The Albanese government’s changes to negative gearing and capital gains tax (CGT) are designed to make housing more affordable for first home buyers (FHBs) by reducing investor participation in the market.

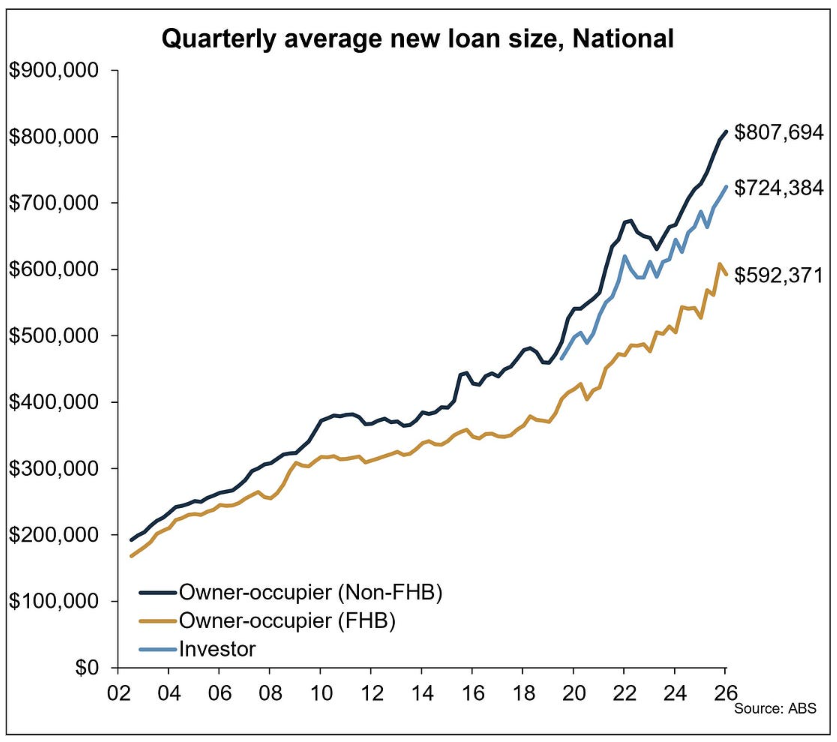

As illustrated below by Cameron Kusher at Oz Property Insights, in the March quarter of 2026, the average loan size for an investor was 22.3% higher than that for an owner-occupier FHB, equating to an average premium of $132,012.

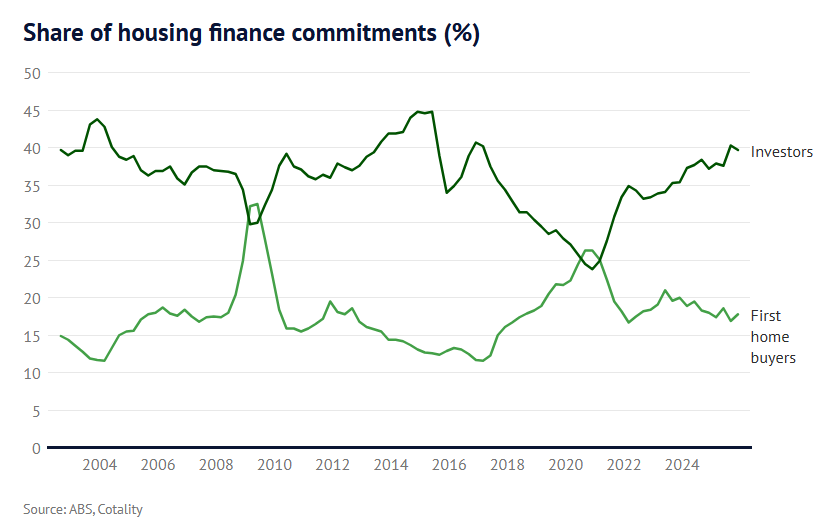

The following chart from Domain also shows a near-perfect negative correlation between investor mortgage demand and FHB mortgage demand.

This data suggests that investors have crowded-out FHBs from the housing market.

Therefore, lower investor demand should result in more FHBs entering the market and a higher home ownership rate.

