Australia’s federal budget uses two main deficit measures, and they differ because they treat certain transactions differently—especially asset sales, loans, and off‑budget funds.

The headline balance captures all cash flows in and out of the Commonwealth government, including:

- day‑to‑day spending

- tax revenue

- capital spending

- asset purchases and sales

- loans issued and repaid

- equity injections

- transactions with government investment funds (e.g., Future Fund, CEFC, NAIF).

The headline budget balance shows the total change in the government’s cash position and can be volatile due to large transactions (e.g., equity injections into off‑budget funds).

The underlying balance receives most of the attention and excludes many large, lumpy, or non‑recurring financial transactions, such as:

- Future Fund earnings

- student loan repayments

- equity injections

- loans to government businesses

- asset sales

- investments in off‑budget funds

- net Future Fund contributions.

The underlying balance is the difference between recurrent spending and recurrent revenue and is what most economists, the Treasury, the RBA, and ratings agencies focus on.

In short, the headline deficit counts everything, including loans and asset purchases, whereas the underlying deficit strips out those financial transactions to show the government’s real operating position.

The Problem:

The gap between the two measures has blown out because the federal government has increasingly pushed spending off the balance sheet via:

- off‑budget investment vehicles

- special funds

- equity injections

- government loans

As a result, the headline deficit has ballooned relative to the underlying deficit.

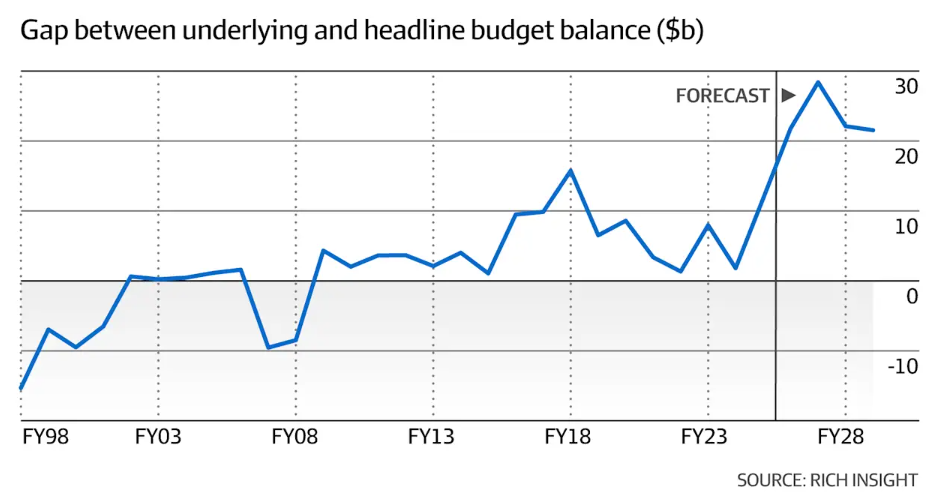

The following chart from veteran budget watcher economist Chris Richardson illustrates the situation:

“Over the next four years, the headline cash deficit is cumulatively forecast to be $237 billion”, The AFR’s John Kehoe wrote in relation to Richardson’s analysis.

“That’s $94 billion worse than the $143 billion cumulative underlying cash deficit that is the government’s preferred measure”.

“The off-budget lurk hides plenty of dollars”, Richardson says.

