Expensive homes and mega-mortgages risk blowing up retirement system

Australia’s retirement system has been based on the presumption that the overwhelming majority of people would own their homes outright upon retirement.

However, due to declining homeownership rates, Australians buying homes later, and carrying larger mortgages into retirement, that assumption is clearly crumbling.

Westpac notes that people over the age of 40 accounted for around 20% of mortgage loans issued to first-home buyers in 2025.

As a result of people purchasing later and taking out larger mortgages, Loan Market Group has found that 40% of respondents do not expect to have paid off their mortgages by the time they retire.

This analysis aligns with warnings from the Super Members Council of Australia, which estimated that more than 40% of Australians will retire with mortgage debt, up from 16% two decades ago.

To exacerbate the situation, 40% of individuals and 33% of couples will utilise their entire superannuation savings to pay off their debts.

Credit bureau Equifax also suggested that the number of enquiries from Australians aged 55+ about refinancing their mortgage rose by 12% year-on-year in February, while enquiries from the 46-55 age group grew by 8%.

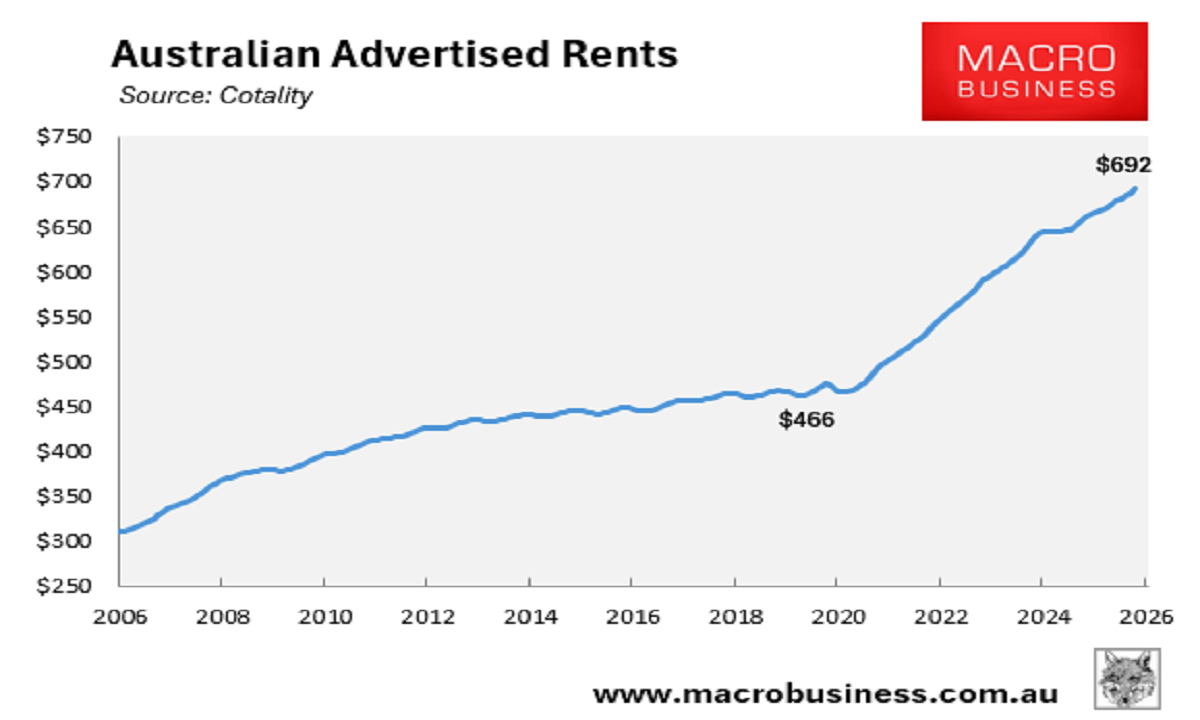

Then there is the problem of surging rents, which have jumped by around 48% since the end of 2019, far outpacing wages and superannuation growth.

Cotality estimates that the median tenant household today needs to spend around $11,700 more annually to rent the median advertised home than they did at the end of 2019.

As a result, research by Super Consumers Australia has found that the typical single renter retiree needs $659,000 in superannuation to enjoy a financially secure future, more than twice the $322,000 required by a homeowner.

Couples face a similar gap: $786,000 for renters versus $432,000 for homeowners.

Renters are three times more likely to struggle financially in retirement. Only 10% of retired homeowners are in financial stress. By comparison, nearly 50% of retired renters face financial stress.

The above data suggest that Australia’s housing crisis poses a direct threat to the nation’s retirement system.

A growing proportion of Australian retirees will rent in the future, while others will shoulder larger mortgage debts.

Both situations will reduce the amount of disposable income available in retirement.