In April, stock markets boomed. The key question remains whether US profit growth (~20% forecast for each of the next two years) will stay incredible or if it will become non-credible in the face of rising energy costs. We switched our tactical portfolios back into stocks mid-month as soon as the ceasefire was announced.

The Iran war is dominating headlines and asset allocation. The worst-case scenarios would be devastating for stock markets. But, given the strength of current earnings, any semi-reasonable resolution (or even an uneasy detente) will be positive for stock markets.

The Two-Speed Economy: Look Beyond the ASX

We are living in a K-shaped global economy.

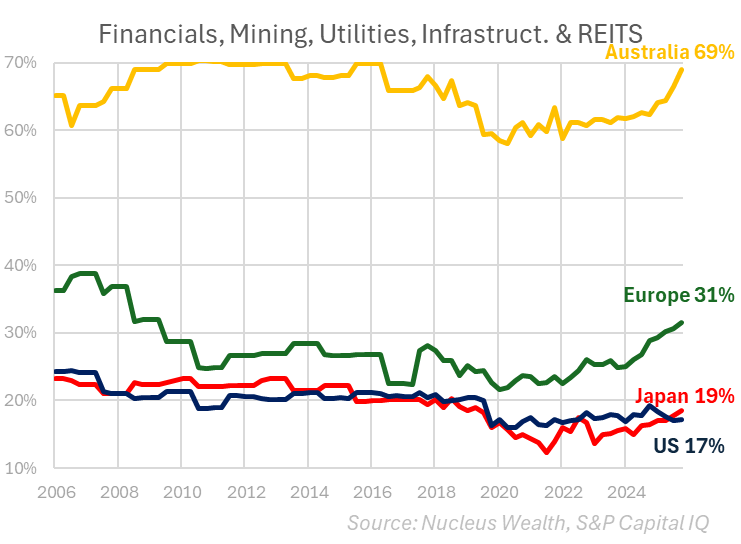

The Australian Dilemma: A Market of Rent Seekers

Let’s be honest about the structure of the Australian economy. It is highly dependent on two things: digging commodities out of the ground and selling houses to each other.

The US AI Earnings Boom: Real Cash, Real Growth

Contrast the Australian market with what is happening in the US.

The Unstoppable Energy Transition

It isn’t just technology that is shifting rapidly; the very foundation of global energy is undergoing a revolution that is “hockey-sticking” faster than most people realise.

Furthermore, the supply chain for this transition is scaling exponentially. With traditional infrastructure like coal or gas, you can build a 10 MW power plant in one year, but then you have to start from scratch to build the next one.

With solar and batteries, the factories are the 2nd derivative. A factory producing 10 MW of solar panels will produce another 10 MW next year. And here is what has been missed: the factories have already been built.

- Approach manufacturers with caution: The solar panel and battery manufacturing sector is difficult. It is heavily government-sponsored and subsidised, meaning it will not operate as a true “free market” for decades. As an investor, your gains in this space will largely depend on whether your domestic government or the Chinese government is feeling more accommodating at any given moment.

- Bet on the change: Stick with the service and infrastructure companies enabling the transition—the “picks and shovels” of the grid. These same companies will be involved extending the lives of existing power plants. The best plays in this sector tend to be international stocks like ABB or Schneider, but there will be some ASX stocks that benefit.

- The fossil fuel endgame: Legacy fossil fuel companies are likely about to make super profits in the short term, driven by underinvestment and supply constraints. Take those profits if you hold them, but be warned: the end is coming much faster than linear forecasts suggest. There is a good short-term argument to use these stocks as a hedge for the Hormuz Strait being closed. But it is not a forever bet.

The Geopolitical Wildcard: Oil and the Strait of Hormuz

Of course, the global economy isn’t without its dark clouds.

How to Position Your Portfolio

In a world defined by Australian domestic struggles, sticky inflation, and a US-led technological revolution, how should the savvy investor position their wealth?

- Look Beyond Australia: The ASX is heavy with rent-seekers and light on genuine innovation. To capture the extraordinary earnings growth of the current decade, overweight international equities.

- Embrace the AI Value Chain: You don’t have to buy the most expensive, hyped-up tech stocks. Look across the entire value chain—from the companies building the data centres, to the chip manufacturers, to the businesses leveraging AI to dramatically reduce their operating costs.

