of intergenerational inequity.

“It’s kind of perverse that we’re subsidising people to amass large amounts of wealth to pass on to their children tax-free, and taking it away from working wage and salary earners through income tax”, ANU Tax and Transfer Policy Institute director Robert Breunig said.

A double-sided problem:

Australia’s heavy reliance on income tax is part of the problem.

Australia relies more on income tax than most countries because its GST is only 10%, far below European consumption taxes (~20%). Other tax bases are shrinking, including the fuel excise (driven by the EV transition), the tobacco excise (driven by illegal smokes and vapes), and the alcohol excise (younger people drink less).

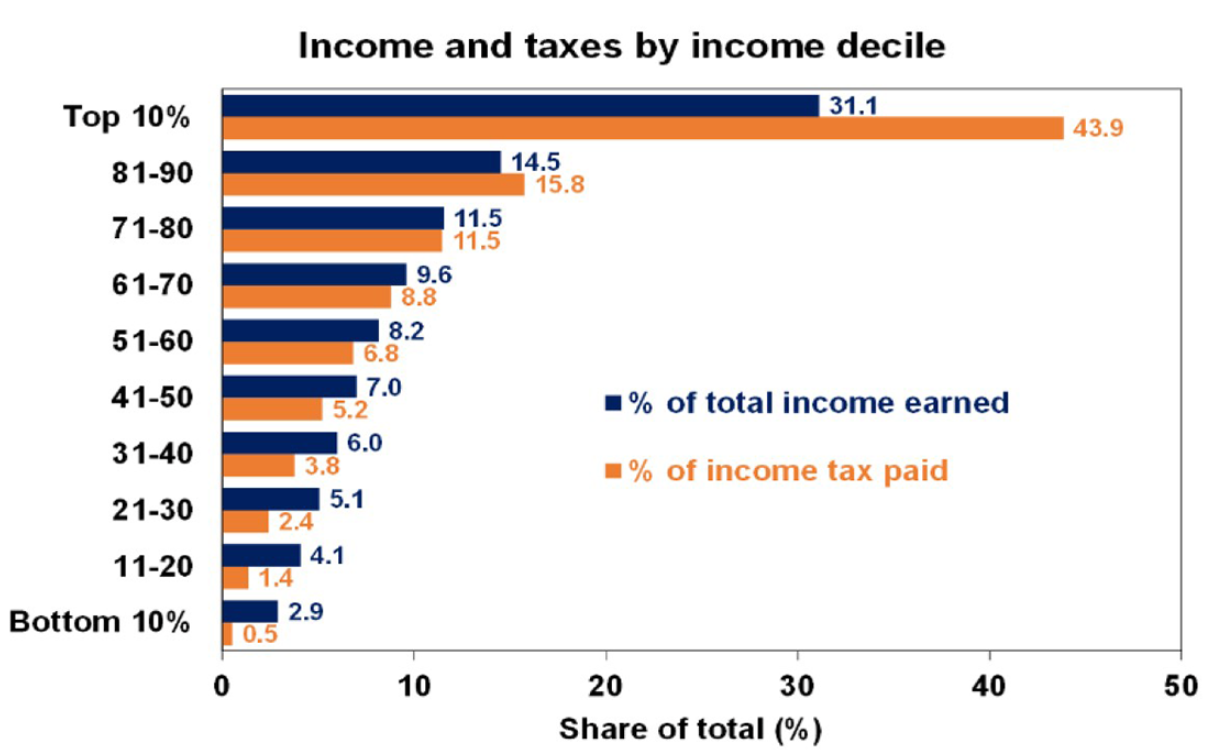

Former Treasury officials noted that the top 5% of taxpayers pay 37% of all income tax, while the top 15% pay 57%.

The top tax bracket of $190,000 has also barely moved since 2008, and bracket creep has pushed more workers into higher tax bands.

The other side of the problem is Australia’s ageing population, driven in part by the retirement of the baby boomer bulge.

As a result, the nation’s tax burden increasingly falls on the relatively shrinking pool of workers, rather than spreading more broadly.

Australia’s tax system increasingly shields wealthy retirees while relying heavily on younger workers to fund government services and rising public debt.

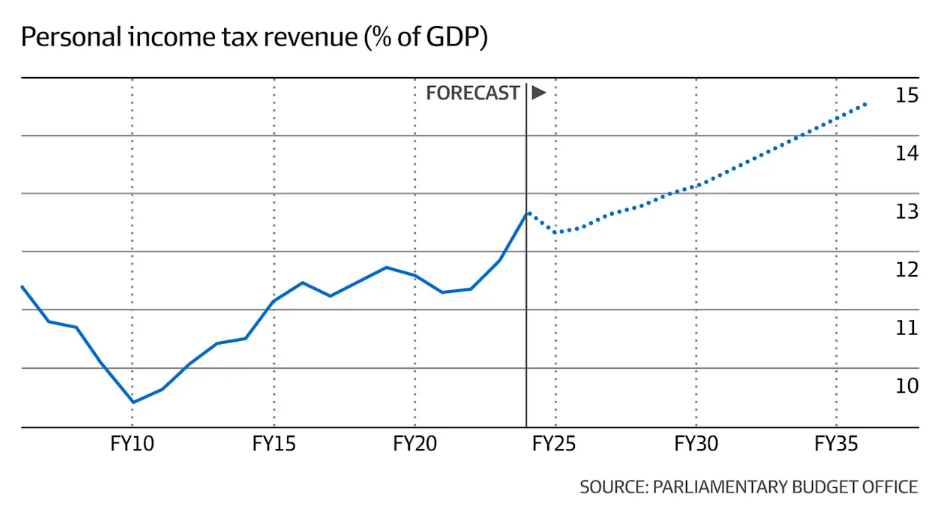

The Treasury’s Intergenerational Report said that without tax reform, personal income tax revenue would increase from about 53% of all taxes now to more than 58% in 2062-63.

Even worse, as the population ages, a smaller workforce will be responsible for paying higher personal income taxes.

Australia needs fundamental tax reform:

The Australian tax system’s reliance on a smaller share of the population paying income tax is clearly unsustainable, wasteful, and unfair.

This is especially true given that the elderly population is growing and paying lower taxes than ever before, even as they control the lion’s share of the nation’s wealth.

Australia needs comprehensive tax reform that shifts the tax base away from productive activities (taxing individuals) and towards more efficient sources such as resources, land, and consumption.

Moving the tax base away from personal income taxes would also diminish the need for large-scale immigration to raise federal income tax revenue.

The 2010 Henry Tax Review provides the reform blueprint and only needs updating.

Australia cannot afford to delay fundamental tax reform for another decade. This would jeopardise workers, intergenerational equity, and the nation’s productivity.