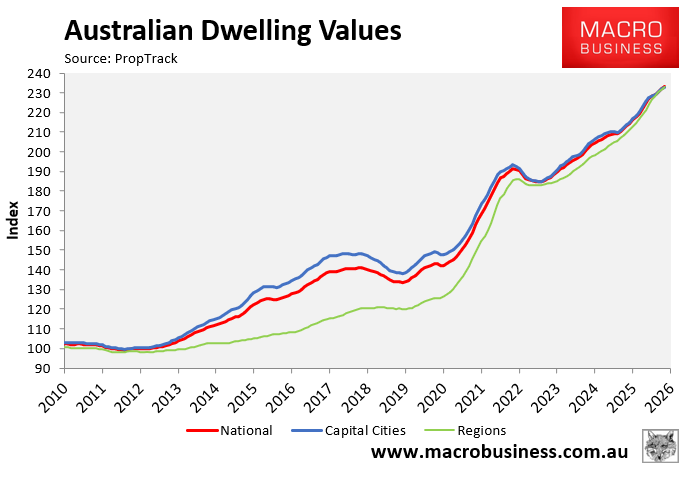

Home prices in Australia have never been this high.

The latest home price data from PropTrack shows that at the end of March 2026, the nation’s median home price had risen by 63% since the beginning of the COVID-19 pandemic in March 2020.

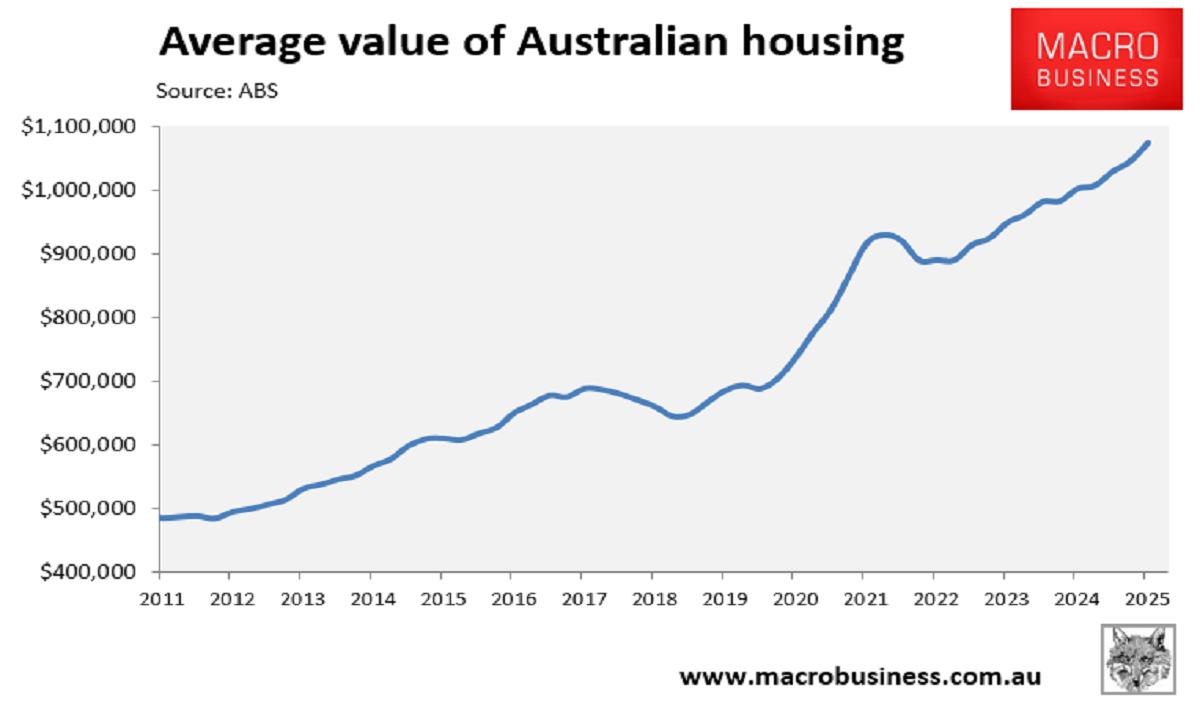

The Australian Bureau of Statistics (ABS) also valued the average dwelling at a record $1,074,000 as of the December quarter of 2025, up from $687,000 as of the December quarter of 2019.

