First home buyers (FHBs) who entered the market recently with very small deposits under Labor’s 5% deposit scheme are now the group most exposed to rising interest rates and falling home prices, especially if they purchased in Sydney or Melbourne.

Three RBA rate hikes in six months have pushed FHB mortgage delinquencies to a seven‑month high, according to Equifax, with 90‑day arrears among FHBs nearly double those of other borrowers.

The expansion of the FHB 5% Deposit Scheme on 1 October 2025 triggered a surge in applications, especially among 18–25‑year‑olds (+22.8%).

However, the small-deposit cohort is now the most vulnerable, with those who bought with only a 5% down payment at risk of having no equity left if forced to sell, while also paying higher mortgage repayments following three rate hikes.

Many buyers who purchased earlier with larger deposits have seen 10–20% price growth and are in a safer position.

Equifax reports FHB 30‑day arrears across the main states as follows:

- Victoria & WA: 0.89%

- NSW: 0.75%

- SA: 0.69%

- Queensland: 0.66%

Non‑first‑home buyers are faring much better, with arrears mostly around 0.3–0.5%.

“The challenge is for buyers who entered with only a 5% deposit — if they are forced to sell, there is a strong chance the money they originally put into the property may no longer be there”, Equifax Chief Solutions Officer Kevin James said.

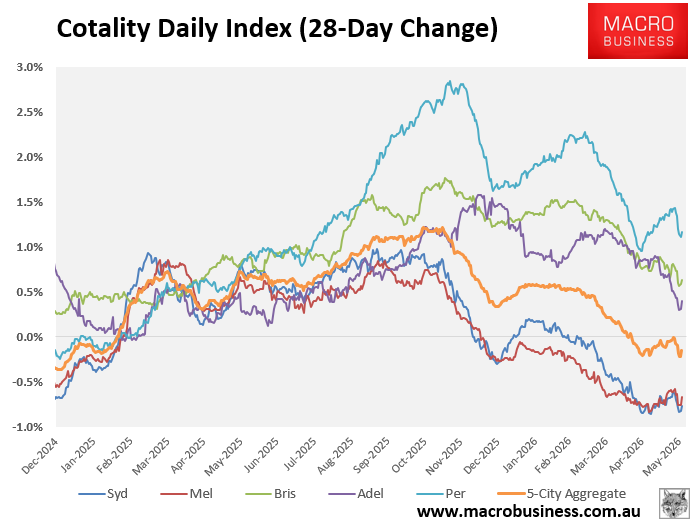

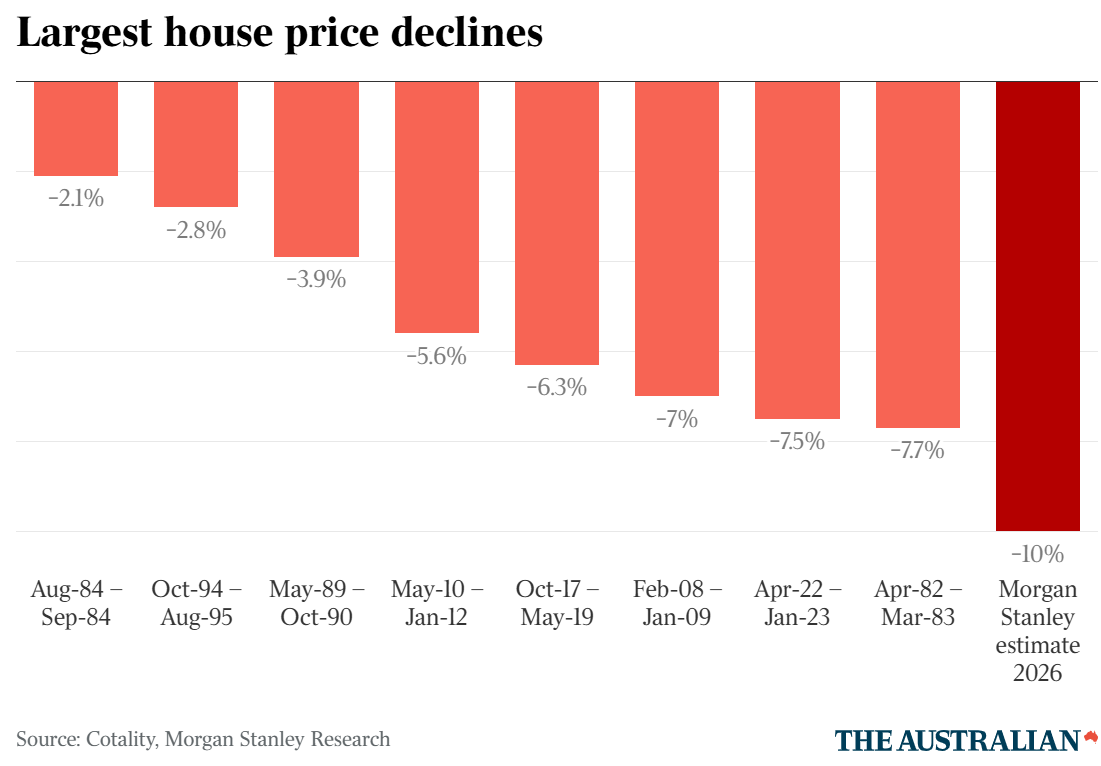

Morgan Stanley warned last month that Australia’s housing market could experience a national 10% decline in values, the largest in at least 40 years.

A 10% decline from peak nationally would obviously wipe out the equity of many recent FHBs who utilised the 5% deposit scheme to enter the market.

After enticing them into the market in late 2025, the Albanese government has now pulled the rug from under them with its negative gearing and capital gains tax changes, which promise to exacerbate the house price correction.

While these changes to property investment taxes will help future FHBs by lowering prices and reducing competition from investors, they will drive recent FHBs who utilised the 5% deposit scheme into negative equity.