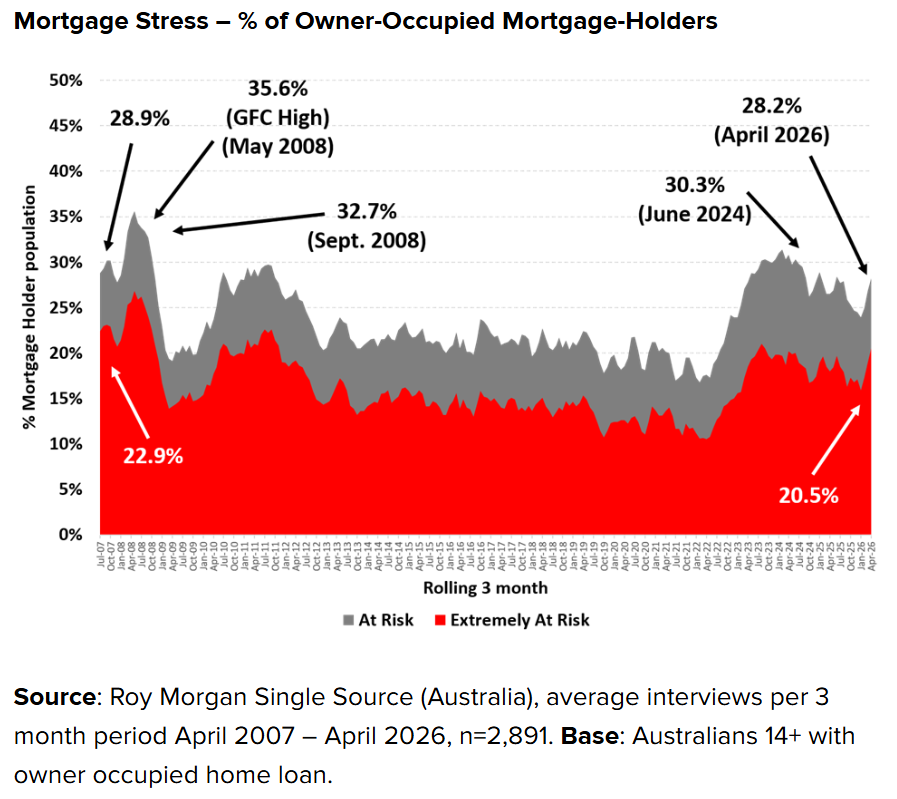

Australian mortgage stress poised to hit 14 year high

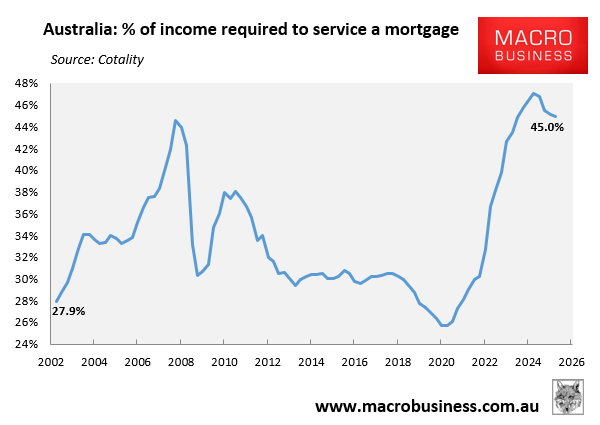

According to Cotality, 2026 began with Australians required to dedicate a near-record share of their income to servicing a new mortgage.

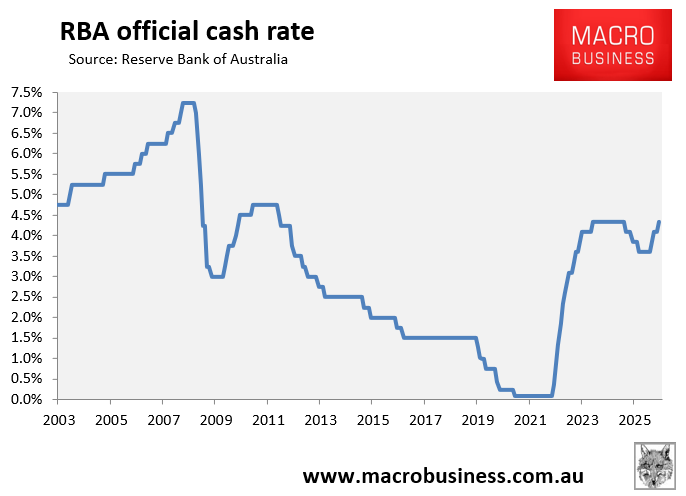

Since then, the Reserve Bank of Australia (RBA) has increased the official cash rate three times to 4.35%, the same level as the prior peak.