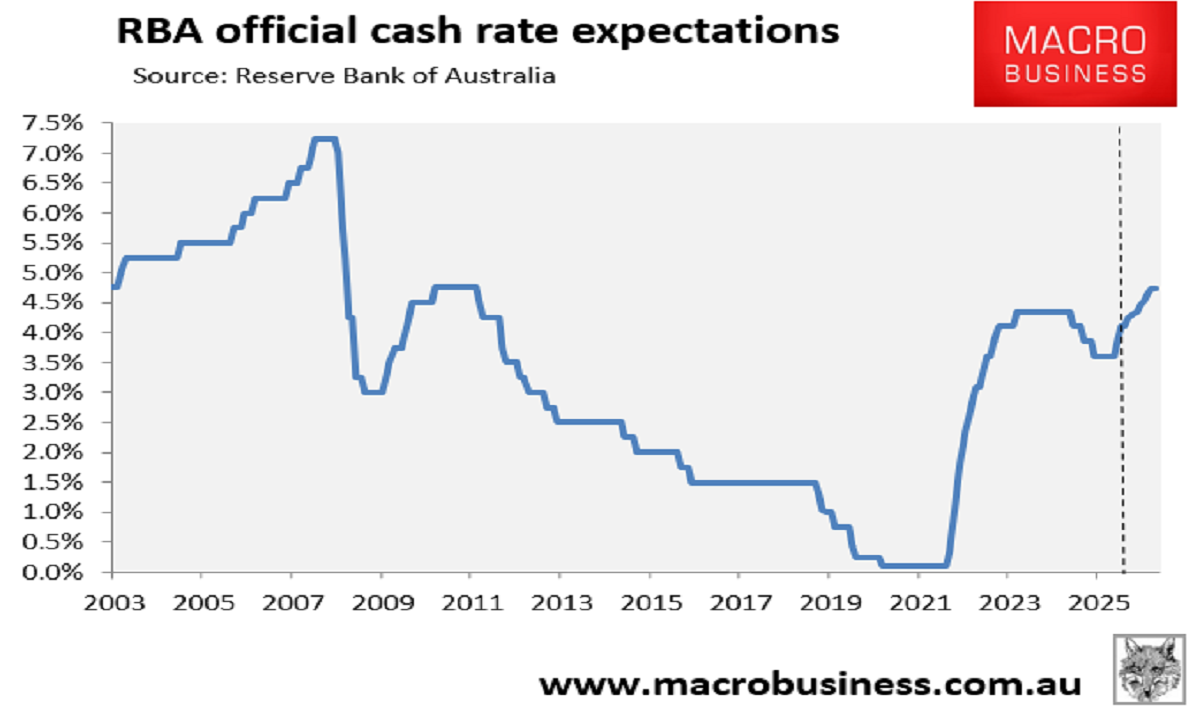

The post-pandemic surge in Australian dwelling values has occurred despite a sharp rise in interest rates, which has reduced borrowing capacity and increased mortgage repayments.

The official cash rate in Australia soared from a pandemic low of only 0.1% to a record 4.25% in May 2022 before retracing to 3.85%. The Reserve Bank of Australia (RBA) has since delivered back-to-back 25 bp hikes in February and March, and financial markets are tipping the cash rate to climb to an 18-year high of 4.85% by year’s end.

