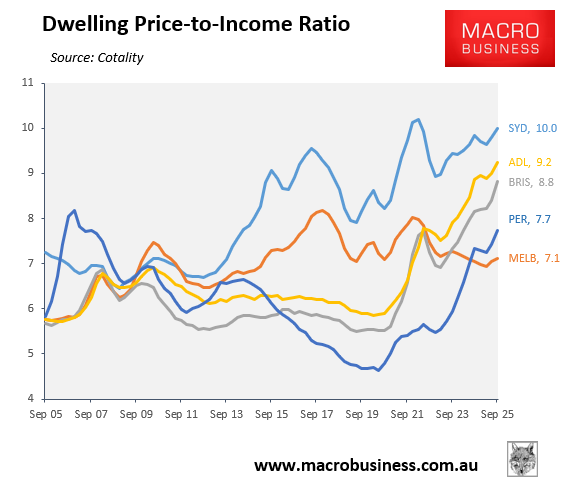

Before the Reserve Bank of Australia (RBA) commenced its monetary hiking cycle in February, Sydney’s housing market was experiencing the nation’s worst affordability.

At the end of 2025, Cotality reported that Sydney’s dwelling price-to-income ratio was 10.0, well above the capital city average of 8.8:

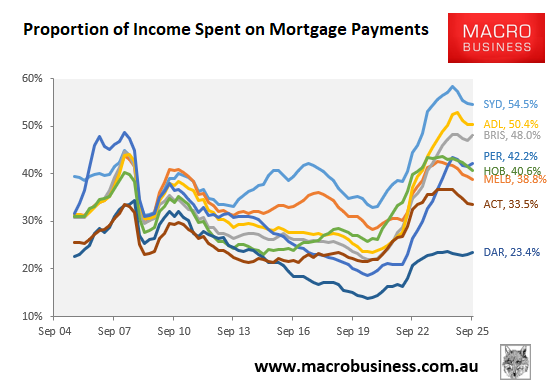

The percentage of median household income required to service the typical new mortgage in Sydney was also 54.5% at the end of 2025, significantly higher than the capital city average of 45.0%:

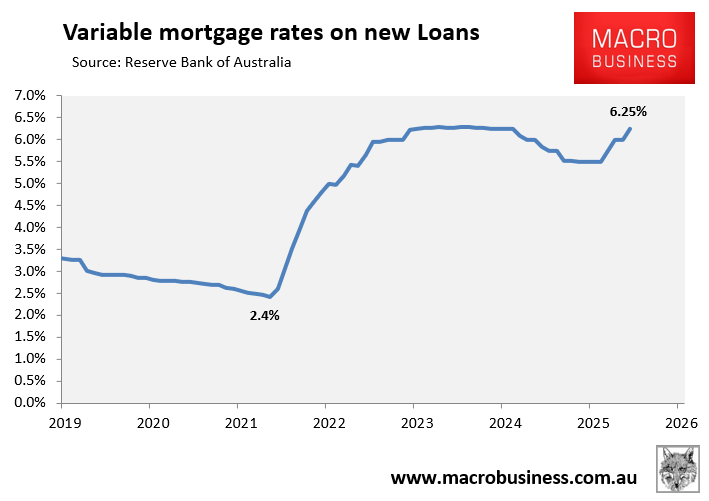

Since the end of 2025, the picture has clearly worsened following three consecutive interest rate hikes by the RBA, which have sent variable mortgage rates to their highest level in more than a decade.

As a result, mortgage repayments relative to income have risen, pressuring cash-strapped households.

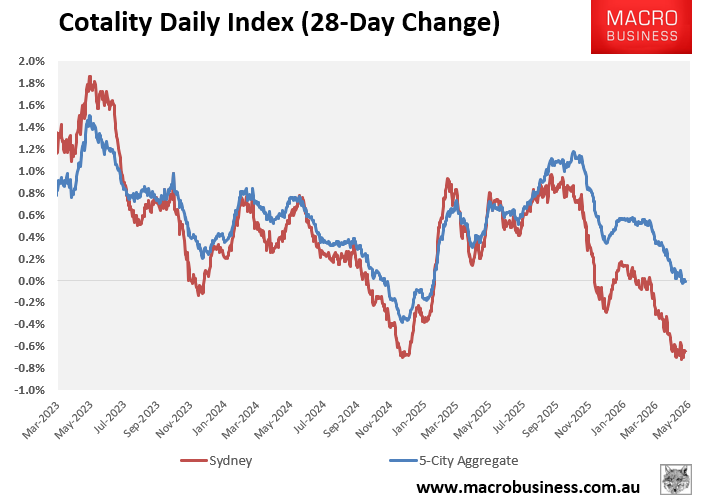

Meanwhile, Sydney dwelling values are now falling, down by 1.5% over the past three months, according to Cotality:

The Australian reports that mortgage stress is no longer confined to the outer‑suburban mortgage belt, spreading into affluent, traditionally low‑risk areas such as Sydney’s North Shore, affecting both middle-Australia and wealthier suburbs.

Stress is now entrenched in dual‑income, middle‑ring suburbs that borrowed heavily during the low‑rate era.

“We are increasingly seeing stress emerge across dual-income middle-ring suburbs where borrowers took on large debts during the low-rate environment and are now adjusting to structurally higher repayment costs”, Research adviser Mansour Soltani said.

The federal budget’s changes to negative gearing and capital gains tax are expected to intensify the pressure.

Banks are tightening investor lending, reassessing serviceability and risk models.

Stress was already rising before the tax changes — meaning the policy shift could amplify existing fragilities.

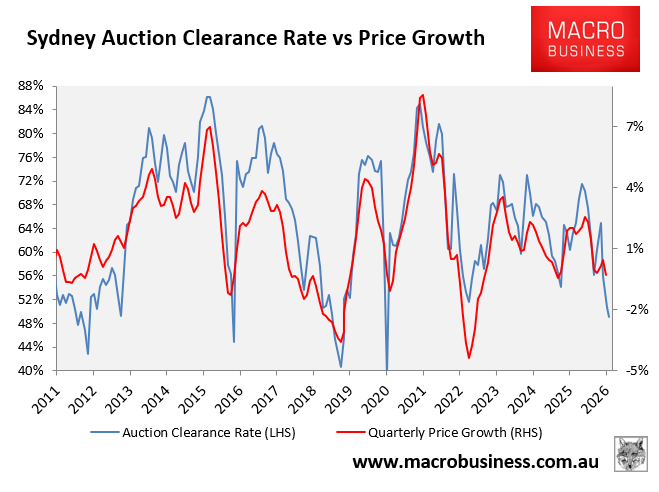

Sydney auction clearance rates have plunged, reflecting investor‑heavy stock.

First-home buyers who purchased in Sydney late last year using the Albanese government’s 5% deposit scheme are especially exposed, since they borrowed very large sums (up to 95% LVR) just prior to the RBA hiking rates three times and prices falling.

Many now face the prospect of holding mortgages they can no longer afford to service and properties valued below their purchase price (i.e., negative equity).