The Great Australian house price boom is losing momentum fast.

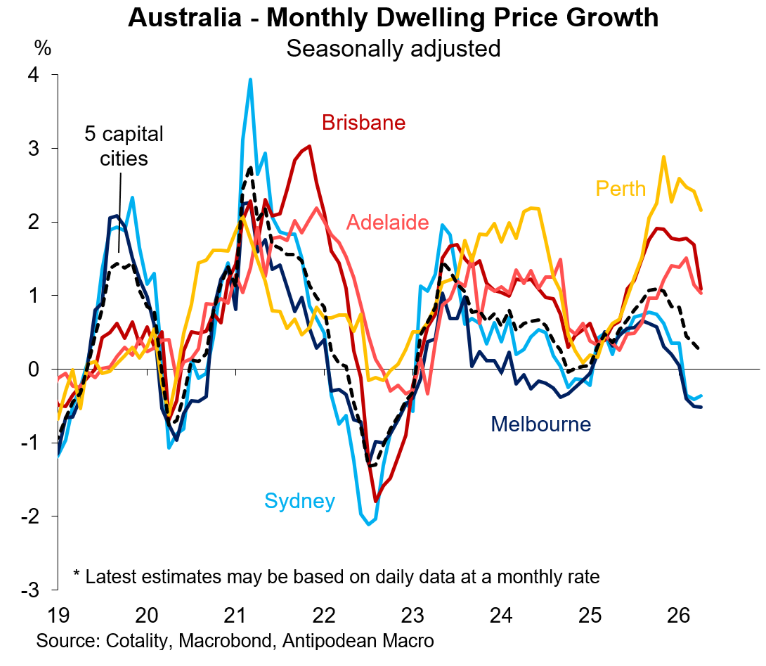

As illustrated below by Justin Fabo from Antipodean Macro, monthly dwelling value growth across the five major capital cities has fallen sharply so far in April, with all major markets losing momentum or, in the case of Sydney and Melbourne, recording outright price falls.