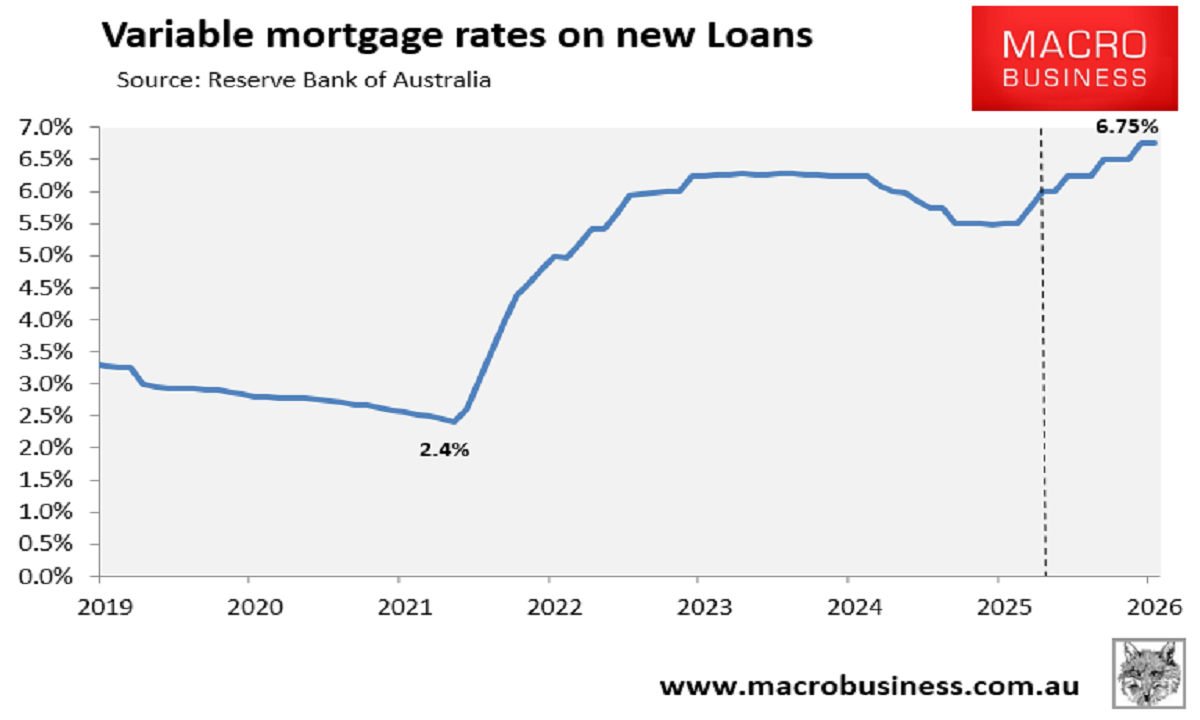

Mortgage rates have followed a similar path. The average discount variable mortgage rate soared from a low of 2.4% in April 2022 to a peak of 6.25% between November 2023 and January 2025 before falling to 5.5% following last year’s three 0.25% rate cuts from the RBA.

The average discount variable mortgage rate has since increased to 6.0% and will end the year at 6.75% if the RBA delivers three additional rate hikes:

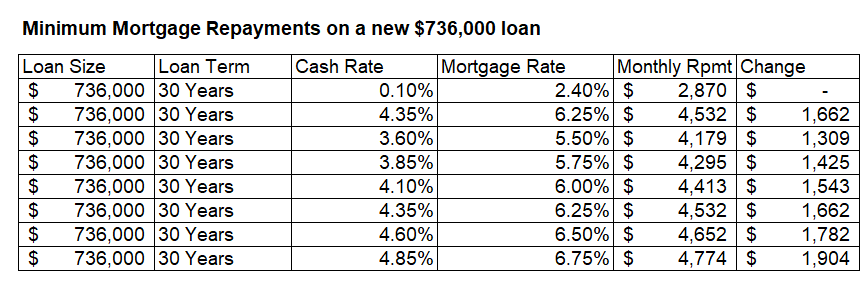

The table below shows the effects of the recent increase in mortgage rates, with an average new loan size of $736,000.

Monthly payments were as low as $2,870 when variable mortgage rates hit 2.4%.

The minimum monthly repayment on a $736,000 loan was $4,532 during the peak period of November 2023 to January 2025, an increase of $1,662, or 58%, when the average variable mortgage rate on new loans reached 6.25%.

The minimum monthly repayment on a $736,000 loan was $4,179 when mortgage rates dropped to 5.5% following RBA rate cuts last year. The figure was still $1309, or 46%, higher than the pandemic low.

If mortgage rates rise to 6.75%, as projected, monthly repayments will rise to $4,774 on an average-sized new loan, $1,904 (66%) higher than the pandemic low.

