The ongoing conflicts in Ukraine and the Middle East are doing more than reshaping geopolitics—they are forcing nations to rapidly accelerate their move away from fossil fuels in the name of energy security.

But when it comes to the energy transition, the debate is often muddied by disingenuous arguments, linear thinking, and theoretical solutions. As investors, we need to cut through the noise and look at the reality of the grid today and where the capital is actually flowing.

Here is what you need to know about the economics of the energy transition.

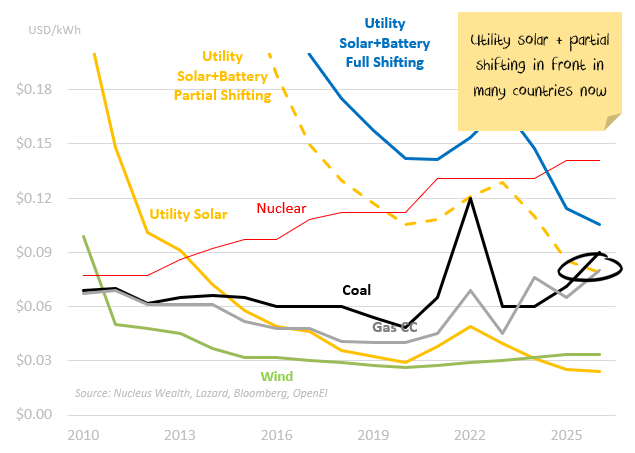

1. Cost of generation

Coal, gas, oil. All have an economic basis in a scarcity curve: the more we use, the deeper we need to dig and the more expensive it becomes to extract. Solar and battery power are on a technology curve. The more the world produces, the cheaper it becomes:

Keep in mind these are averages – different fuel prices, different latitudes generate different outcomes.

This leaves us with energy parity, where the technology curve serves as an upper bound for the scarcity curve. i.e. the price of energy will trend towards the cost of Solar+Batteries.

Solar+Batteries are the “killer app” – extremely scalable once they reach an acceptable cost. We are getting really close.

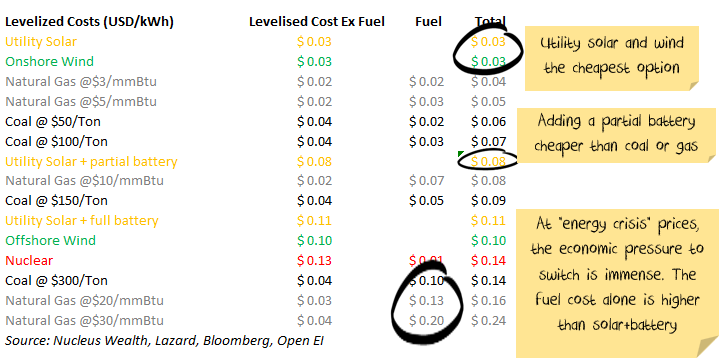

The issue is that gas-fired electricity is extremely sensitive to fuel cost. Even more so than other technologies. Currently, at elevated gas and coal prices, renewables + batteries are cheaper.

Note that at $20/mmBtu gas prices or $300 coal prices, it becomes more economical to shut down power plants in favour of new solar or wind + batteries.

2. Transmission and Distribution Matter

Electricity isn’t just about generation. It is about moving power from where it is created to where it is consumed.

I frequently see disingenuous cost comparisons: comparing the pure “generation cost” of one method against the “generation plus transmission cost” of another. Or pretending we need to replace a 50-year-old coal-fired power plant, but the 50-year-old transmission lines will be fine.

Depending on the region, transmission and distribution account for roughly 40% of the total cost of electricity. The reality today is simple:

- The cheapest generation is the one already built.

- The cheapest form of new generation is the one that does not require you to build new transmission lines to support it.

3. Supply matters

Ukraine/Russia and Iran have inserted a corollary. It doesn’t matter how cheap your energy is if the supply can be disrupted. This might mean China builds more coal-fired plants than it would have in a world without wars. But this is probably of less benefit to major coal exporters (like Australia) than you might think. China has a lot of coal, not much oil or gas. It is not looking to substitute Middle Eastern dependence for Australian dependence.

Another plus for solar + batteries. Distributed power has a defence imperative.

4. Is wind running out of puff?

The long, impressive decline in the cost of wind energy is likely behind us. While “like-for-like” costs will probably continue to decline, building in more difficult geographic locations will likely limit the average generating cost.