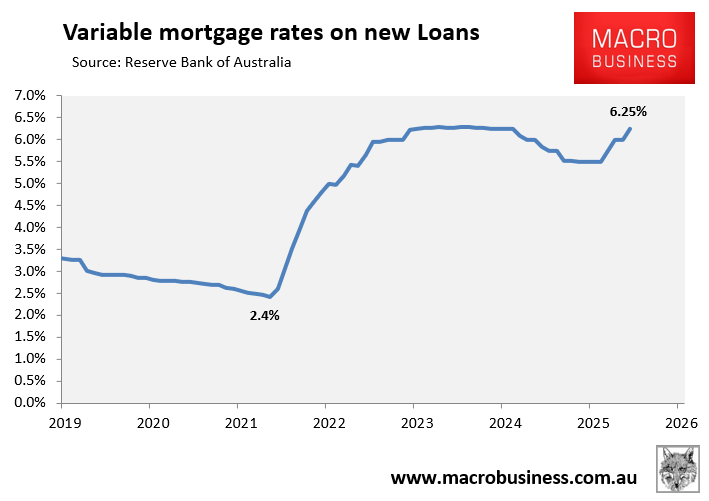

As a result, the discount variable mortgage rate on new loans has increased to 6.25%, which is well above the historical pandemic low of 2.4%:

The interest rate futures market is now fully pricing one more increase in the official cash rate to 4.60% by the end of the year, which would take the cash rate to a 15-year high and increase the discount variable mortgage rate to 6.50%.

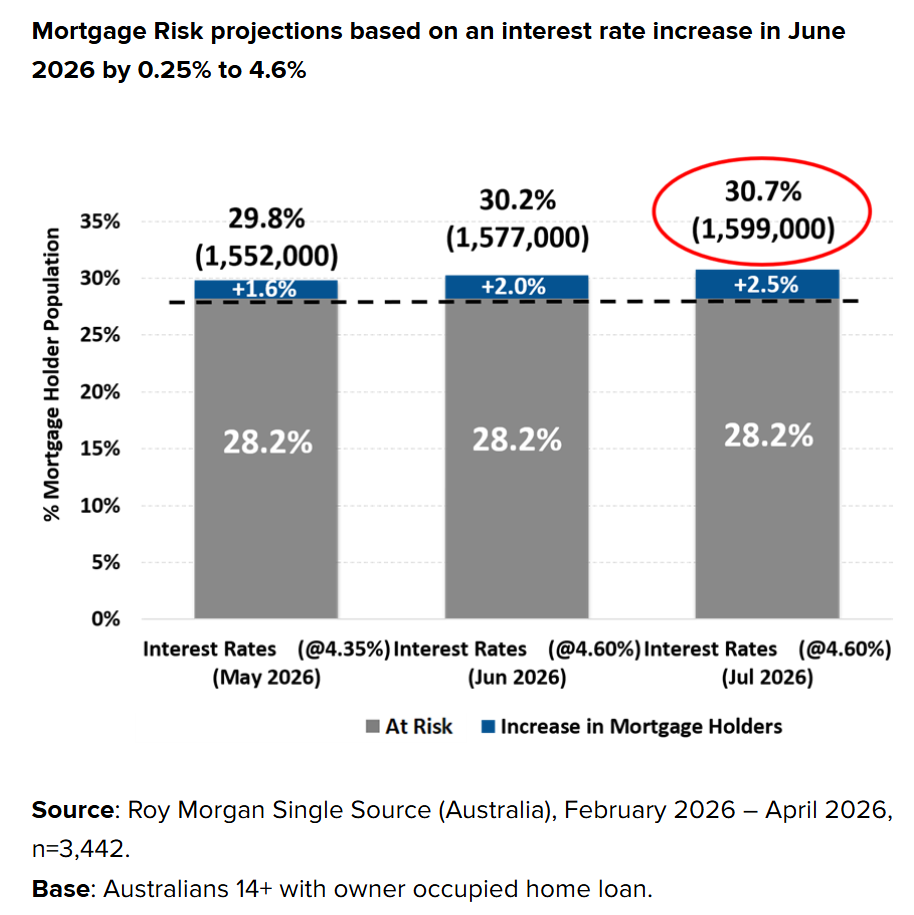

Roy Morgan has released new modelling suggesting that if the RBA does deliver one more interest rate hike, then the share of households at risk of mortgage stress would rise to 30.7%, with nearly 1.6 million mortgage holders at risk:

This would represent the highest share of mortgage holders in stress in around 14 years, according to Roy Morgan:

Roy Morgan explains that it “uses a conservative forecasting model, essentially assuming all other factors apart from interest rates remain the same”. However, Roy Morgan notes that “unemployment is the key factor which has the largest impact on income and mortgage stress”.

