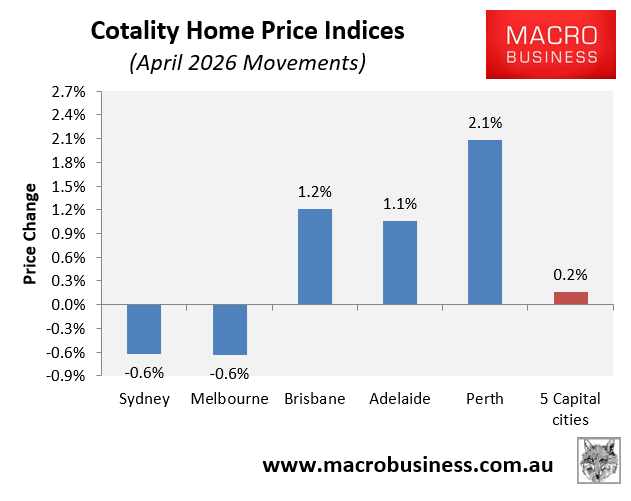

Cotality’s daily dwelling values index for 30 April shows that home values across the five major capital city markets rose by only 0.2% over the month, with sharp falls of 0.6% in Sydney and Melbourne offsetting still strong growth in Perth (2.1%), Brisbane (1.2%), and Adelaide (1.1%).

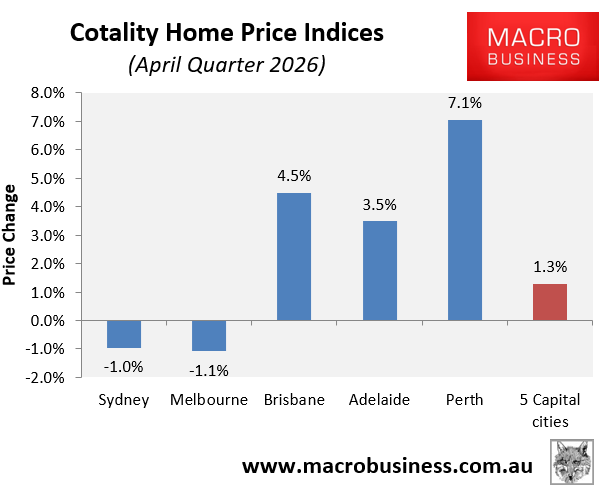

Over the April quarter, home values rose by 1.3%. However, it was a two-speed market, with value declines of 1.0% in Sydney and 1.1% in Melbourne partly offsetting strong value gains in Perth (7.1%), Brisbane (4.5%), and Adelaide (3.5%).

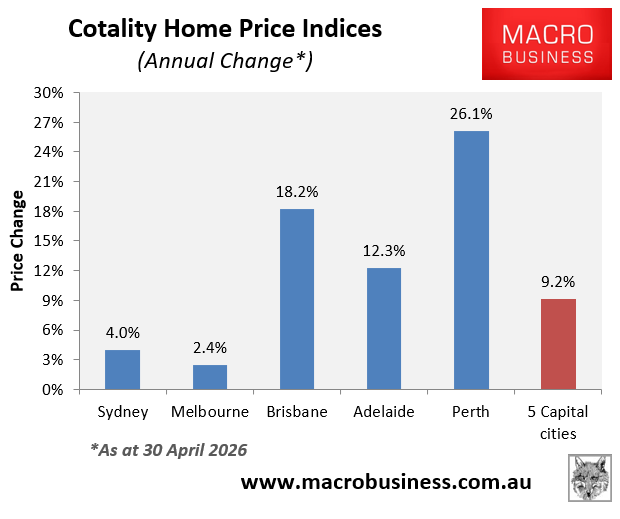

Over the year to 30 April 2026, all major capital city markets recorded value gains. However, growth was modest in Sydney (4.0%) and Melbourne (2.4%), strong in Brisbane (18.2%) and Adelaide (12.3%), and exceptionally strong in Perth (26.1%).