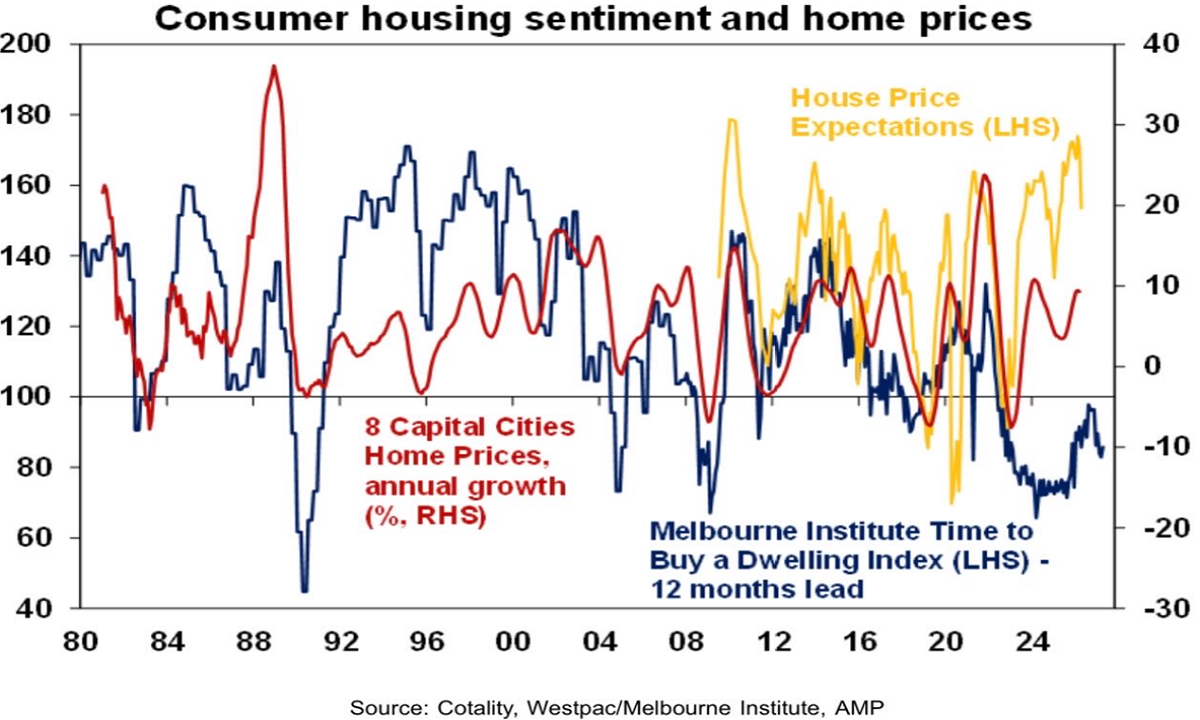

The loss of momentum was foreshadowed by the latest Westpac Melbourne Institute consumer sentiment survey, released last week, which showed that house price expectations fell by 10.2% in April, albeit it remained fairly bullish overall.

Chart by Shane Oliver (AMP)

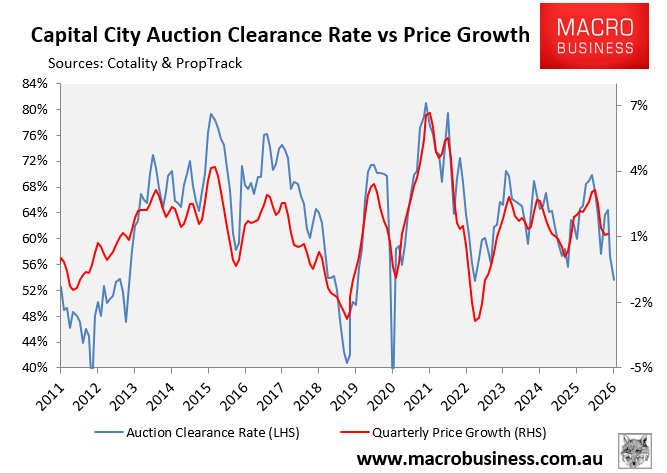

Auction clearance rates have also fallen sharply over recent months, which typically correlates strongly with home price growth:

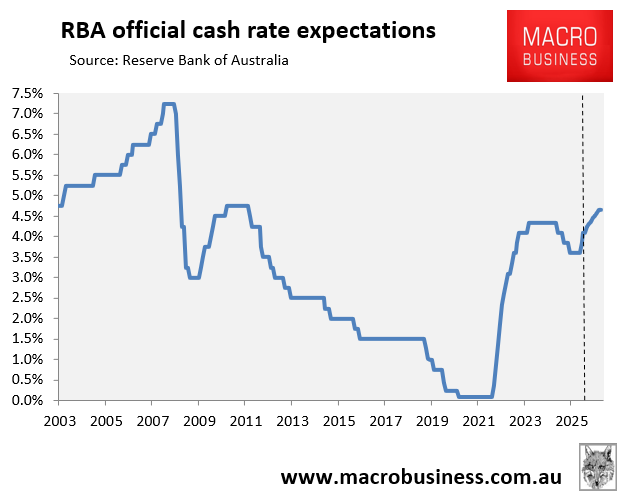

The negative outlook is understandable. The Reserve Bank of Australia (RBA) has delivered back-to-back interest rate hikes, and financial markets expect at least another two 25 bp rate hikes this year, which would push the official cash rate to a 15-year high:

