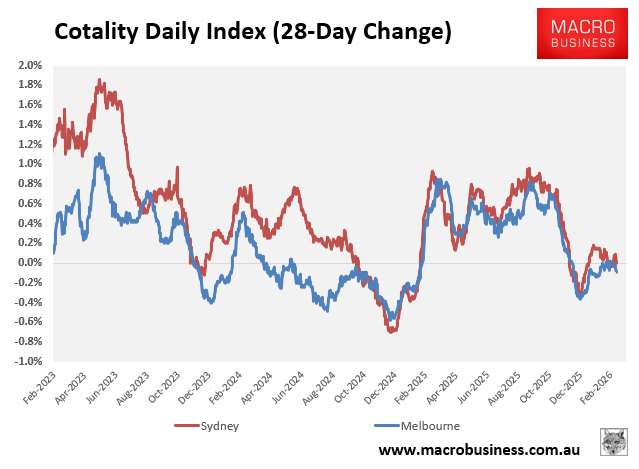

Cotality’s daily dwelling values index reports that Melbourne home values have declined by 0.1% over the past 28 days, whereas Sydney’s have recorded 0% growth:

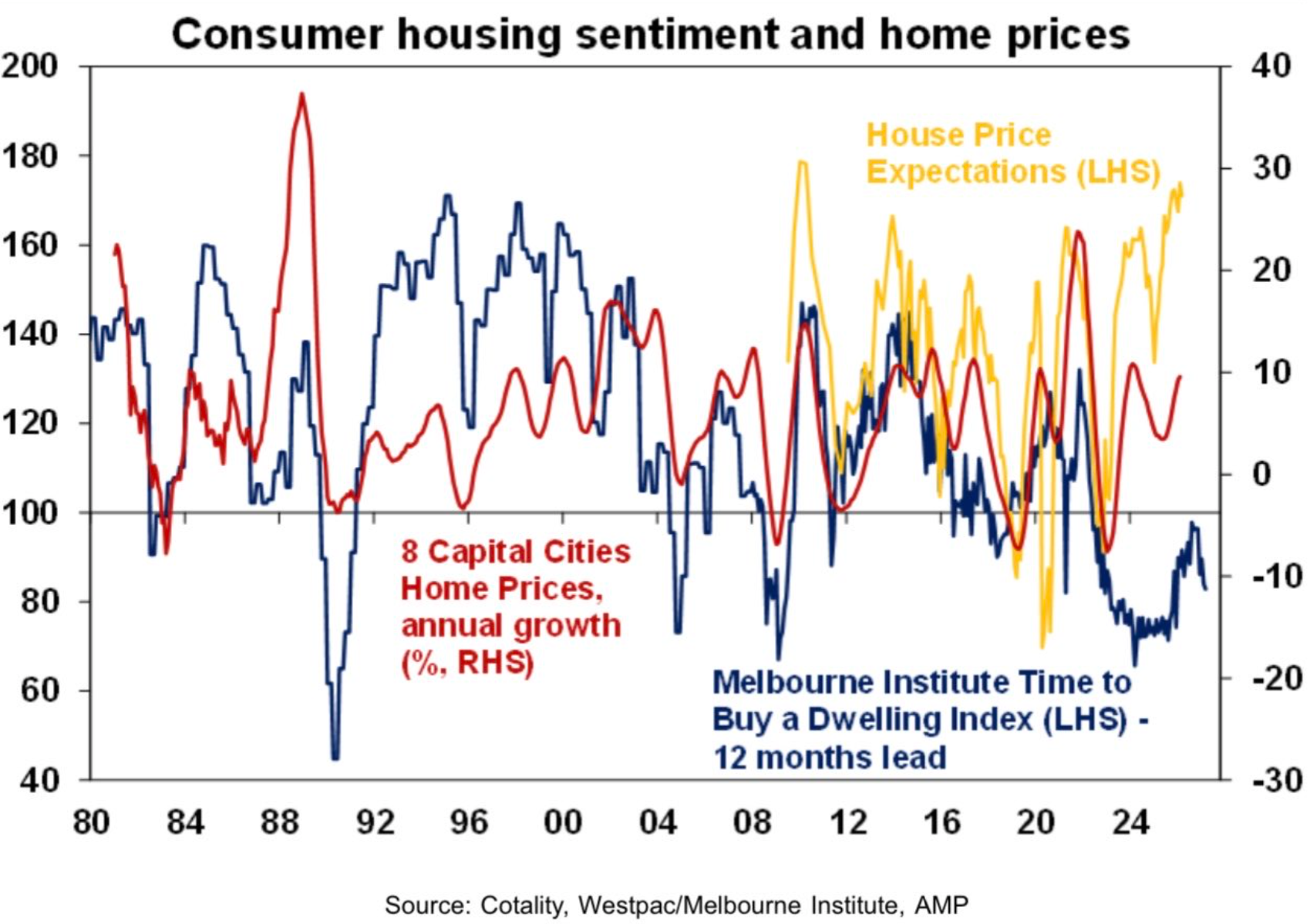

This week’s Westpac-Melbourne Institute consumer sentiment survey for March showed that while consumer house price expectations remain strong, sentiment around whether now is a good time to buy a home has declined sharply:

Chart by Shane Oliver (AMP)

As illustrated below by Justin Fabo from Antipodean Macro, homebuyer sentiment has fallen especially sharply in Sydney, which has been reflected in its decline in dwelling price growth:

Leading property market analyst Louis Christopher from SQM Research has updated his home price forecasts in light of the war in the Middle East and the upgraded inflation outlook, whereby the interest rate futures market has now fully priced two additional rate hikes in 2026, with the possibility of a third.

RBA Cash Rate Pricing

“We have downgraded our forecasts with this revision for Sydney and Melbourne. We’re now expecting housing price falls in Sydney by the order of up to 6% for the course of 2026 and for Melbourne up to 4% for the course of 2026”, Christopher said in his podcast.

“In particular, Sydney’s economy is driven by its financial services sector in many respects. Unfortunately, financial services as an industry does not do well in times like these”.

“So it’s likely we’re going to see job losses in the financial services sector, which would have a carry-on flow to the local economy, which then in turn affects the housing market”, Christopher said.

Christopher also noted on Twitter (X) that Sydney recorded its “weakest clearance rate result for a second week of March since our results began in 2020”.

The concern surrounding Sydney, in particular, is well-founded. It is the most expensive housing market in the nation and, therefore, most sensitive to interest rate hikes.

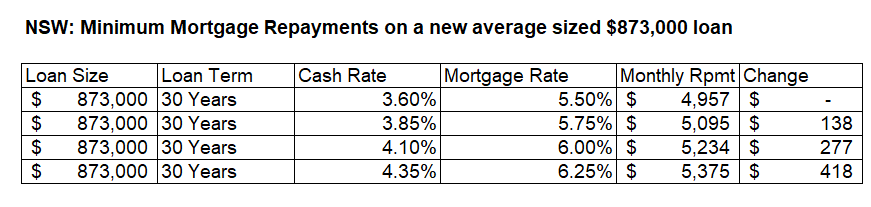

A 0.25% rise in mortgage rates adds $138 to the monthly repayments on the average new mortgage of $873,000 in NSW:

Therefore, if the RBA were to hike rates twice more, then Australia’s official cash rate would return to its recent peak of 4.35%, with average variable mortgage rates increasing to 6.25%.

The average new mortgage holder in NSW would see their minimum mortgage repayments increase by a cumulative $418 a month over what they would have paid if the RBA had not tightened.

It is little wonder, then, that Louis Christopher has forecast heavy price falls for Sydney’s housing market.