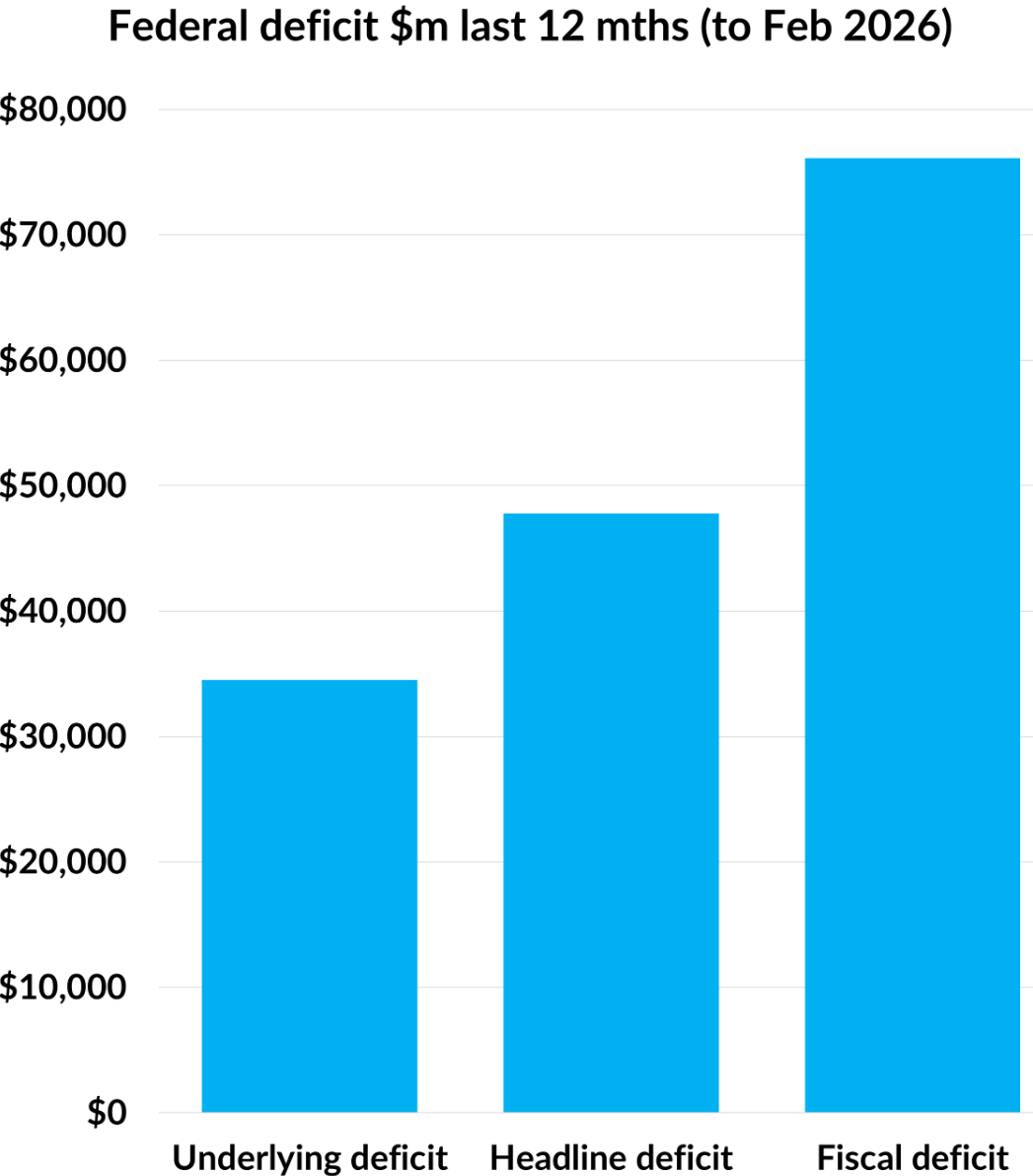

But it gets even worse, according to Richardson. There is a third budget measure called the fiscal deficit, which also picks up things like the forgiveness of student loans, which Richardson describes as “poor policy” because “it subsidises tertiary-educated individuals who typically earn higher lifetime incomes using taxpayer funds from those who may never have attended university”.

Source: Chris Richardson

As illustrated above, the fiscal deficit was $76 billion in the year to February 2026, more than double the $34 billion underlying deficit.

“In Canberra, what gets measured gets manipulated”, Richardson wrote on Twitter (X).

“Unless we fight for better budget reporting, we’ll keep getting treated as mugs”.

The Takeaway:

Tighter controls are required on government spending, and transparency is desperately needed regarding the various off-balance-sheet slush funds utilised by the government.

In addition to cutting wasteful and inefficient spending, the federal government should revisit the 2010 Henry Tax Review and initiate a fundamental tax reform process.

We must broaden the tax base beyond personal income and corporate taxes by expanding taxes on consumption, resources, and land.

Otherwise, Australia’s shrinking pool of workers will be taxed into oblivion.