This isn’t to say wind is dead. Well-situated wind projects with minimal transmission requirements remain incredibly attractive investments.

The issue is scalability. The prime locations—the low-hanging fruit with high, consistent yields and easy grid connections—are already largely developed.

Exponential growth in solar + batteries seems far more likely than exponential growth in wind.

5. Nuclear Dreams

The best argument for nuclear power is to increase supply diversity. But the economic argument is lacking.

Nuclear is safe and reliable, but it’s crippled by compliance costs. In developed nations, regulation is so strict that every plant is a “first-of-its-kind” project.

Proponents point to Small Modular Reactors (SMRs) as the silver bullet for these regulatory and cost hurdles. But I want to see at least one working model. Nuclear has a 70-year opportunity to create cost-effective small modular reactors. How many more years do they need?

Currently, small modular reactors feel like the carbon capture and storage argument: here is a technology that will potentially solve everything – a great excuse to do nothing about fossil fuels.

Small Modular Reactors also face a Scaling Deficit. Think of it like this:

- Solar/Batteries: We add “zeros” to production constantly. We went from 1 to 10 to 1,000 to 10,000. Then through a bunch more steps to 10 million units. Every time we double production, costs drop by ~20% (Wright’s Law).

- SMRs: We might go from 1 to 10 to maybe 100 units. The world doesn’t need tens of thousands of SMRs. You simply cannot get the same “learning rate” from 100 reactors per year that you get from 10 million solar panels per year.

6. The Solar and Battery Maths

There is a legitimate cost to the intermittency of renewables, particularly solar.

In a large grid where solar accounts for a small fraction of the energy mix, integration costs are negligible. But as solar becomes the dominant source of power, the cost grows exponentially.

Critics love to point out that the sun doesn’t shine at night. They’re right: as solar grows, the “cost of intermittency” grows exponentially.

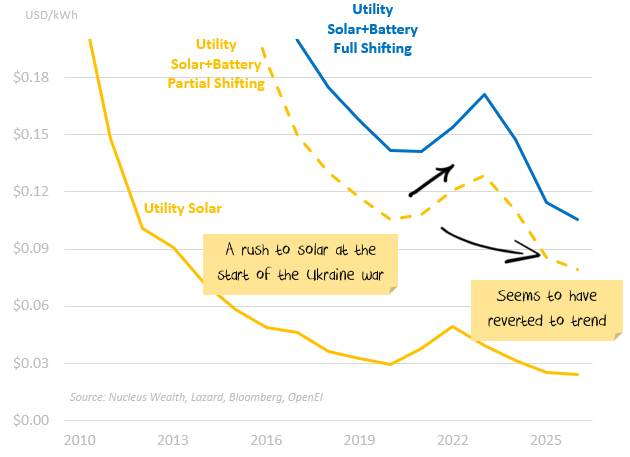

But critics missed the part where batteries entered their own “Experience Curve.” Combined with the rising costs of coal and gas—pushed to record highs by the ongoing regional instabilities—Solar + Partial Storage is now officially cheaper than “firm” fossil fuels.

We are no longer waiting for a miracle; we are just waiting for the next shipment of batteries.

Following the Ukraine war, solar prices jumped as Europe scrambled for more capacity. That might happen again. But, costs are coming down, and the relentless march lower seems to have reasserted itself:

7. People Are Bad at Non-Linear Maths

The energy transition is not a linear process, and human brains are notoriously bad at grasping non-linear relationships.

With traditional infrastructure like coal or gas, you build a power plant in one year, and then you start from scratch to build the next one.

With solar and batteries, the factories are the 2nd derivative. Expanding the factories that produce solar panels accelerates the move away from fossil fuels. We have already seen extraordinary increases in global solar panel manufacturing capacity—so much so that installation and transmission simply cannot keep up with the supply.

To put this in perspective: the world now has the manufacturing capacity to produce enough solar panels in a single year to generate roughly 5% of total global electricity demand.

Even if this factory capacity barely grows from here, the sheer volume of new generation rolling off the lines means the acceleration is already baked in and compounding.

