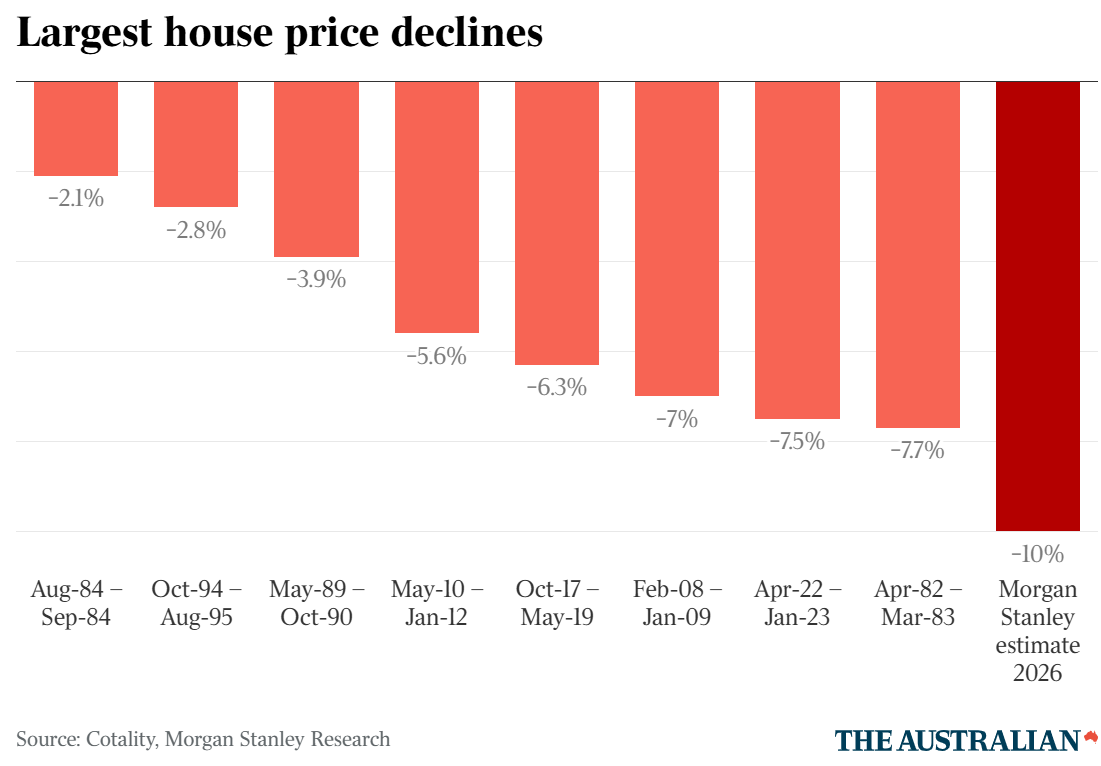

Earlier this month, I wrote an article entitled “Australian house prices poised for largest decline in 40 years”, explaining why the housing market is facing a generational decline.

My analysis has received support from Morgan Stanley, which warns that the 2026 budget’s changes to negative gearing and capital gains tax (CGT) could trigger a 10% decline in home values, which would be the sharpest decline in at least 40 years.

Morgan Stanley says the budget’s removal of negative gearing for established homes and tougher CGT rules will slash investor returns.

Investors in established housing make up one‑third of marginal demand, so the impact is large.

“Proposed tax changes to capital gains and negative gearing announced in the federal budget last week fundamentally change the asset allocation decision for Australian households”, Morgan Stanley chief economist Chris Read said.

“This is particularly the case for housing: the previous model of high leverage, cash flow losses, and large expected capital gains is meaningfully challenged”.

Morgan Stanley estimates house prices may need to fall 15–20% to fully restore investor economics, but expect a national decline of up to 10% in practice.

“We estimate that a 15-20% decline would be required to fully restore investor economics”, Morgan Stanley said.

“A sharp decline in investor demand will be offset in part by owner-occupiers and new build investors, but this adjustment will take time and lower prices”.

Investors will demand higher rental yields, but Morgan Stanley argues rents cannot rise fast enough to compensate, so prices will fall instead.

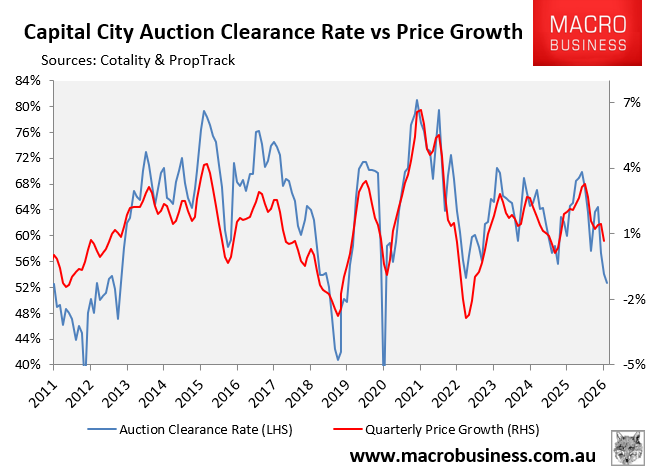

Morgan Stanley argues that market signals are already weakening. Auction clearance rates have dropped to multi‑year lows, especially in Sydney and Melbourne.