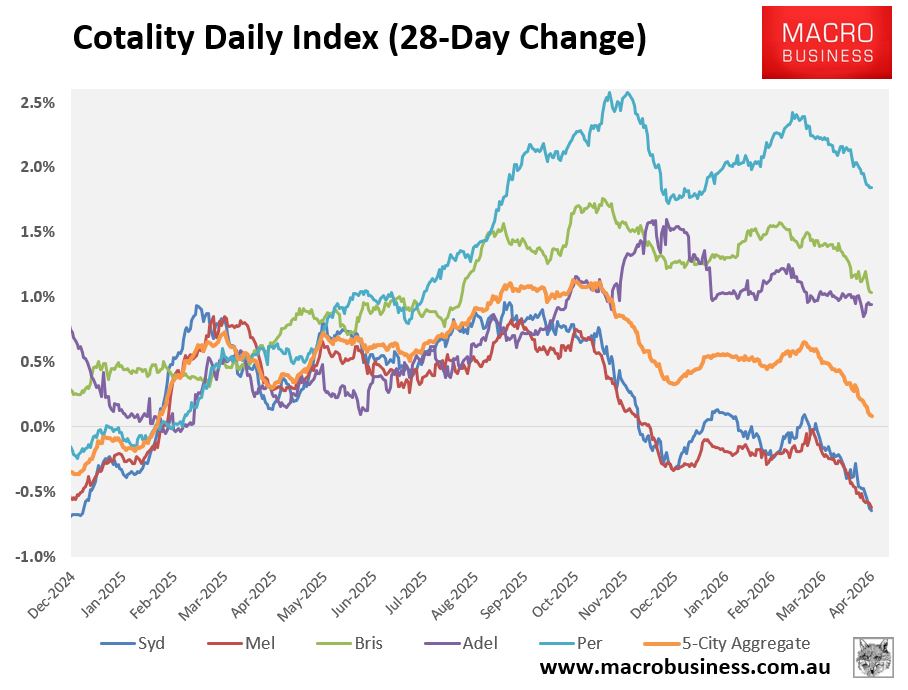

The following chart plots dwelling value growth on a rolling 28-day basis across the major capital cities.

As you can see, price falls are accelerating in Sydney and Melbourne, which is pulling down the five-city aggregate. By contrast, growth remains strong in the other major markets, albeit momentum is slowing.

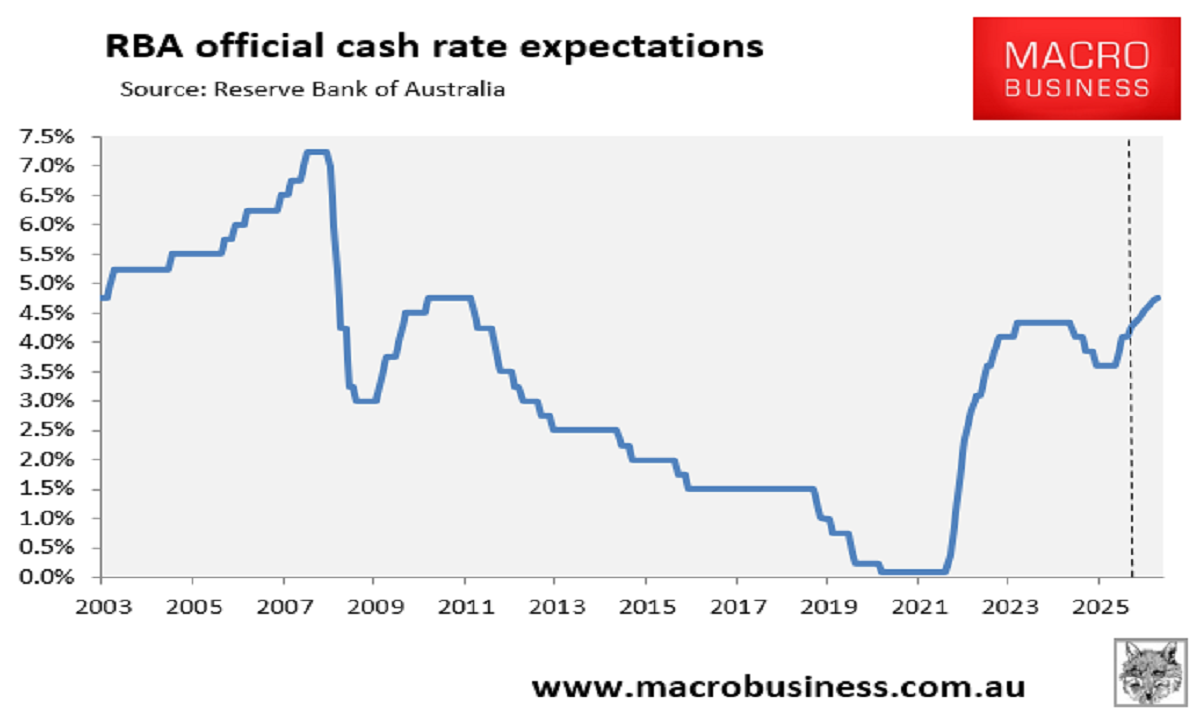

With inflation embedded amid rising energy costs and financial markets tipping at least another two and possibly three interest rate hikes this year, Australian home values are certain to lose momentum.