The Australian Treasury’s Budget explainer on the negative gearing and CGT changes suggested that house price growth will be around 2% lower over a couple of years than it otherwise would have been. However, I believe this forecast is overly optimistic.

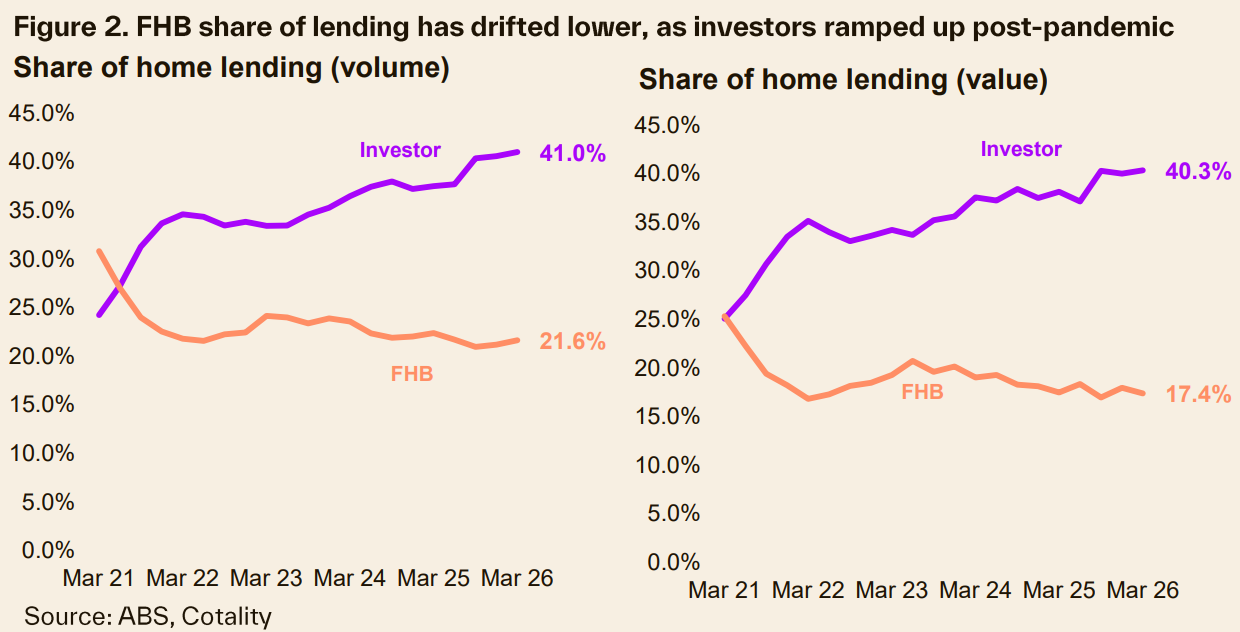

Cotality has released research showing that the investor share of total lending rose in March. In volume terms, the investor share was at a record high of 41.0%, whereas in value terms it was at 40.3%, its highest share since December 2016:

Again, the above chart shows a negative correlation between investor mortgage share and FHB mortgage share.

Cotality notes that investor mortgage demand will slow due to the Budget’s changes to negative gearing and CGT:

“Policy changes in this year’s Federal Budget are likely to have a negative impact on investor demand, and by extension, new investor loans”.

“The removal of negative gearing for purchases of existing properties is likely to reduce investor lending on a net basis; while some new investors may be drawn to purchase newly constructed properties (where negative gearing is retained), they have historically favoured existing dwellings and may now look to other (non- property) assets instead”.

“With rental yields well below the cost of borrowing (particularly if interest rates rise further), fewer investors into existing properties would be able to generate a positive cashflow, meaning that the costs of holding these assets are now substantially higher and serviceability challenges more prominent”.

I will add that with investors comprising such a large share of the home loan market – i.e., around 40% in the March quarter – any downshift in demand from this cohort will necessarily have a significant negative impact on home values.

Certainly, the impact is likely to be far higher than the circa 2% price adjustment forecast by the Australian Treasury.