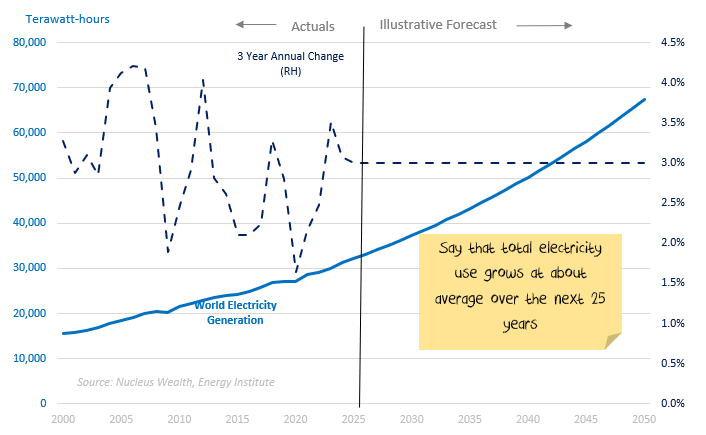

To illustrate, consider a world of 3% electricity growth, supported by a switch to EVs and data centres, constrained by lower population growth:

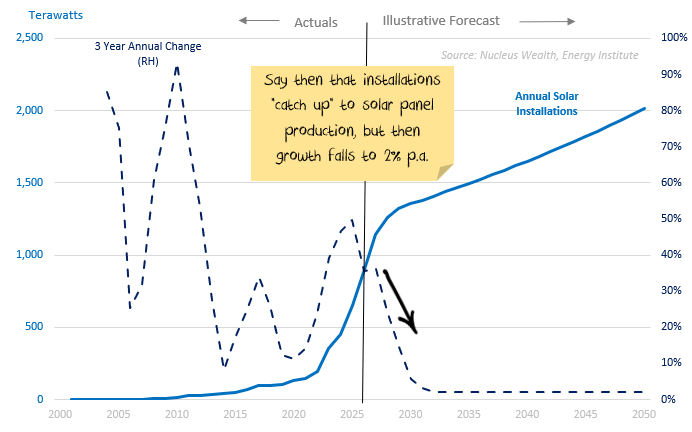

Right now, the bottleneck is not solar panel production, but rather the installation and permitting. Let’s say installation catches up to production, and then promptly falls to a 2% growth rate:

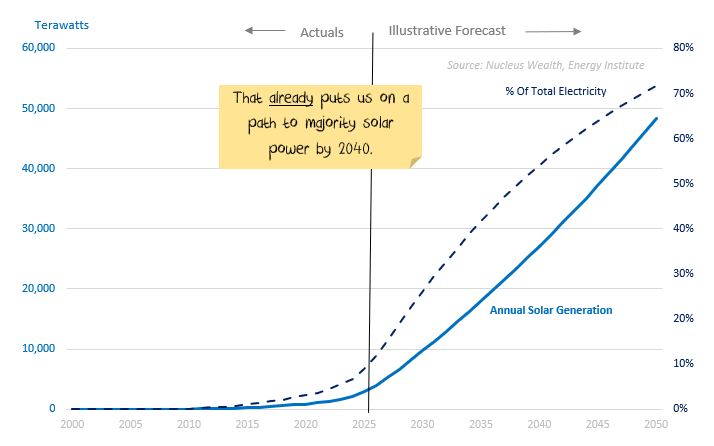

Under that scenario, we are already on a path to majority solar power by 2040:

The upshot: the extreme growth in solar panel production has already occurred. Now we are waiting for installation and batteries.

8. How to Invest in the Transition

So, what does this mean for your portfolio?

Approach manufacturers with caution: The solar panel and battery manufacturing sector is difficult. It is heavily government-sponsored and subsidised, meaning it will not operate as a true “free market” for decades. As an investor, your gains in this space will largely depend on whether your domestic government or the Chinese government is feeling more accommodating at any given moment.

Bet on the change: Stick with the service and infrastructure companies enabling the transition—the “picks and shovels” of the grid.

The fossil fuel endgame: Legacy fossil fuel companies are likely about to make super profits in the short term, driven by underinvestment and supply constraints. Take those profits if you hold them, but be warned: the end is coming much faster than linear forecasts suggest. There is a good short-term argument to use these stocks as a hedge for the Hormuz Strait being closed. But it is not a forever bet.

Damien Klassen is Chief Investment Officer at the Macrobusiness Fund, which is powered by Nucleus Wealth.

Follow @DamienKlassen on X(Twitter) or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an Authorised Representative of Nucleus Advice Pty Limited, Australian Financial Services Licensee 515796. And Nucleus Wealth is a Corporate Authorised Representative of Nucleus Advice Pty Ltd.