- Acknowledge the energy transition: Energy systems are changing. Countries no longer want to be dependent on a troubled Middle East or Russia (or a mecurial USA?). Battery and solar annual production has already grown exponentially. Existing energy is having its life extended.

- Protect Against Sticky Inflation: We are moving into an era of higher nominal interest rates and lower real interest rates. Central banks will tolerate slightly higher inflation because they cannot afford to completely crush their heavily indebted economies. Protect your defensive allocations by utilising inflation-linked bonds rather than relying solely on traditional fixed interest.

The Asymmetry of Hope

The problem? The distribution of outcomes is not a neat bell curve. It’s a cliff.

- Upside: If a deal is struck, we are looking a markets that are a little expensive and extremely high earnings growth. A reasonable trade-off.

- Default course: We are in an interminable standoff of “almost” deals and extended deadlines. But, if enough ships get through, energy prices are high but not catastrophic, then there is a navigable path for stock markets.

- Downside: Extreme. At the other end of the spectrum lies $200+ oil and a deep, structural global recession as energy supply chains are physically smashed.

Net effect: Are we headed for the greatest corporate profit boom of our generation? Or a deep recession driven by rampaging energy prices.

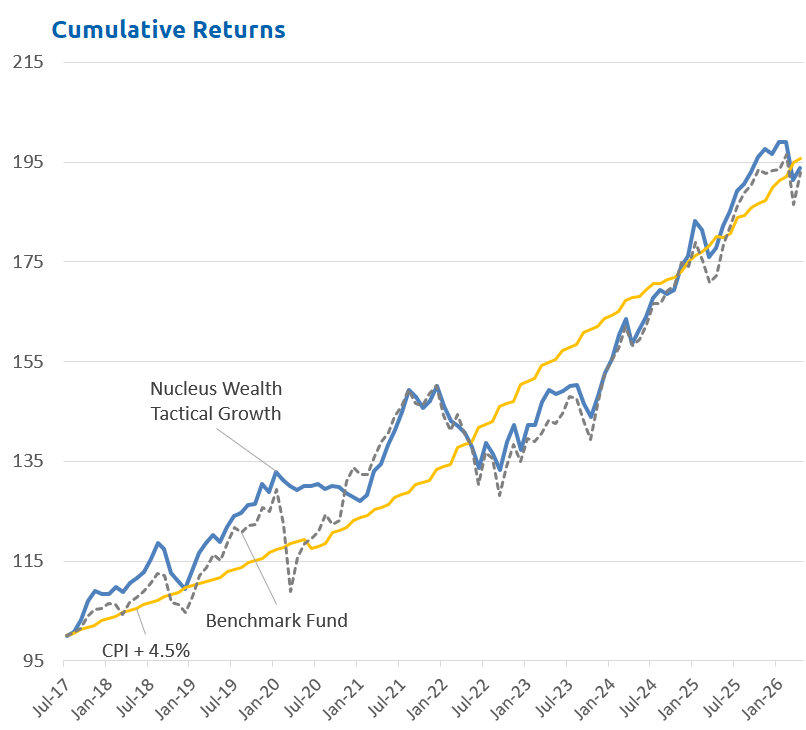

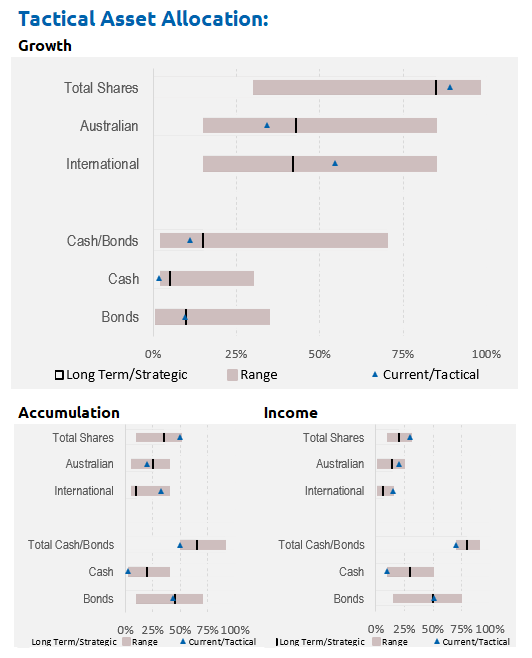

Asset allocation

Bought back into shares during the month and ended overweight shares. We are overweight inflation linked bonds. At the end of the month, the growth in international meant our allocation to shares was high:

