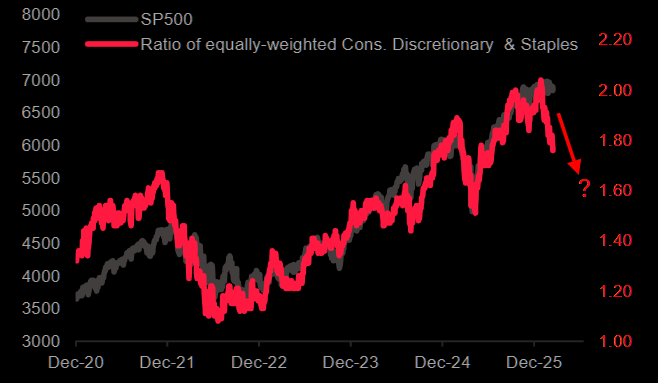

Chart from TME. The equity market is telling us that investors want stability over growth.

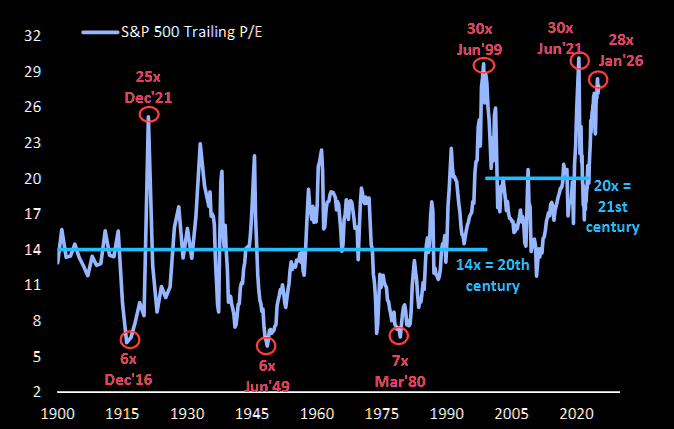

With trailing valuations so high, this is no great surprise.

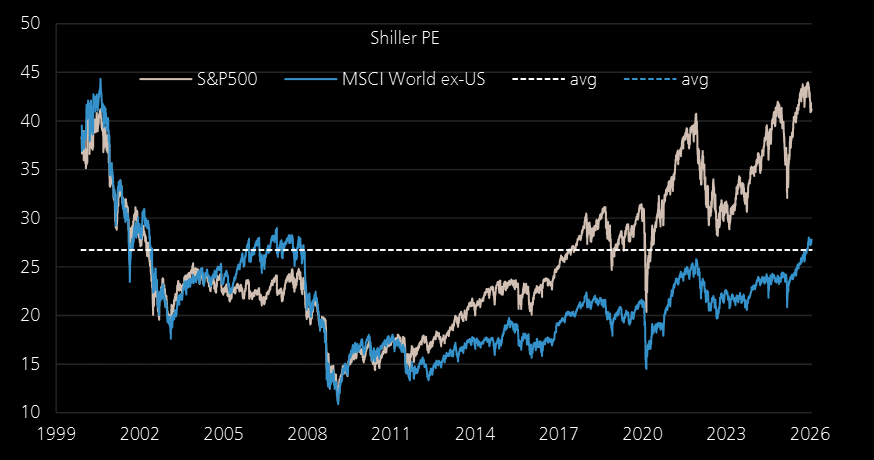

Schiller PE, which has its problems says it’s 1999 all over again,

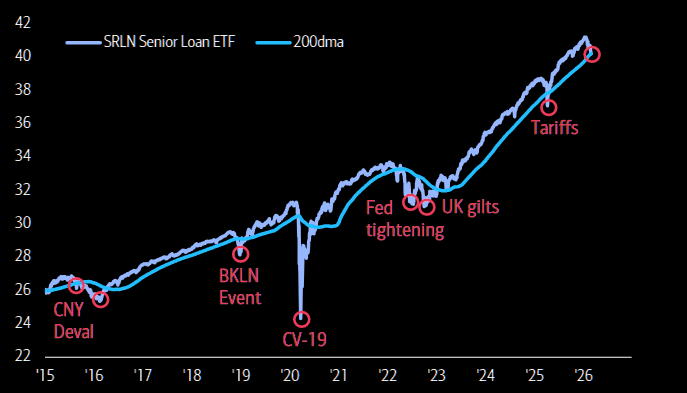

When credit cracks, you must listen. Equity sell-offs led by credit sell-offs have the potential to go much deeper. KBW is the US small bank index.

To wit.

Private equity is leading the way, as its exposure to AI disruption is seen as greater.

