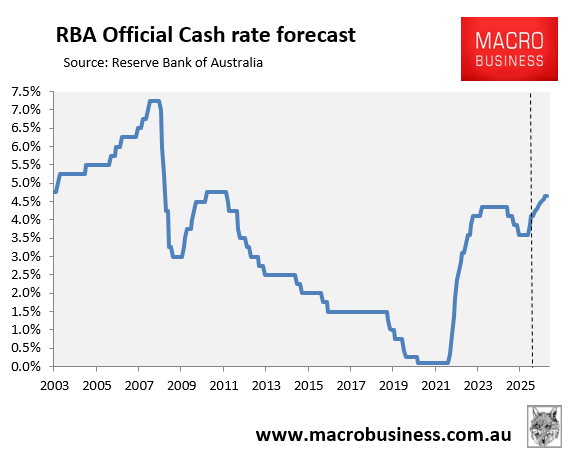

I argued last week that the Reserve Bank of Australia’s (RBA) current tightening cycle mirrors the 2007–08 hikes before the 2008 Global Financial Crisis (GFC), when the RBA kept hiking even as the US subprime crisis was unfolding.

In that earlier episode, the RBA raised rates by 1.0% in the seven months before the GFC, then was forced to slash rates by 4.0% once the crisis hit.

This time around, the RBA has already delivered two back-to-back 25 bp hikes, with the interest rate futures market fully pricing two more rate hikes by the end of the year:

This time around, the RBA is hiking amid a global energy crisis, which is likely to plunge the world into recession.

The Middle East conflict is worsening, and the Strait of Hormuz—which carries ~20% of global oil and gas trade—is likely to remain closed for the foreseeable future.

US President Donald Trump has threatened to bomb critical Iranian infrastructure, such as power plants, if the Strait remains closed. The Iranian regime has responded that it would strike the energy, desalination and information technology infrastructure of the US and its allies across the Middle East.

Thus, as reported by Tarric Brooker today, “the risk now is that the targeting of vital Iranian power infrastructure could drive Tehran to further damage energy infrastructure, potentially creating a scenario where the loss of energy supplies through the Strait of Hormuz is not a shipping issue but a much more long-term one grounded in a lack of exportable production”.

Such a scenario would push oil and gas prices sharply higher, driving global inflation while simultaneously destroying demand.

The combination is a classic stagflationary recession risk.

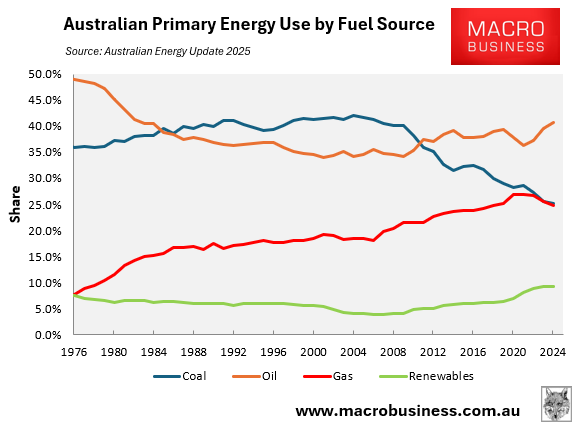

Australia relies heavily on liquid fuels, especially diesel, across mining, freight, agriculture, essential services, and backup electricity generation.

Oil already made up 41% of Australia’s primary energy use in 2024.

Eastern Australia has no gas reservation scheme, meaning domestic gas prices will likely surge alongside global prices.

Higher gas prices feed directly into electricity generation costs, fertiliser costs, and industrial input costs.

Australia, therefore, faces a severe economic slowdown if the global energy shock intensifies.

The RBA is tightening in response to a global recession, just as it did before the GFC.

When the downturn hits, the RBA will likely be forced to reverse course quickly and cut rates aggressively to prevent a deep recession.

Yarra Capital’s Tim Toohey agrees with this assessment:

Yarra Capital chief economist Tim Toohey argues that the RBA has made a major policy mistake by raising interest rates at a time when the economy is being hit by multiple simultaneous shocks—geopolitical, technological, and financial.

That is, the RBA is tightening into:

- collapsing confidence

- slowing household income

- a geopolitical oil shock

- a looming AI‑driven labour shock

- tightening global financial conditions

Toohey believes the RBA is tightening into a downturn, risking an unnecessarily deep economic slowdown.

He argues that no sensible central bank would tighten policy in response to all three shocks simultaneously.

“Choosing to tighten into large and persistent exogenous economic shocks could well prove to be one of the biggest policy errors the RBA has made”, Toohey argues.

“Expectation shocks, oil price shocks and policy errors… How many of these do you count?”

The upshot is that the RBA may be forced to respond similarly to the GFC by slashing rates to ward off a recession.