Financial markets backtrack on RBA rate hikes

Recently, two major banks – CBA and NAB – have pivoted on interest rates and now expect the Reserve Bank of Australia (RBA) to keep the official cash rate on hold until mid-next year before delivering cuts.

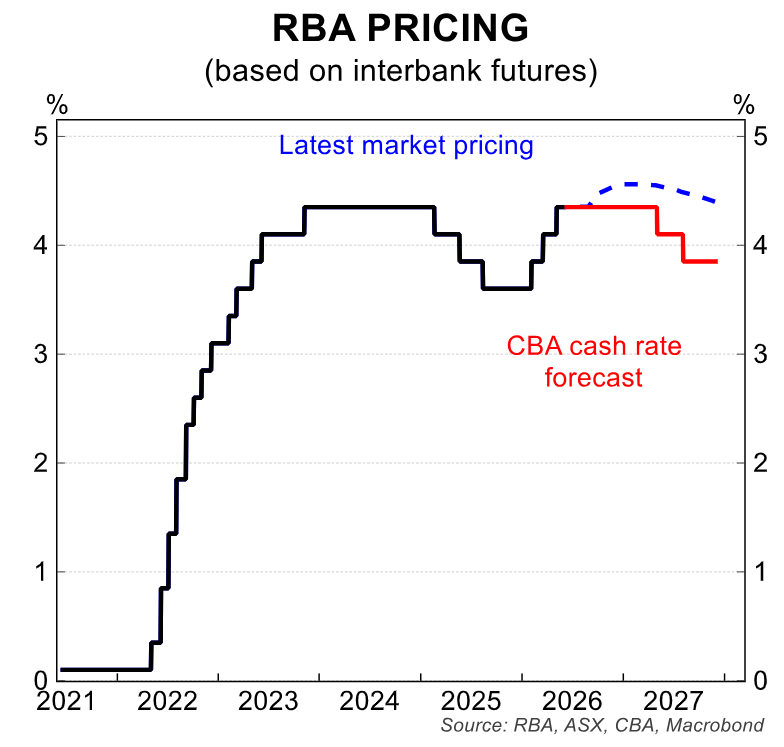

CBA expects the RBA to remain on hold at 3.35% until early 2027, followed by 25 bp cuts at next year’s May and August monetary policy meetings:

NAB also expects the RBA to remain on hold before beginning an easing cycle in the first half of next year.

NAB forecasts that the official cash rate will settle at 3.60% by the end of 2027, implying that the RBA will reverse this year’s three rate cuts and return the official cash rate to its February level.

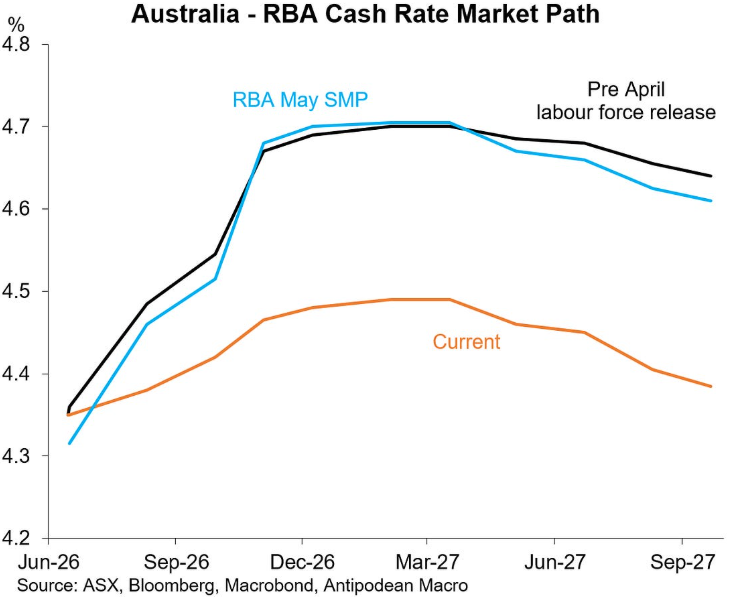

The interest rate futures market has also become more dovish, pivoting from expecting two more rate hikes this year to a less than 100% chance of one more rate hike this year, as illustrated below by Justin Fabo from Antipodean Macro:

The interest-rate futures market is currently pricing an official cash rate of 4.50% by the end of 2026, suggesting a 60% chance of one more rate hike.

By the end of 2027, the futures market forecasts the official cash rate at its current level of 4.35%, which is obviously higher than what CBA and NAB are pricing.

I share the view that the RBA will remain on hold and that the next move in rates will be down.