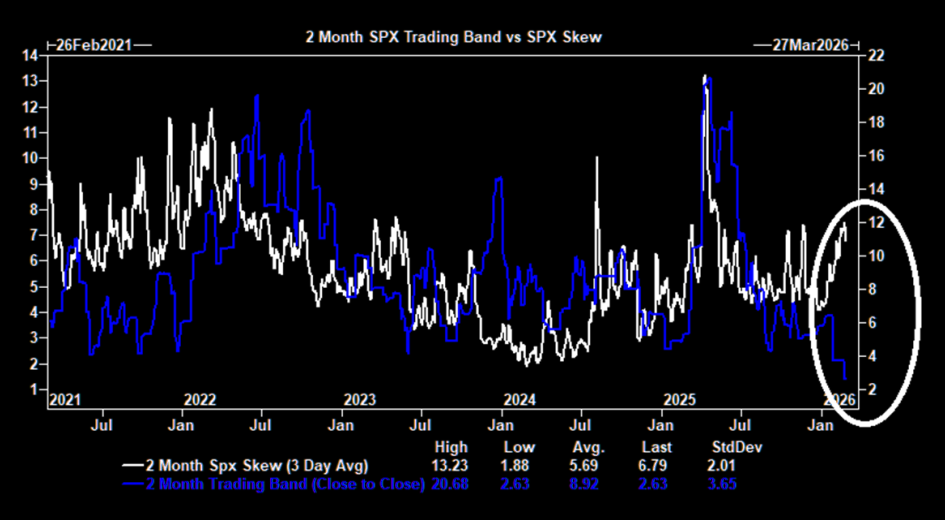

Skew is screaming “protect me”.

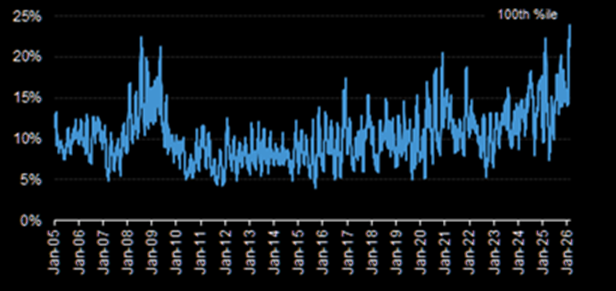

Single name volatility is setting records under the seemingly calm index bonnet.

Tech drives US valuations and outperformance.

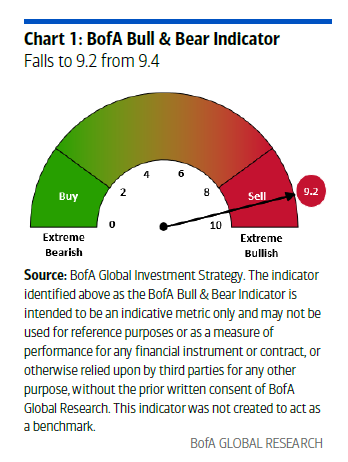

Let’s turn to Michel Hartnett at BoA for more.

Tale of the Tape: when bank loan funds break bad… “bad events” (CNY deval, COVID, UK pension crisis… (Chart 3); if SRLN Senior Loan ETF $40, XLF Financials $52 hold we’re good but key levels break… “event” coming, proper flush in risk assets, all gets priced in via big March pop in US dollar (DXY to 100), big bid for duration (note ZROZ up 5.6% YTD), until Fed eases and/or AI capex cut eases credit tension.

The Price is Right: SK Hynix (AI memory darling) up 5x past 10 months (18% more and surge matches Cisco’s 6x bubble gain Oct’98 to Mar’00), KOSPI as overbought as gold Jan’26, Bitcoin Mar’24, Mag7 Jul’23 (Chart 4) prior to pullbacks, all-time Nikkei highs, 3-year China FX high… Asia assets frontrunning global economic boom + affordability Trump need to reduce 31% China tariffs; short view… sell the greed, Asia risk assets fall ahead of US-Japan (19th) & Xi-Trump (31st) March summits.

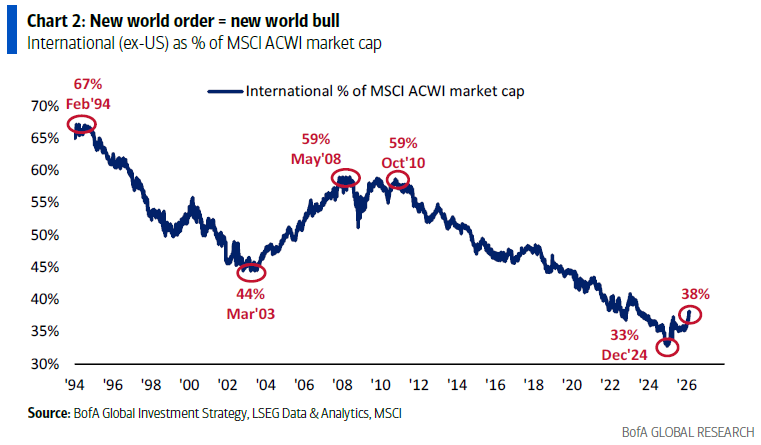

The Biggest Picture: long view… new world order = new world bull; we say international stocks outperform US H2’2020s; RoW 38% share of $97tn global stock market cap (vs US 62% – Chart 2) to rise further on fiscal excess, populism, end of deflation… plus AI disruption more labor market and/or corporate revenue negative to services-heavy US GDP & SPX index than manufacturing/resource-heavy EAFE/EM macro & equity indices.

Spot in the short term. Any enduring conflict in the Persian Gulf, or chaos afterwards as the US pulls out, with oil prices higher than expected, will not mix well with any kind of credit event in the US. The Fed could be cornered.

But I still doubt Hartnett’s take on the long.

In my view, AI will be semi-successful as a business application, so its productivity and profit benefits should be large enough to boost speak for themselves but not so large that they destroy the labour market.

This is a more attractive setup than ROW, which is stuck competing with an ever-deflating China in a zero-sum game of chasing DM demand.

Despite more stimmies, which just looks like Japanifaction to me.