CGT changes should be restricted to residential property

Amid widespread criticism of the federal budget’s changes to capital gains taxes (CGT), the Albanese government last week announced that businesses with turnover of up to $10 million will be eligible for a CGT discount of 50% on the sale of active assets, up from the current revenue threshold of $2 million.

In addition, the government will provide an exemption from the new CGT rules for owners and employees of start-ups deemed to be “innovative business”, and has agreed to concessions regarding the tax treatment of testamentary trusts to mitigate the impact on deceased estates.

Despite the amendments, opposition remains steadfast.

For example, Australian Chamber of Commerce & Industry (ACCI) CEO Andrew McKellar says the federal government’s partial changes to its budget reforms are “a rushed patch-up job”. He added that the changes aim to push the legislation through parliament with as little scrutiny as possible.

The ACCI has sent a letter to all MPs and senators calling on them to “consider the impacts of penalising investment in businesses in your own community”.

Western Australian Premier Roger Cook and state Treasurer Rita Saffioti will also meet with Prime Minister Anthony Albanese and Treasurer Jim Chalmers on Monday. Saffioti will ask for mining exploration companies to receive similar concessions from the federal government’s capital gains tax that were granted to start-ups last week.

Saffioti contends that mining exploration companies are the ‘original start-ups’, while the Association of Mining & Exploration Companies is hoping the Greens will back its case for mining exploration companies to receive favourable treatment under the CGT changes.

I support the CGT changes on established residential property but believe that non-residential assets should continue under the old 50% discount regime.

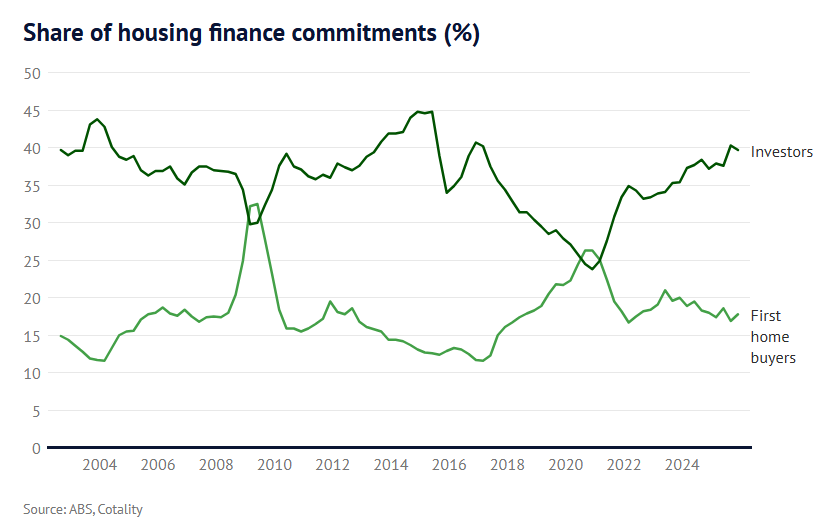

The fact of the matter is that there are negative externalities for purchase affordability when a property investor buys an established home, since they often out-compete and crowd-out a first home buyer and place upward pressure on dwelling values:

No such negative externalities exist regarding non-residential assets, since nobody lives in shares or a business.

Therefore, it makes sense to run a more punitive tax regime for established housing than other asset classes on affordability and equity grounds.

However, operating one of the world’s most punitive CGT regimes on non-residential assets is harder to justify and risks increasing complexity and undermining overall entrepreneurship and business investment.