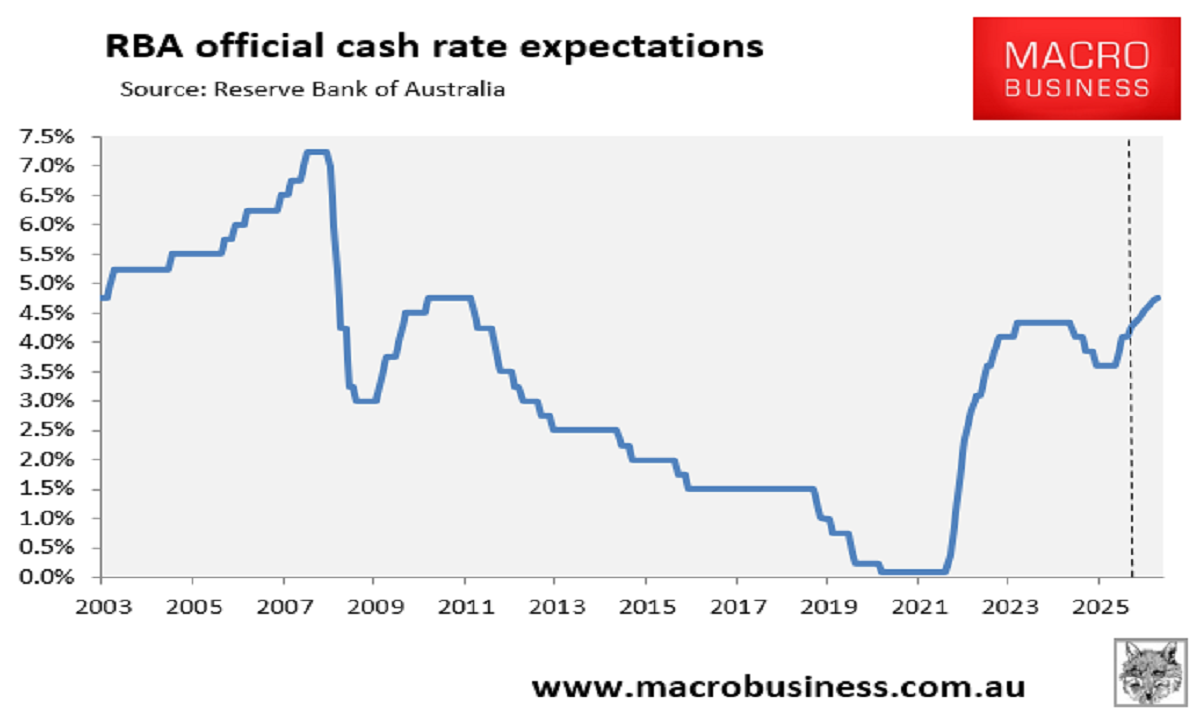

The interest rate futures market has priced an official cash rate of 4.75% by the end of 2026.

This implies that the Reserve Bank of Australia (RBA) will deliver at least two, and possibly three, more interest rate hikes this calendar year.

If the RBA delivered two more rate hikes, the official cash rate would end the year at 4.60% – the highest level in 15 years. If the RBA delivered three hikes, it would end 2026 with a cash rate of 4.85%, the highest level in 18 years.

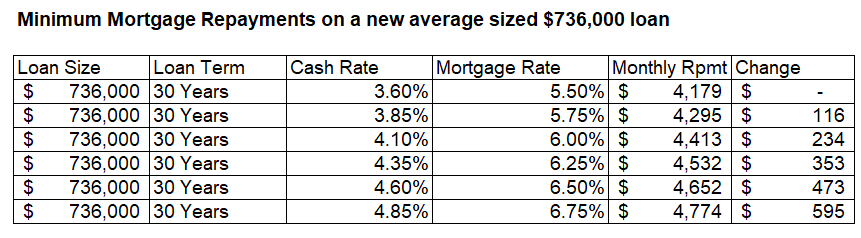

The impact of such rate rises on the average new mortgage holder is illustrated in the table below, which compares monthly mortgage repayments against those at the beginning of the year, before the RBA commenced its hiking cycle.