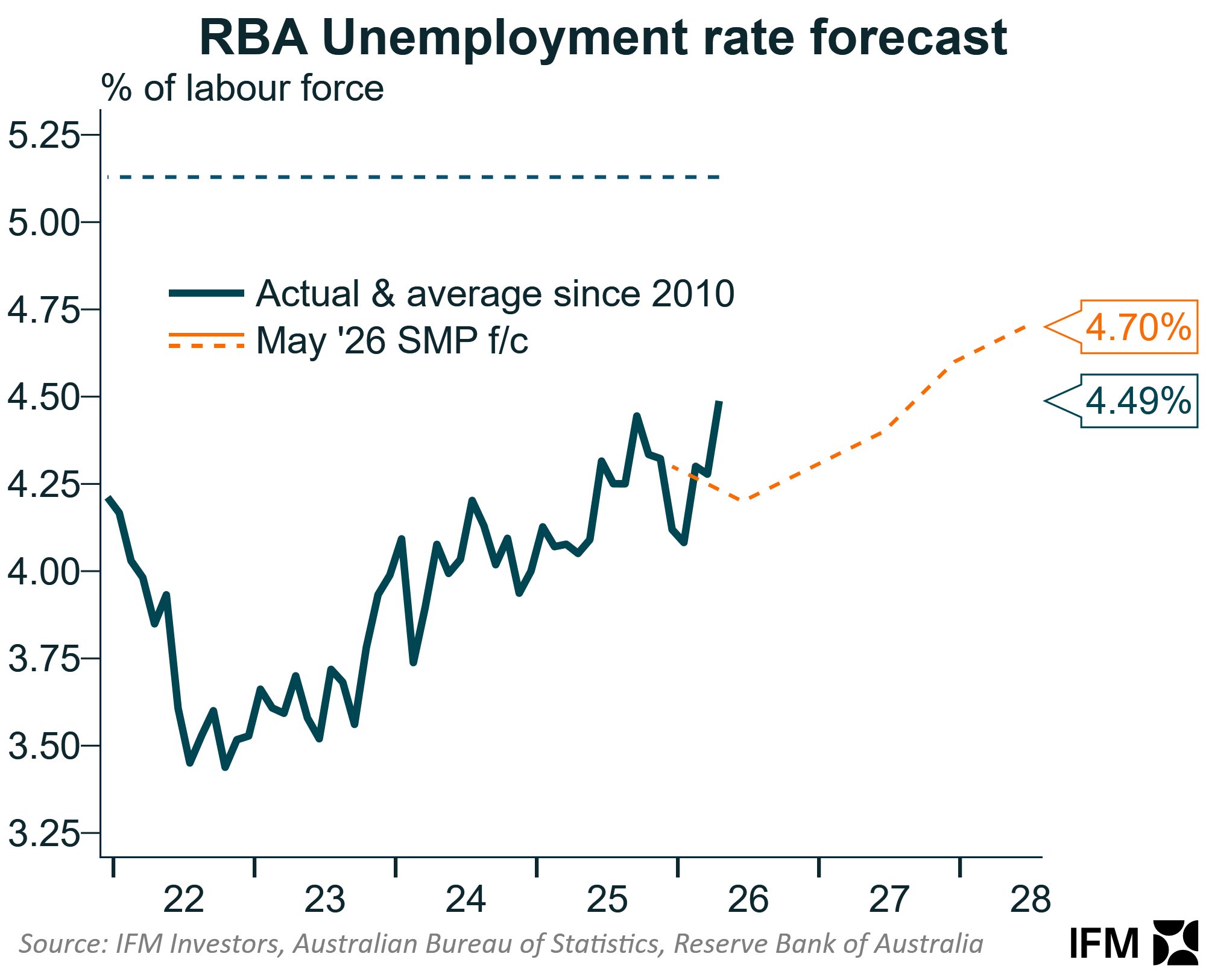

Australia’s unemployment rate has recently risen to its highest level since late 2021 and will likely rise further amid interest rate hikes, the slowing economy, the rollout of AI, and ongoing strong immigration.

Chart from Alex Joiner at IFM Investors

As a result, Australia faces a sharper rise in mortgage stress if unemployment continues to rise.

First home buyers who recently purchased using the Albanese government’s 5% deposit scheme are most at risk of falling into financial stress, since they borrowed large amounts (LVRs of up to 95%) and have seen mortgage rates rise and, in Sydney and Melbourne, home prices fall.