Morgan Stanley notes price growth has “peaked” and high‑value suburbs are already sliding.

A weaker housing market is expected to slow the broader economy in late 2026. The RBA may interpret the slowdown as evidence that policy is restrictive enough and hold rates steady for the rest of 2026. Consumer spending and the labour market may soften.

“A weaker housing market will drive a broader economic slowdown, with policy implications”, it concluded.

“We see the RBA able to stay on hold for the rest of 2026”.

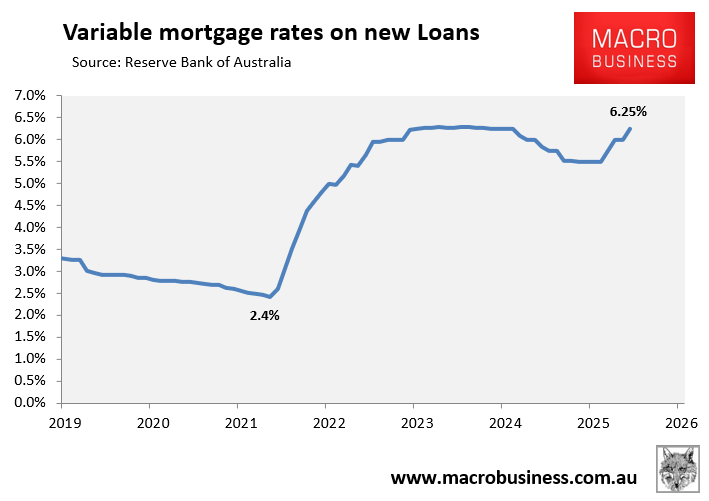

The headwinds facing the housing market are immense. Variable mortgage rates on new loans are now tracking at their highest level in around 15 years:

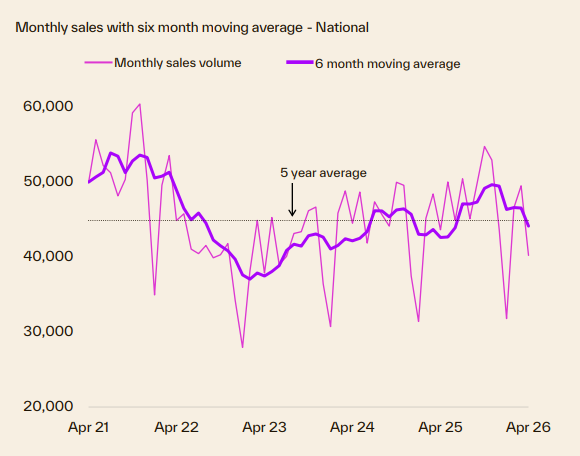

Buyer demand has also tanked, as illustrated by the collapse in auction clearance rates and the sharp fall in sales volumes.

Source: Cotality

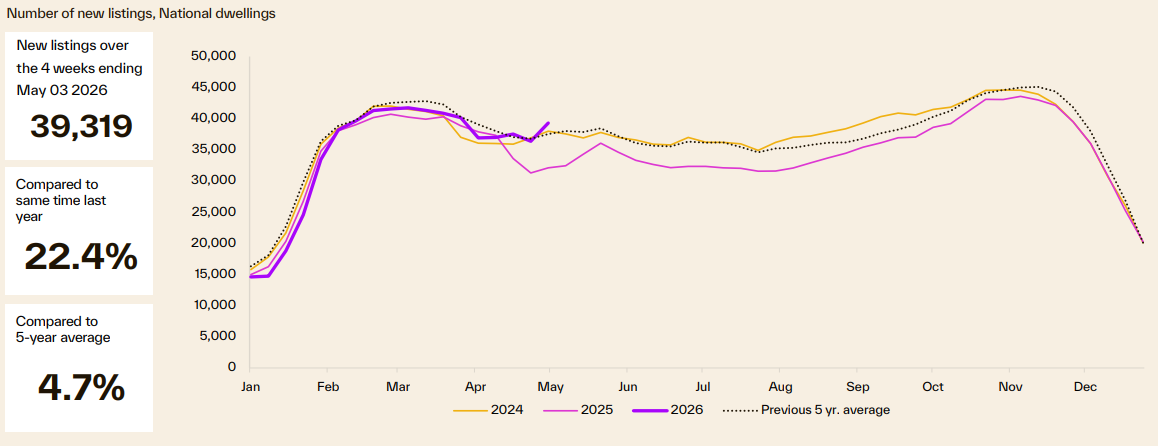

Meanwhile, the volume of new listings has shot up 22.4% over the past year to be tracking 4.7% above the five-year average:

Source: Cotality

The national unemployment rate has also risen to its highest level since November 2021 and will likely worsen amid the RBA’s monetary tightening, softer job growth in the non-market sector (as governments tighten spending) and the fallout from the global energy shock.

