Thousands of rental properties have reportedly disappeared from the market following the Albanese government’s negative gearing and CGT reforms, with early data showing a sharp contraction in investor‑owned rental supply across major cities.

FoundIt data for May suggests there was a net loss of rental stock across every major East Coast market.

5,447 rental homes were sold, but only 3,915 new rental homes were purchased, resulting in a net loss of 1,532 rental properties in a single month.

FoundIt’s Kent Lardner warns that the current situation is “just the tip of the iceberg” as investors continue to digest the reforms.

Reporter Aidan Devine claims that landlords now have more pricing power, which will inevitably harm renters:

“Competition in Australia’s rental market has intensified in the first month since the government announced landmark capital gains tax and negative gearing reforms in the May federal budget”…

“And, with long queues of tenants often the norm at weekend rental inspections, that’s given existing landlords grounds to charge more rent”.

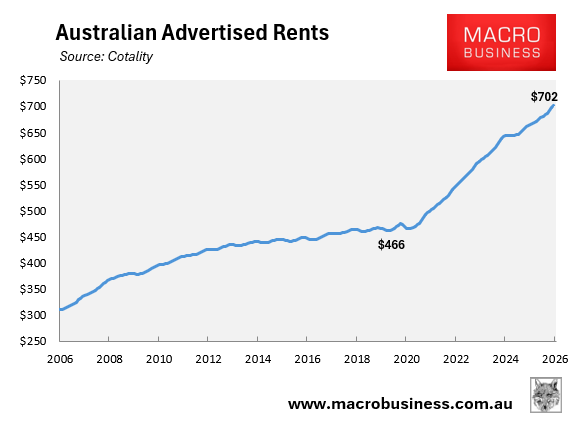

The reality is that Australian rents have already surged over the past four years due to the federal government’s record net overseas migration.

The empirical evidence also does not support the suggestion that an investor exodus will drive up rents.

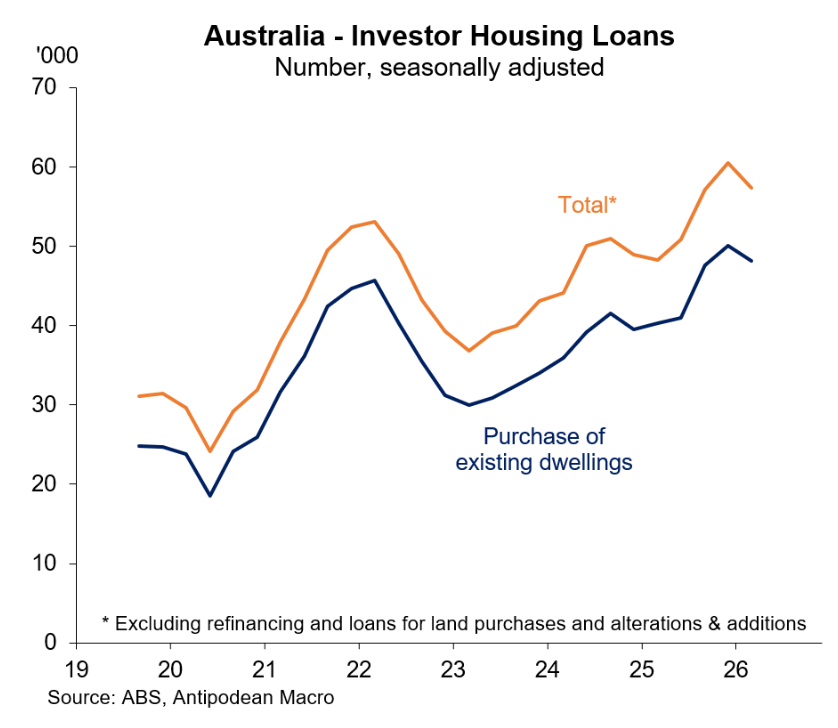

More than 80% of investor mortgage commitments are for established homes. Therefore, fewer than one out of five investors are adding to housing supply:

Most investors, therefore, have turned homes for sale into homes for rent.

When an investor sells, the property does not vanish. Rather, it will either be purchased by another investor or by an owner-occupier (possibly a first-home buyer).

Therefore, if fewer investors participated in the market, or if investors sold up following the budget’s negative gearing and CGT changes, there would be fewer homes for rent, but also fewer people needing to rent, as more owner-occupiers would be in the market.

The rental supply-demand balance would be largely unaffected.

Moreover, negative gearing and CGT have been retained for newly constructed homes, which should add to supply over the longer term.

Victorian data suggests fears of an investor exodus are overblown:

In 2024, the Victorian government significantly increased holding costs for investors—primarily through lower land‑tax thresholds, expanded vacant‑residential‑land taxes, and new short‑stay levies.

The changes mean more investors now pay land tax, and those who already pay are paying more, reducing net yields.