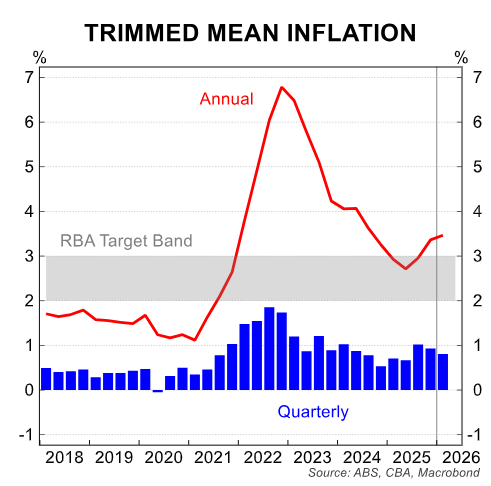

While inflation remains above the RBA’s 2% to 3% target band, it would likely take solace in the fact that the housing market has stalled, with values now trending lower across the combined capital cities.

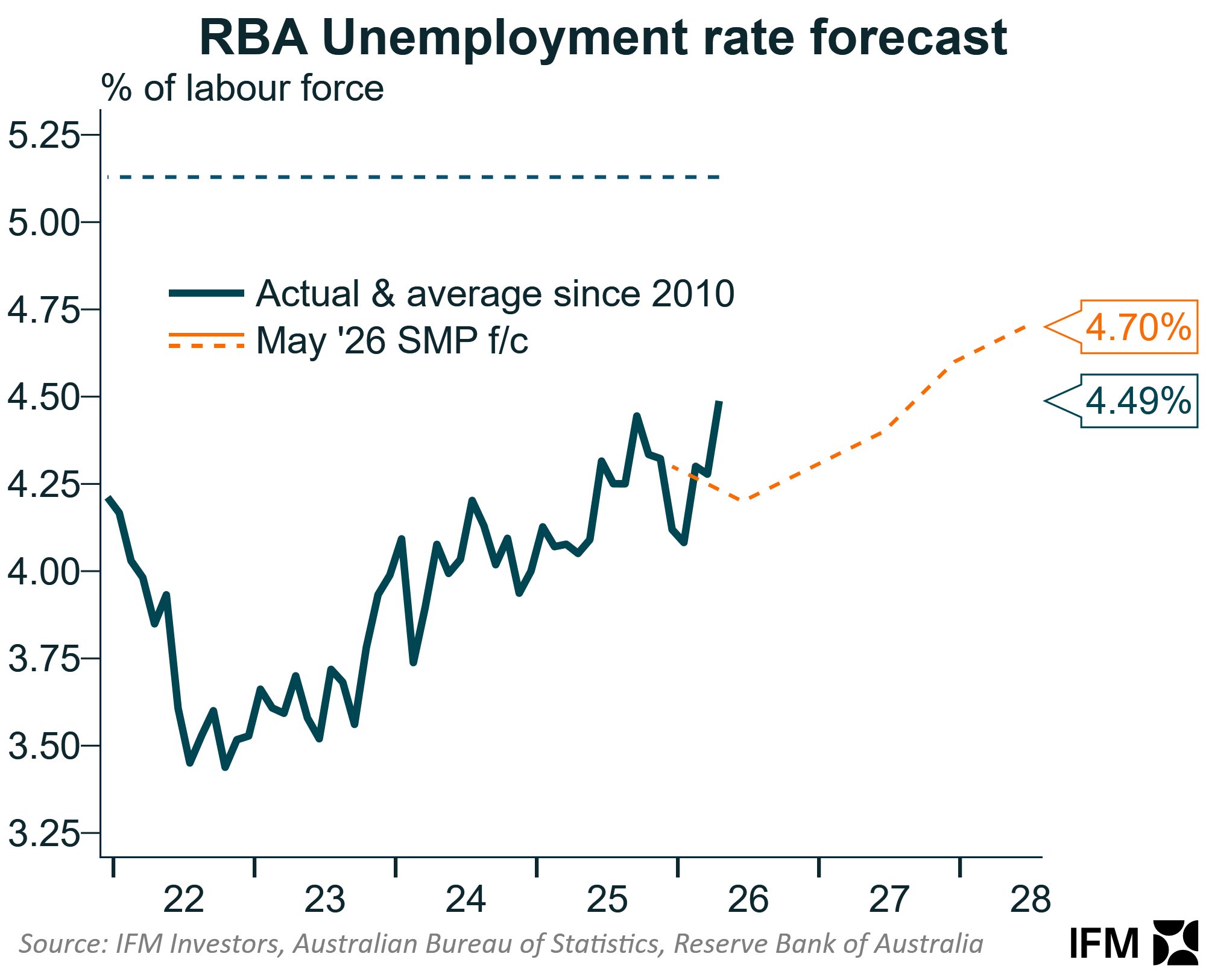

Australia’s unemployment rate is also rising faster than the RBA had forecast, with the economy entering another per capita recession following a 0.1% decline in per capita GDP in the March quarter.

The data, therefore, suggests that the economy is softer than the RBA had anticipated and that monetary policy is already restrictive.

For months, I have argued that the RBA would tighten too much this year and then cut next year as the economy teeters on the brink of recession.

The slowing economy, rising unemployment, and falling home prices will likely force the RBA to cut interest rates, even if inflation remains above target.