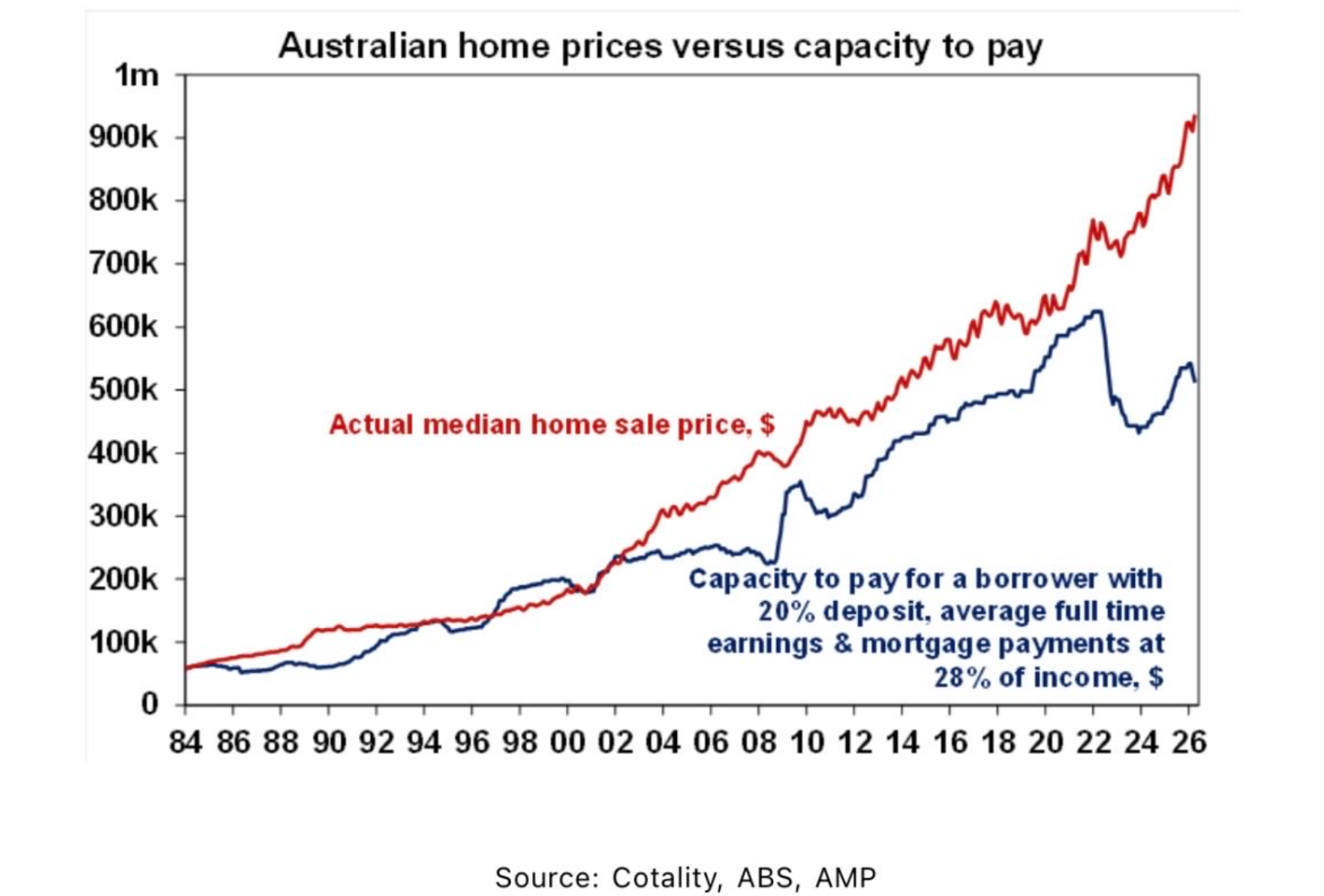

Ultimately, the dilemma facing home prices is summarised by the following chart from Shane Oliver at AMP:

Australian home values have grown to a level that is beyond what buyers can afford at prevailing interest rates.

Therefore, as interest rates rise further, home prices nationally will fall.

The jaws must close with the red line falling towards the blue line.