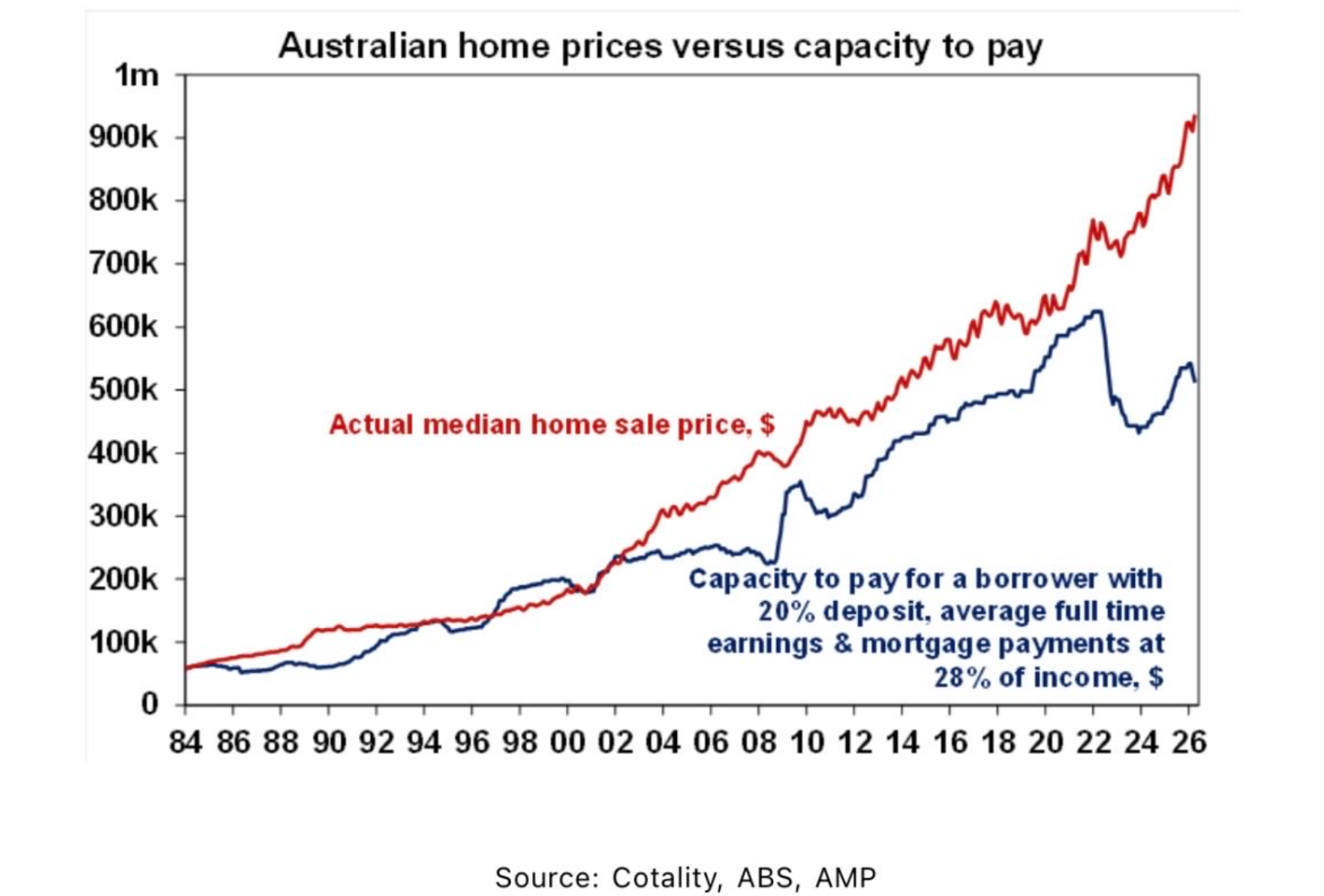

The following chart from Shane Oliver at AMP shows that a record gap has developed between borrowing capacity and home prices. This gap is widening once more amid continued (albeit slowing) home price increases alongside rising mortgage rates:

The above borrowing capacity chart suggests that home values have risen well above fundamentals, making them way overvalued.

With mortgage rates set to rise further, borrowing capacity will become even more out of alignment with prices, stretching valuations even further.

Finally, expectations that the upcoming federal budget will curb capital gains tax or negative gearing tax breaks for property investors are likely to reduce investor demand in the market, similar to what has been experienced in Melbourne after land taxes were raised on investors.

In the end, with interest rates rising, Australian housing prices need to decline to bring them more in line with borrowing capacity.

Home values cannot remain so disjointed from fundamentals forever.