As you can see, average mortgage repayments on a typical $736,000 new mortgage would be $473 a month higher if the cash rate hit 4.60%, and $595 a month higher if it ended the year at 4.85%.

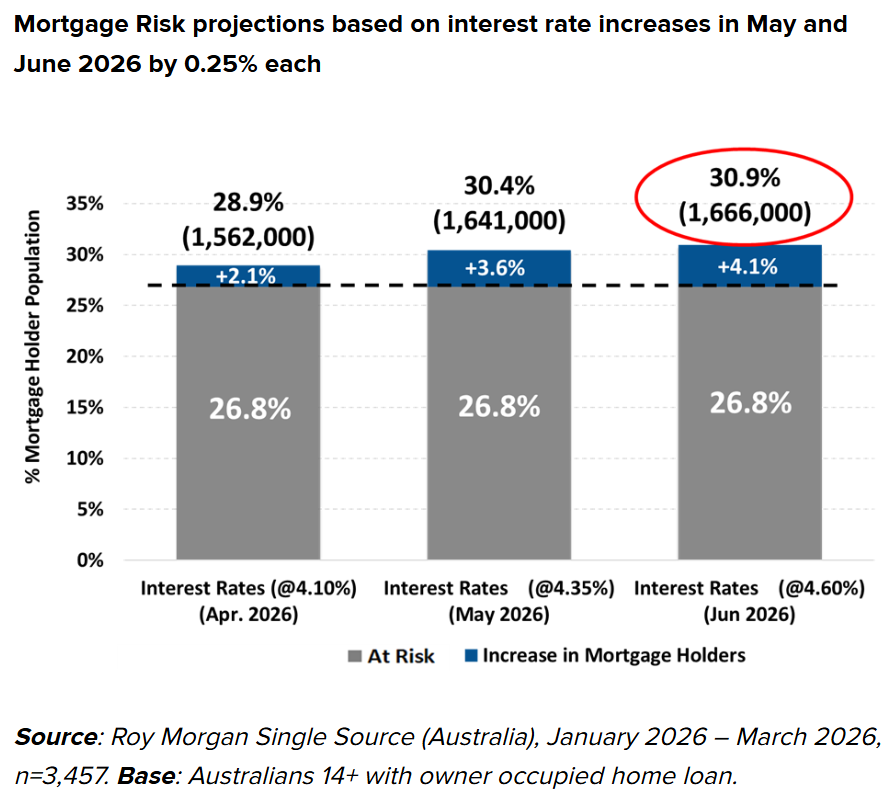

According to analysis from Roy Morgan, 30.9% of mortgage holders would be “at risk” of stress if the RBA were to lift the official cash rate twice more to 4.60%:

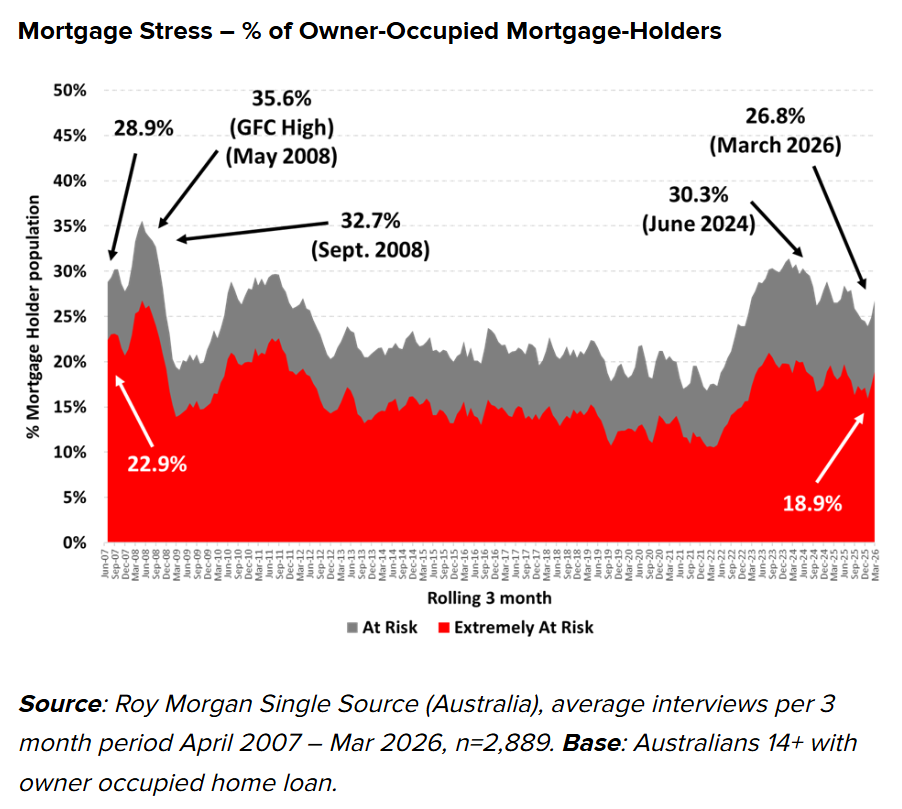

This would represent the highest rate of mortgage stress since the Global Financial Crisis in mid-2008, when the official cash rate hit 7.25%:

Roy Morgan CEO Michele Levine warned that the biggest risk to mortgage holders isn’t rising interest rates but unemployment.

“The fact remains the greatest impact on an individual, or a household’s, ability to pay the mortgage is not interest rates, it’s if they lose their job or main source of income”.

While the current unemployment rate of 4.3% remains historically low, risks are building.

In addition to rising inflation and interest rates, the prospect of diesel fuel shortages could literally shut down parts of the economy, resulting in recession and higher unemployment.

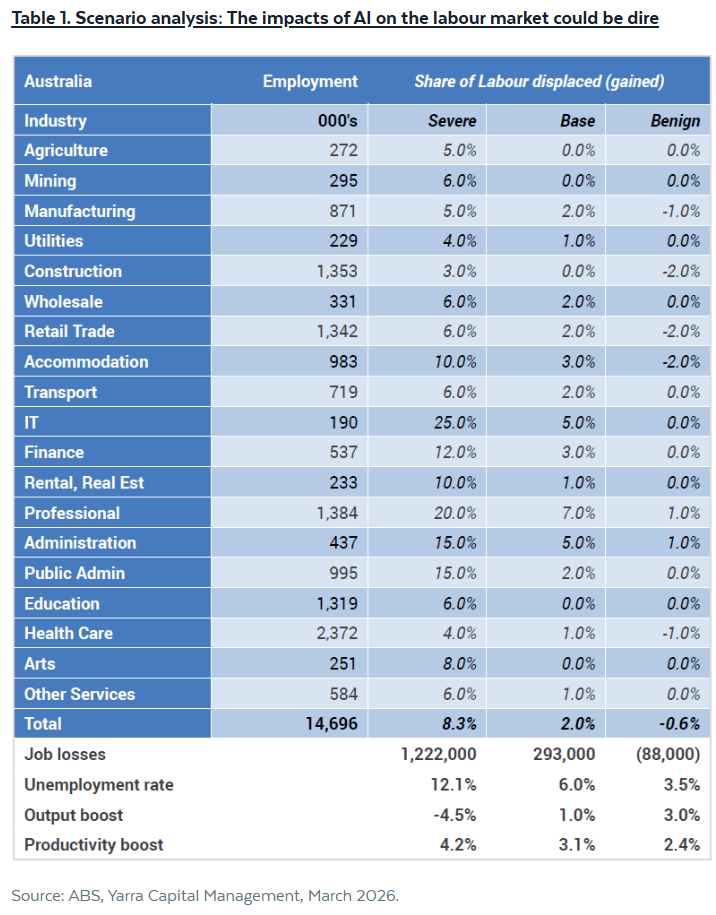

Tim Toohey from Yarra Capital also warned that if AI is “deployed at scale in Australia over the next two years”, then the nation’s unemployment rate could rise to 6% or higher:

Recent first-home buyers who leveraged the expanded 5% deposit scheme to purchase in Sydney and Melbourne should feel particularly vulnerable, given that home prices in these two markets are now falling sharply.

Recent first home buyers in these markets face the prospect of falling into negative equity.