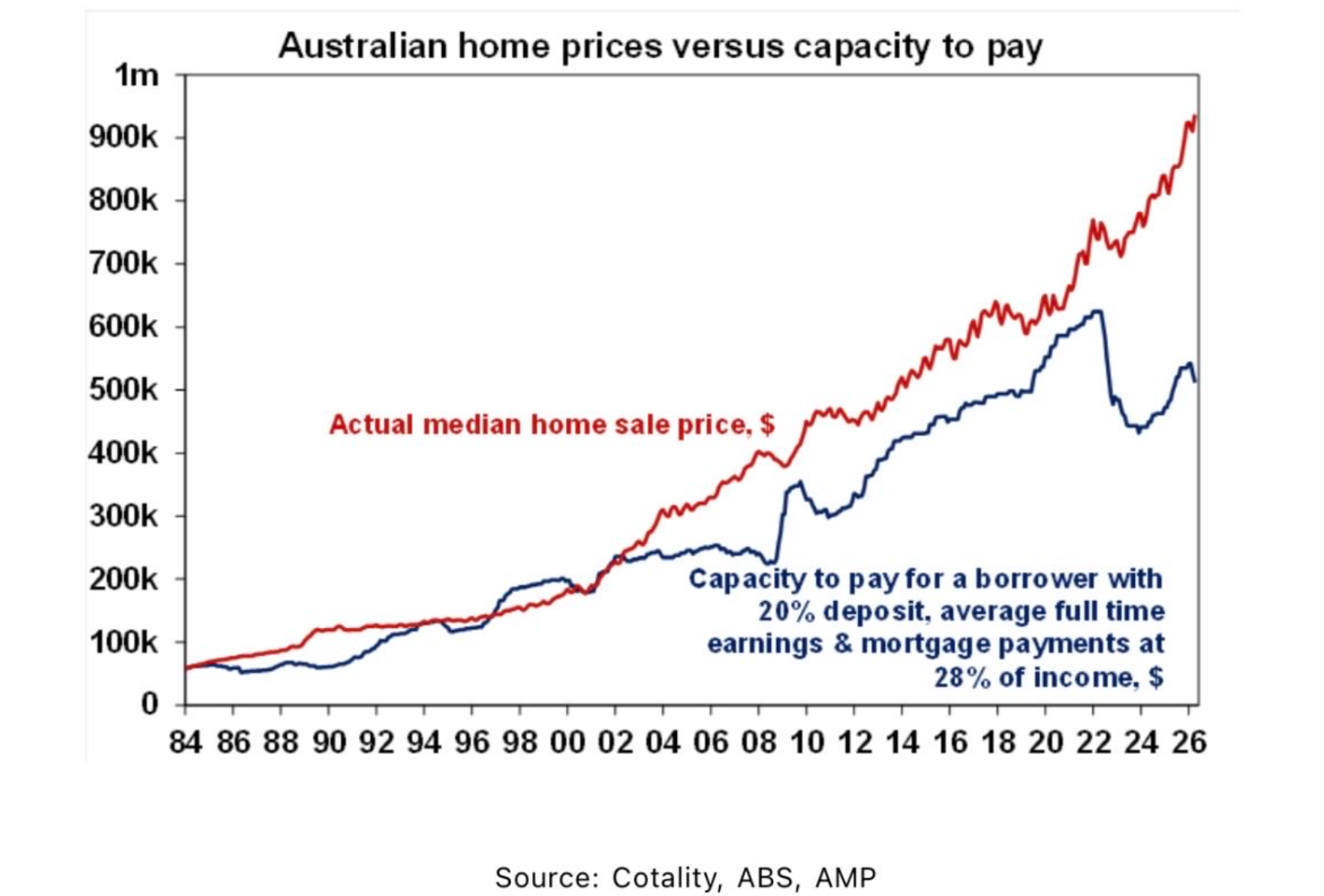

Australian home prices should have fallen due to the sharp increase in mortgage payments and the circa 30% decrease in borrowing capacity.

For most of the past 30 years, Australian home prices tracked borrowing capacity because buyers bid up to the maximum the bank would lend.

When rates fall, borrowing power rises and prices generally rise; when rates rise, borrowing power falls and prices generally soften.

The following chart from Shane Oliver at AMP shows how the relationship has broken down and a record gap has developed between borrowing capacity and home prices. This gap is beginning to widen again as home prices rise alongside mortgage rates:

Several factors explain the decoupling of home prices from borrowing capacity.

First, the “Bank of Mum and Dad” is now a major and expanding player in the housing market. Contributing an estimated $35 billion to $92 billion in loans annually, it is considered the nation’s fifth-largest mortgage provider, assisting first home buyers in purchasing property.

Two out of five first-time homebuyers are now using the Bank of Mum and Dad, according to Hillhouse Legal Partners. This is because parents can avoid borrowing limits by funding deposits with their own money.

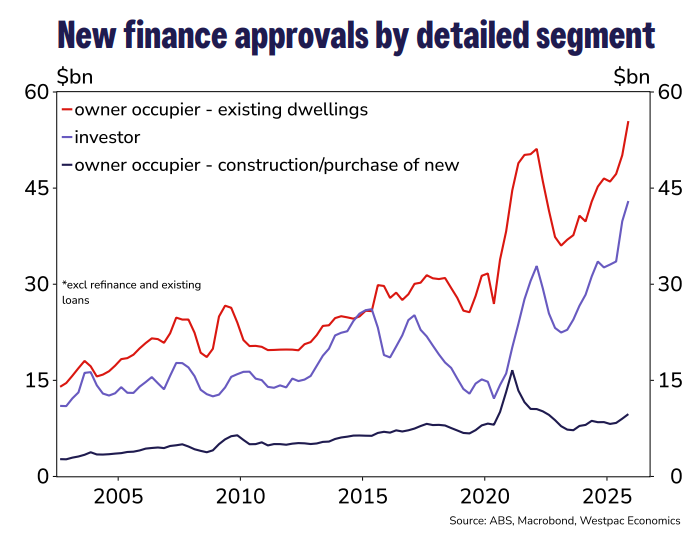

Secondly, the proportion of market participants who are investors has grown substantially, as shown below.

Traditional borrowing constraints are less of an issue for investors because they typically borrow against existing home equity.

Finally, government incentives such as shared equity schemes, homebuyer grants, and 5% deposit schemes mitigate the effect of borrowing limits.

As a result, there has been a decoupling of Australian housing values from borrowing ability.

With mortgage rates set to rise further, borrowing capacity will become even more out of kilter with prices, making current valuations even less sustainable.

Ultimately, home prices must fall to bring them more in line with borrowing capacity.

Only then will Australian housing values make sense.