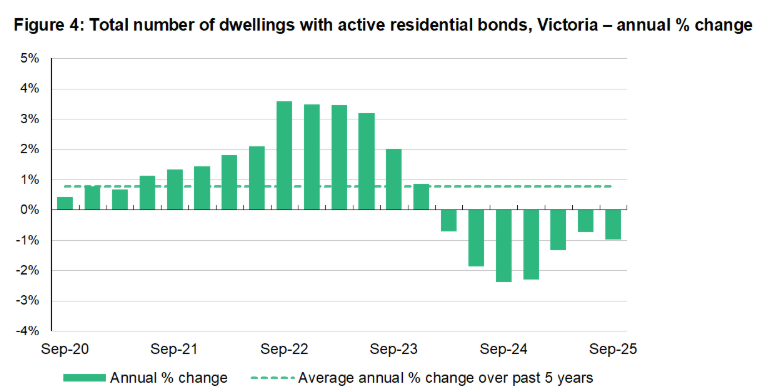

As a result, a significant number of investors abandoned the market, as evidenced by the decrease in rental bonds on issue:

Despite the exodus of investors, Melbourne’s rental market has fared far better than the other major capital cities.

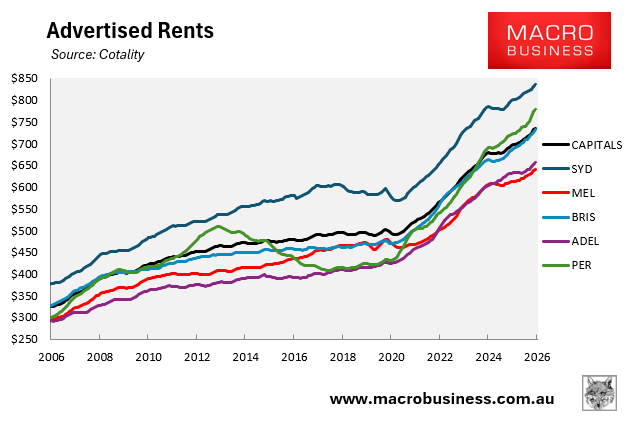

According to Cotality, Melbourne advertised rents grew by 37% in the five years to May 2026, significantly below the 42% growth recorded across the combined capital cities:

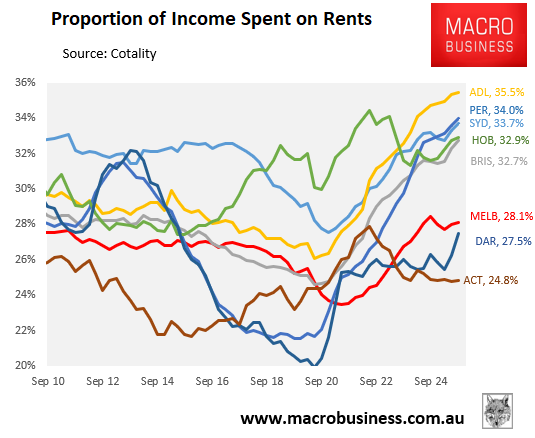

The amount of income required to rent the median home in Melbourne was 28.1% in Q3 2025, significantly below the other major capital cities and the national average of 33.4%:

Victoria’s dwelling construction rate is also tracking well above the other states, suggesting the investor tax changes haven’t harmed supply.

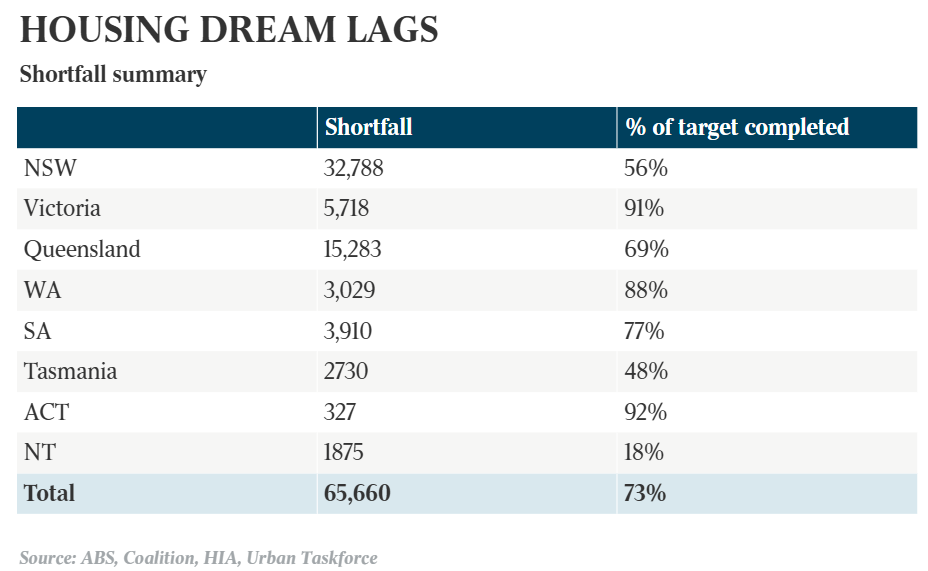

As illustrated below, Victoria is the only state to be tracking close to the National Housing Accord supply target:

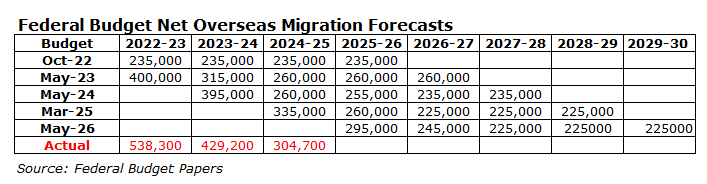

Ultimately, excessive immigration into a supply-constrained market is the primary driver of Australia’s rental crisis. And the latest federal budget has just upgraded migration by 55,000:

Renters should be angry about excessive migration, not the changes to negative gearing and CGT.