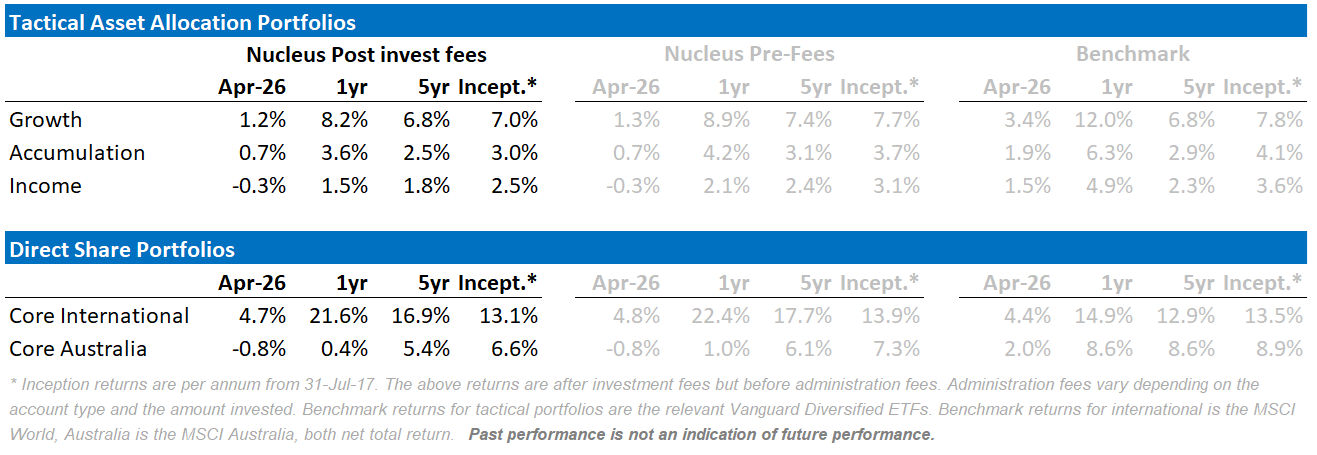

Performance Detail

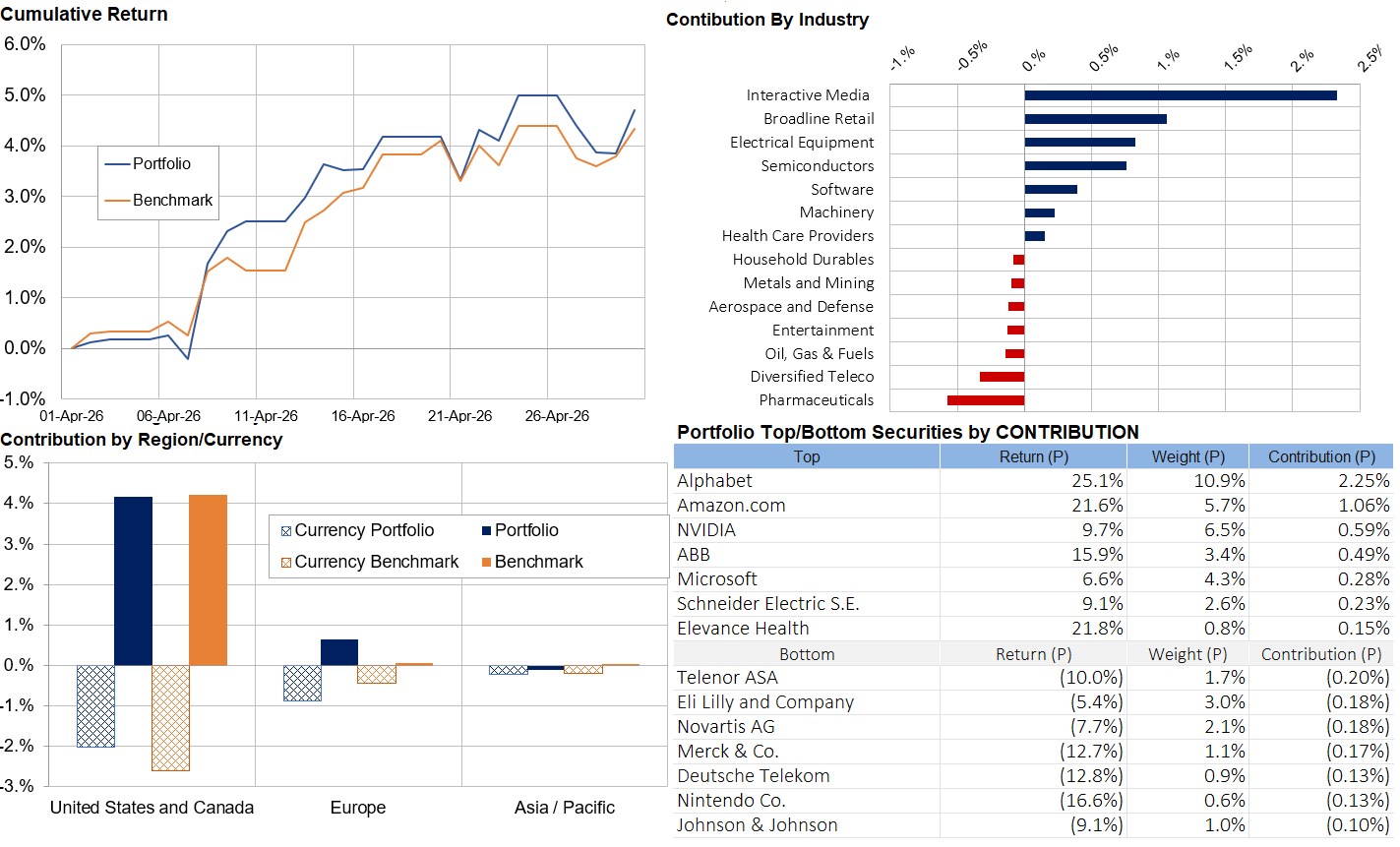

Core International Performance

The announcement of a temporary ceasefire in the Iran war saw markets rally on the increased prospect of some form of conclusion. Technology and Growth stocks bounced while Defensive stocks gave back some recent gains. Currency turned as well as the USD strengthened.

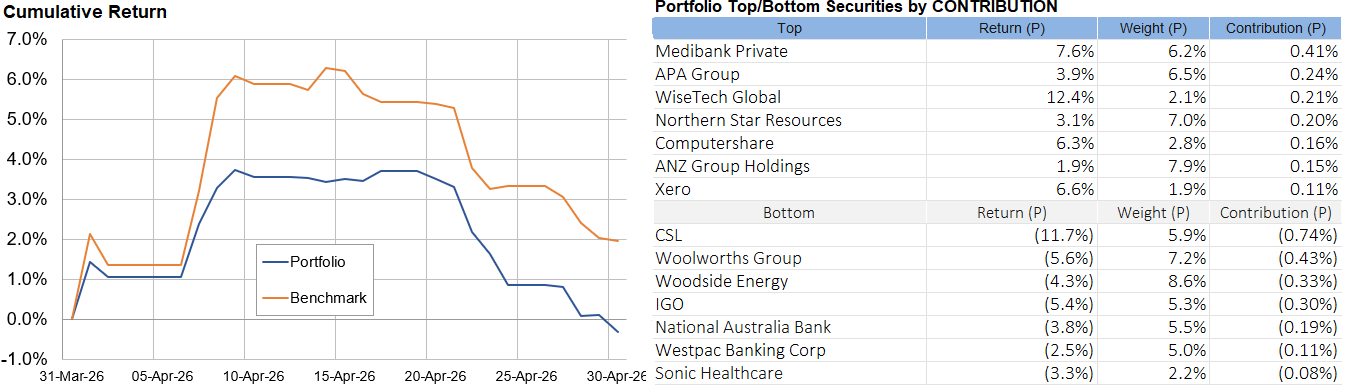

Core Australia Performance

Growth stocks bounced while Defensive and Oil & Gas stocks waned especially CSL.

Damien Klassen is Chief Investment Officer at the Macrobusiness Fund, which is powered by Nucleus Wealth.

Follow @DamienKlassen on X(Twitter) or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an Authorised Representative of Nucleus Advice Pty Limited, Australian Financial Services Licensee 515796. And Nucleus Wealth is a Corporate Authorised Representative of Nucleus Advice Pty Ltd.