Sydney and Melbourne are facing significant falls in home values in 2026, which will pull national values into negative territory, while growth will likely decelerate sharply in the other major markets, with some posting outright monthly declines by year’s end.

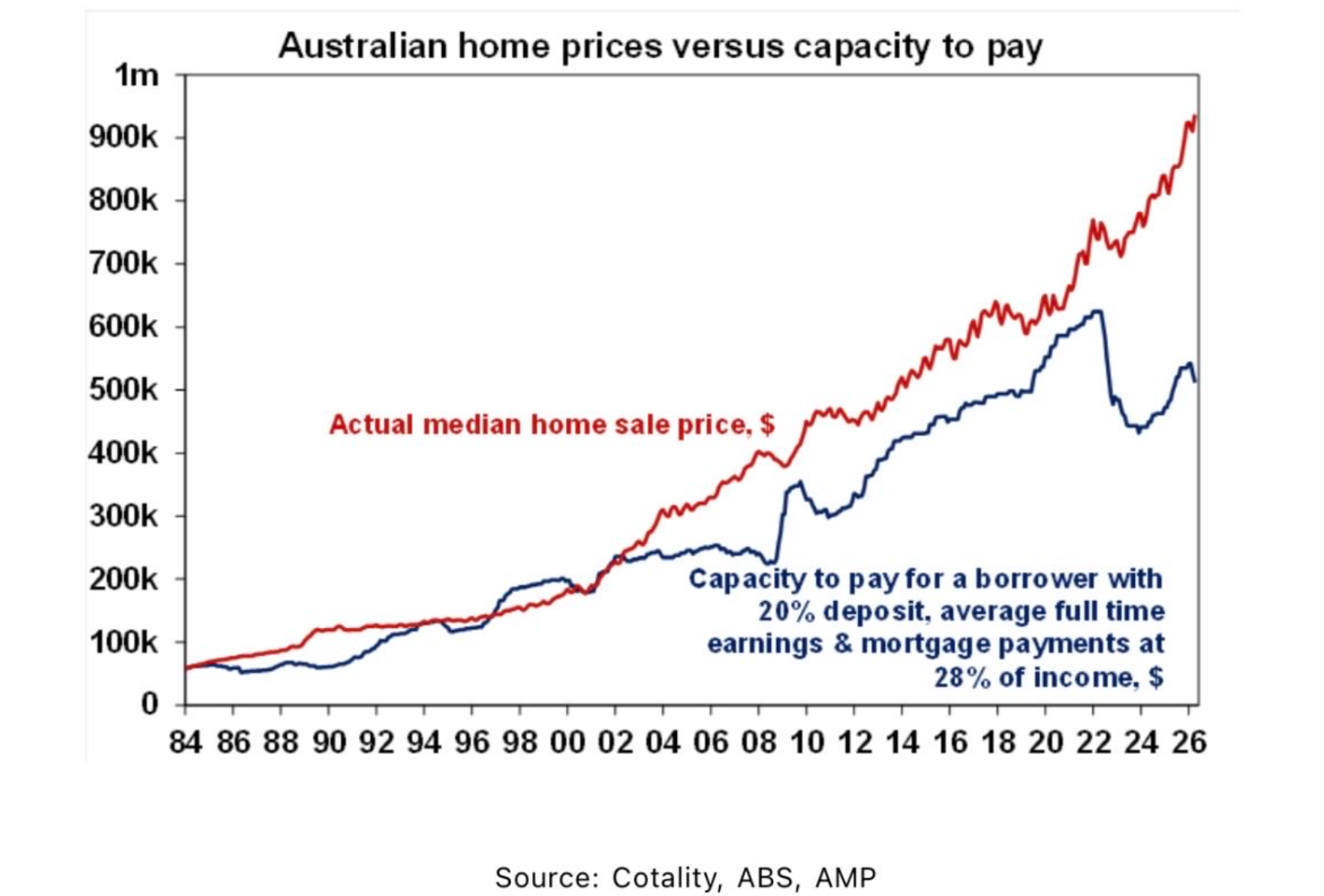

Ultimately, the problem facing Australia’s housing market relates to overvaluation, as illustrated in the following chart from AMP chief economist Shane Oliver.

Put simply, Australian home values have grown beyond what buyers can afford at prevailing interest rates.

Therefore, as interest rates rise further, home prices nationally should fall.